A More Equitable Tax System Is Possible

April 29, 2025

By Beverly I. Moran

This essay is part of Roosevelt’s 2025 collection, Restoring Economic Democracy: Progressive Ideas for Stability and Prosperity.

The Internal Revenue Code is hideously complicated.1 The complicated rules hide many sins and give policymakers the opportunity to help the rich at the expense of everyone else.2

Consider the Child Tax Credit and the Earned Income Tax Credit.

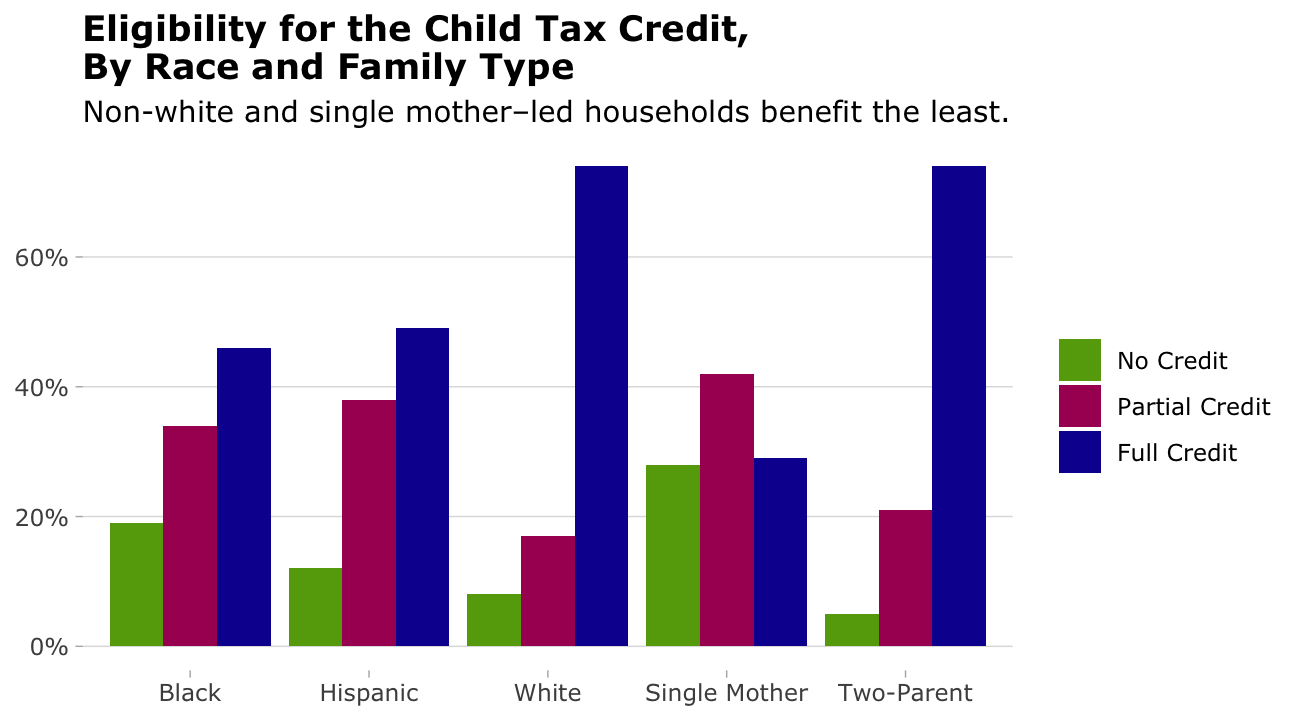

The Child Tax Credit gives eligible parents cash.3 But poor, Black, woman-headed, and Hispanic families get less. The poorest families get nothing at all. Most children living in the bottom 10 percent of household income are completely ineligible while virtually all children in the top 50 percent of income qualify for the full $2,000. A whopping 70 percent of children in families headed by single mothers do not receive the full credit, compared to 25 percent of children in two-parent homes. Black children make up 25 percent of ineligible children, although they are only 14 percent of all children.4

The Earned Income Tax Credit, meanwhile, is meant to help working people climb out of poverty.5 Want to increase your chance of an audit?6 Apply for the Earned Income Tax Credit.7 Indeed, Humphreys County, Mississippi—where a third of the people live in poverty—is the most audited county in the entire United States.8 Imagine living in a rural county with little public transportation and low literacy and numeracy rates and fighting an audit between your two minimum wage jobs.9 Seem like a fair fight to you?

