Reining in Corporate Power

April 29, 2025

By Lenore Palladino

This essay is part of Roosevelt’s 2025 collection, Restoring Economic Democracy: Progressive Ideas for Stability and Prosperity.

In the first weeks of the Trump administration, it became clear to everyone that extreme corporate power has deep political and economic consequences. The issue is not just Elon Musk’s ability to run rampant but instead, as Rana Foroohar put it, the “Faustian bargain” that business leaders have made with Trump.1 What can we do at this moment to start to reverse the decades-long growth of corporate power and the enduring negative impacts of the corporate governance paradigm of shareholder primacy?

Even when political conditions make immediate reform unlikely, we should continue developing and exploring new economic frameworks, regardless of their current political feasibility. The value of innovative economic thinking is not limited by whether reforms can pass in the present moment. As part of our work developing policies for a stronger economy and society, I propose that reshaping the role of corporations in society must be central. This requires two areas of work: The first is ending how shareholder primacy structures internal corporate decision-making. The second is ending the myth that shareholders are always investors. It is also critical to structurally reform the financial sector, because the previously drawn lines between regulated and unregulated finance simply no longer hold.

The corporate decision-making framework of shareholder primacy has meant that rather than investing in productive capabilities, companies prioritize short-term profits and shareholder payments through mechanisms like stock buybacks. Shareholder primacy undermines corporations’ implied duty to benefit society through innovation: Corporations receive privileges through public charters of limited liability and perpetual existence, shielding shareholders from the risks of the actual business. This framework has worsened economic and racial inequality by benefitting the economic elite of white, wealthy households that own the vast majority of corporate shares, while (not coincidentally) increasing the compensation of corporate executives.

It is time for federal lawmakers to require large corporations to incorporate federally and to set new rules for corporate governance that balance the interests of stakeholder groups, including workers, managers, customers, and shareholders. The corporation’s privileges come from the public, and we have the right to promote innovation and productivity rather than extraction. In my book, Good Company: Economic Policy After Shareholder Primacy, I detail specific policy interventions to rebalance power within corporations and refocus on the capacity of businesses to produce goods and services that actually serve society. These include rules to curb financial extraction, include workers and other stakeholders in the decisions of the business, and require that the board of directors is accountable to the corporation itself, rather than solely to shareholders, and includes worker voices.2

The second area of work is to reckon with the paradigm that supports shareholder primacy: the assumption that shareholders buying and selling stock leads to real business investment, which is so deeply buried that it can be hard to see.3 The conflation of shareholding and investing—the concept that trading financial assets leads to productive investment in goods-and-services production—is not only conceptually confused but also perniciously supports the corporate governance paradigm of shareholder primacy. The widespread belief that stockholders are always “investors” has helped justify corporate policies that prioritize shareholder interests above all else. In reality, most shareholders, including those who own stocks through various financial intermediaries, aren’t directly contributing to companies’ productive capabilities.

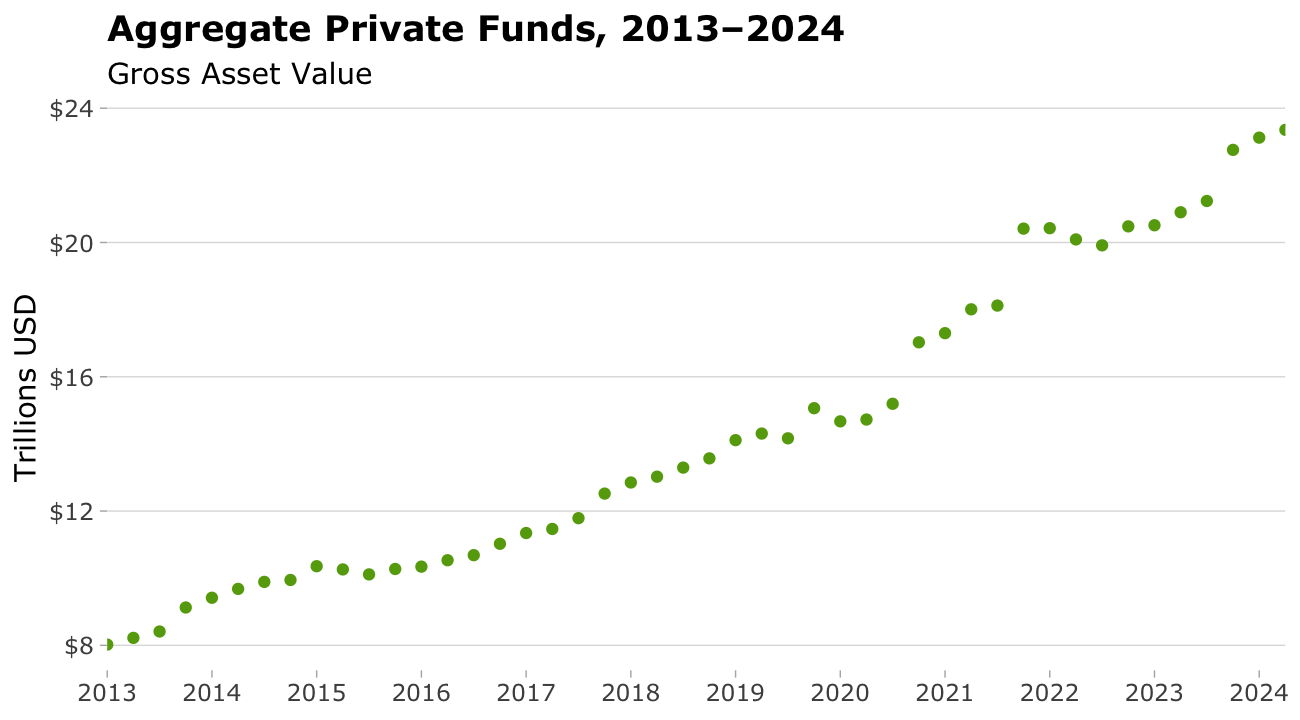

Another area for reform from the root is how we regulate the financial sector, because the regulations set up in the New Deal no longer match the financial sector we have in 2025. The divisions between regulated banking and all other ways that people and business transact and lend no longer make sense, and the securities laws that enabled the “private” side of financial markets to operate in the dark, based on the theory that wealthy people were sophisticated enough to know their risks, don’t work when all of us are part of these markets through our asset managers. The growth of private financial markets has now reached the point where “private” trading dominates financial activity: Private funds have approximately tripled in size in the past decade to $26 trillion in gross assets (compared to the $23 trillion in the US commercial banking industry). Private markets raise more in equity than public markets: In 2021, new stock issuances resulted in $434.7 billion, while private markets raised $1.73 trillion in committed funds that same year—almost four times as much.4 The regulated banking sector is becoming more and more enmeshed with private credit funds and other nonbank financial institutions, and the risks are being recognized by, among others, the International Monetary Fund.5 Today we have distinctions without a difference in too many areas of finance. Finance should be regulated holistically with the ultimate goal in mind: Finance should support a productive economy.

We have no choice but to focus on structural reform because piecemeal efforts to rein in the power of corporate leaders have led us to today. The American people recognize how extreme elite power is and are looking for leaders to propose structural changes. New economic paradigms are necessary to end corporate shareholder primacy, regulate finance holistically, and, well, “Make Corporations Innovate Again.”

Read Footnotes

- Rana Foroohar, “Doge Versus Business,” Financial Times, February 24, 2025, https://ft.com/content/63a413b7-1d02-4865-917e-1a99bbb0e135. ↩︎

- Lenore Palladino, Good Company: Economic Policy After Shareholder Primacy (University of Chicago Press, 2024).

↩︎ - Lenore Palladino and Harrison Karlewicz, “The Myth That Shareholders Are Always Investors: Challenging the Paradigm of Shareholder Primacy,” Roosevelt Institute, November 21, 2024, https://rooseveltinstitute.org/publications/myth-shareholders.

↩︎ - Lenore Palladino and Harrison Karlewicz, “The Growth of Private Financial Markets,” Political Economy Research Institute, May 2024, https://peri.umass.edu/wp-content/uploads/joomla/images/publication/WP600.pdf.

↩︎ - “The Last Mile: Financial Vulnerabilities and Risks,” International Monetary Fund, April 2024, https://imf.org/en/Publications/GFSR/Issues/2024/04/16/global-financial-stability-report-april-2024.

↩︎