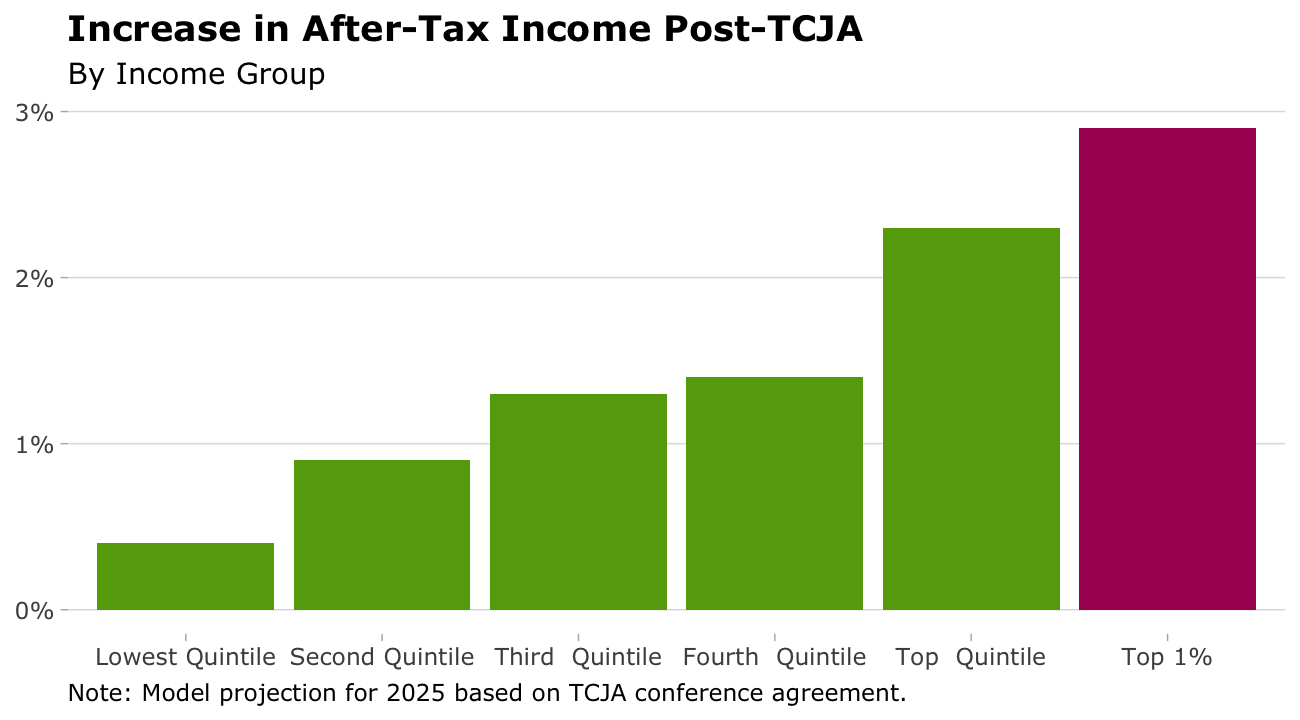

The Tax Cuts and Jobs Act of 2017 made the most significant changes to the Internal Revenue Code in 30 years.10 From 2018 to 2024, these temporary cuts primarily benefited the wealthy while adding nearly $2 trillion to the federal debt.11 In fact, 80 percent of the corporate tax cuts between 2018 and 2022 went to the top 10 percent of earners.12 In 2018, the wealthiest 0.1 percent of households received an average tax cut of $193,380, while the middle 20 percent only saw an average tax cut of $930.13 The individual tax cuts offered little to those making less than $70,000 a year. Indeed, by 2023, these lower-income taxpayers actually saw a decrease in their after-tax income, while those earning $500,000 or more continued to benefit.14

Extending these cuts for another 10 years could add another $4 trillion to the national debt, with nearly half of the benefit going to households that earn $450,000 or more.15

But these cuts are set to expire this year, meaning policymakers have the opportunity in 2025 to undo some of this damage and benefit lower-income taxpayers.

Three Ways to Improve the Tax Code in 2025 to Benefit Lower-Income Taxpayers

- Modify the Child Tax Credit so that it helps the poorest children. As it stands, the credit gives families in the top 50 percent of income $2,000 per child while half the families in the bottom 10 percent get nothing at all.

- For the Earned Income Tax Credit, return to the inflation measure the Internal Revenue Service (IRS) used to adjust the income eligibility ceiling before the 2017 law. The current inflation measure assumes that people can adjust their spending in ways that do not exist for people in food and transportation deserts.

- End all itemized deductions. The 2017 law increased the standard deduction to the point that 90 percent of taxpayers no longer use the itemized deductions. The Congressional Research Service calculates that ending itemized deductions will go a long way to reducing the budget deficit and, because higher income groups are the beneficiaries of the deductions, their demise would reduce income inequality.

Ensure the Child Tax Credit Reaches All Low-Income Families

The 2017 tax reform increased the credit from $1,000 to $2,000 per child, raised the income limit for eligibility from $110,000 to $400,000, and capped the refundable amount to $1,400 per child.16 As a result, 90 percent of families benefit from the credit.17 However, some groups such as poor, Black, Hispanic, and single-mother-headed families get less or nothing at all.18

Lower-income families are less likely to owe $2,000 in tax per child, and they sometimes owe nothing if their earned income is too low. Without owing taxes, there is nothing to refund—pushing the maximum amount of the Child Tax Credit out of reach for families who could use the money most.

To improve the Child Tax Credit:

- Lower the income ceiling to pre-2018 levels. (This will happen automatically if the 2017 tax law expires.)

- Allow poor families with no earned income to qualify for the credit.

- Keep the credit at $2,000 and make the full refund of $2,000 available to all eligible families.

Change the Inflation Measure for the Earned Income Tax Credit

The Earned Income Tax Credit supports low-income workers. However, inflation can rob taxpayers of these benefits by pushing their incomes over the eligibility ceiling. To correct for this contingency, Congress can adjust the credit’s income ceiling for inflation.

The 2017 law permanently changed how the IRS calculates inflation adjustments. Before 2018, the IRS used the Consumer Price Index for All Urban Consumers (CPI-U), which assumes that people buy the same “basket of goods” even when prices rise.19 The 2017 law switched to the Chained Consumer Price Index for All Urban Consumers (C-CPI-U), which assumes that people adjust their spending to limit the impact of rising prices.

This new inflation measure hurts low-income people, who often do not have the flexibility to adjust their spending the way the C-CPI-U imagines. For example, they disproportionately live in areas with fewer affordable food options and less access to transportation.20

To fix this, the law should direct the IRS to return to the Consumer Price Index for All Urban Consumers (CPI-U). Because this metric permanently changed in 2017, the 2025 expirations would not automatically make this happen.

Eliminate Itemized Deductions

Finally, the 2017 tax reform doubled the standard deduction, eliminated personal exemptions, and temporarily altered itemized deductions.21 As a result, 90 percent of taxpayers now use the standard deduction.22 It’s simpler and saves time and money. With so few taxpayers using itemized deductions, it has never been a better time to end them all.

Ending all itemized deductions would reduce income inequality. Higher-income households are the most likely to itemize deductions. Since the 2017 law, only 2 percent of taxpayers who earn under $30,000 itemize, while over 64 percent of taxpayers earning over $500,000 do.

Ending all itemized deductions would reduce the deficit by $2.5 trillion between 2023 and 2032.23 It would also make tax obligations more consistent across income groups. These deductions undermine the progressive tax by lowering the taxable income wealthy individuals reflect on their returns. Repealing all itemized deductions and keeping the larger standard deduction that is set to expire in 2025 would go a long way toward a more equitable tax code.

The more we decrease poverty, the more we increase the likelihood that our government can give us all the best possible life. We can’t, and shouldn’t, rely solely on the Internal Revenue Code to solve poverty, but the expiration of the 2017 tax law in 2025 is an opportunity to make things better.

Read Footnotes

- NYU School of Law, “Schenk Tells NPR That the U.S. Tax Code Is So Complex That Most Filers Make Mistakes,” news release, accessed April 15, 2025, https://law.nyu.edu/news/SCHENK_NPR.

↩︎ - Allaire Urban Karzon, “Tax Expenditures and Tax Reform,” review of Tax Expenditures, by Stanley S. Surrey and Paul R. McDaniel, Vanderbilt Law Review, 1985, https://heinonline.org/HOL/LandingPage?handle=hein.journals/vanlr38&div=51&id=&page=.

↩︎ - “Child Tax Credit Overview,” National Conference of State Legislatures (NCSL), updated November 22, 2024, https://ncsl.org/human-services/child-tax-credit-overview.

↩︎ - Sophie Collyer, David Harris, and Christopher Wimer, Left Behind: The One-Third of Children in Families Who Earn Too Little to Get the Full Child Tax Credit, Columbia University, Center on Poverty and Social Policy, May 13, 2019. https://povertycenter.columbia.edu/sites/default/files/content/Publications/Who-Is-Left-Behind-in-the-Federal-CTC-CPSP-2019.pdf.

↩︎ - “Policy Basics: The Earned Income Tax Credit,” Center on Budget and Policy Priorities, updated April 28, 2023, https://cbpp.org/research/policy-basics-the-earned-income-tax-credit.

↩︎ - Paul Kiel and Jesse Eisinger, “Who’s More Likely to Be Audited: A Person Making $20,000—or $400,000?” ProPublica, December 12, 2018, https://propublica.org/article/earned-income-tax-credit-irs-audit-working-poor.

↩︎ - “How Do IRS Audits Affect Low-Income Families?” Tax Policy Center, updated January 2024, https://taxpolicycenter.org/briefing-book/how-do-irs-audits-affect-low-income-families.

↩︎ - Paul Kiel and Hannah Fresques, “Where in the U.S. Are You Most Likely to Be Audited by the IRS?” ProPublica, April 1, 2019, https://projects.propublica.org/graphics/eitc-audit.

↩︎ - “Humphreys County School District,” US News & World Report, accessed April 15, 2025, https://usnews.com/education/k12/mississippi/districts/humphreys-co-school-dist-102847.

↩︎ - “Tax Cuts and Jobs Act of 2017 (TCJA),” Legal Information Institute, Cornell University, updated May 2022, https://law.cornell.edu/wex/tax_cuts_and_jobs_act_of_2017_(tcja); “The Tax Cuts and Jobs Act Makes Significant Changes to Taxation of Business Operations,” Schmiedeskamp Robertson Neu & Mitchell LLP, accessed April 15, 2025, https://srnm.com/the-tax-cuts-and-jobs-act.

↩︎ - “T17-0314 – Conference Agreement: The Tax Cuts and Jobs Act; Baseline: Current Law; Distribution of Federal Tax Change by Expanded Cash Income Percentile, 2025,” Tax Policy Center, December 18, 2017, https://taxpolicycenter.org/model-estimates/conference-agreement-tax-cuts-and-jobs-act-dec-2017/t17-0314-conference-agreement; “How Did the TCJA Affect the Federal Budget Outlook?” Tax Policy Center, updated January 2024, https://taxpolicycenter.org/briefing-book/how-did-tcja-affect-federal-budget-outlook.

↩︎ - Patrick J. Kennedy, Christine Dobridge, Paul Landefeld, and Jacob Mortenson, “The Efficiency-Equity Tradeoff of the Corporate Income Tax: Evidence from the Tax Cuts and Jobs Act,” working paper, March 21, 2024, https://patrick-kennedy.github.io/files/TCJA_KDLM_2024.pdf.

↩︎ - Sanam Rasool, William Alan Reinsch, and Thibault Denamiel, “Revenue Implications of Tax Cut and Jobs Act Provisions in 2025,” Center for Strategic & International Studies, December 19, 2024, https://csis.org/analysis/revenue-implications-tax-cut-and-jobs-act-provisions-2025.

↩︎ - “The 2017 Tax Revision (P.L. 115-97): Comparison to 2017 Tax Law,” Congressional Research Service, updated February 6, 2018, https://crsreports.congress.gov/product/pdf/R/R45092.

↩︎ - David Trimmer, “Extending the Tax Cuts and Jobs Act,” Policy Engine, October 28, 2024, https://policyengine.org/us/research/tcja-extension; Howard Gleckman, “Those Making $450,000 and Up Would Get Nearly Half the Benefit of Extending the TCJA,” Tax Policy Center, July 8, 2024, https://taxpolicycenter.org/taxvox/those-making-450000-and-would-get-nearly-half-benefit-extending-tcja.

↩︎ - NCSL, “Child Tax Credit Overview.”

↩︎ - Jacob Goldin and Katherine Michelmore, “Who Benefits from the Child Tax Credit?,” National Tax Journal 75, no. 1 (2022): 123–47, http://nber.org/papers/w27940.

↩︎ - Collyer, Harris, and Wimer, Left Behind.

↩︎ - “Consumer Price Index Frequently Asked Questions,” Bureau of Labor Statistics, last modified December 18, 2024, https://bls.gov/cpi/questions-and-answers.htm.

↩︎ - “Communities with Limited Food Access in the United States,” Annie E. Casey Foundation, updated August 4, 2024, https://aecf.org/blog/communities-with-limited-food-access-in-the-united-states.

↩︎ - “Topic No. 551, Standard Deduction,” Internal Revenue Service, last modified January 2, 2025, https://irs.gov/taxtopics/tc551; “Tax Reform Provisions That Affect Individuals” Internal Revenue Service, last modified November 18, 2024, https://irs.gov/newsroom/individuals.

↩︎ - “What Is the Standard Deduction?” Tax Policy Center, updated January 2024, https://taxpolicycenter.org/briefing-book/what-standard-deduction.

↩︎ - “Eliminate or Limit Itemized Deductions,” Congressional Budget Office, December 7, 2022, https://cbo.gov/budget-options/58635.

↩︎