Trump Blows Up the Economy, Calls It Trade Policy

April 11, 2025

Tariffs can be strategic—Trump’s plan is anything but.

The Roosevelt Rundown features our top stories of the week.

(Photo by Kayla Bartkowski/Getty Images)

Making Sense of Nonsensical Tariffs

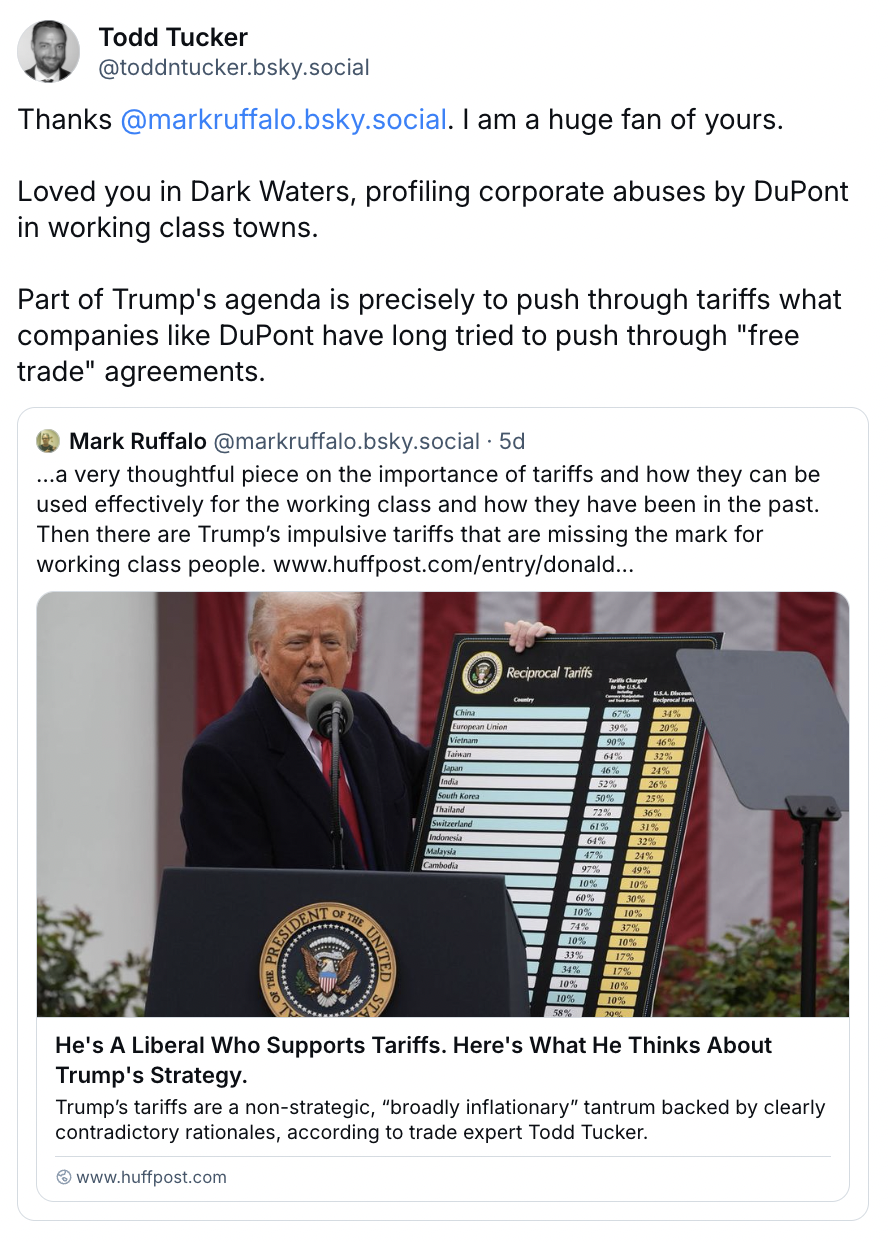

Uncertainty looms over the daily economic lives of Americans as President Trump’s chaotic announcements of indiscriminate tariffs continue to dominate headlines. “The administration has been barreling down this tunnel towards an economic collapse,” Roosevelt’s Todd N. Tucker said in an interview with HuffPost this week. “This tantrum that Trump is throwing is not well-reasoned and not well-thought out.”

- What doesn’t add up: Administration officials’ justifications for the sweeping tariffs have varied from raising revenue via import taxes to bringing back manufacturing. But “those purposes are at odds with each other,” Tucker explained to HuffPost. If a tariff is effective in its goal to boost domestic industry, then revenues would necessarily be low: “The imports aren’t coming in and paying the tariff, they’re just not coming in.”

A truly progressive use of tariffs would be “directed to the most important goals for working-class livelihoods and the environment,” Tucker said in an interview with The Intercept. Measured trade protections could be used “to address the most fundamental problems we face in the economy, rather than willy-nilly applying them across the board.”

- What tariffs could do: Tucker explained the role industrial policy could have in the renewable energy transition to the Boston Globe: “When it comes to building green technologies,” the Globe recounts, “America is something like a developing country.”

- What else we need: But trade protections alone don’t make up a comprehensive industrial policy—Tucker spoke to Slate about the policies that would be needed to complement targeted tariffs. “A tariff isn’t going to hire people at national labs to do experiments for new tech,” he said. “For that, you need to have a staffing strategy, a recruitment strategy, and a higher education strategy.”

While economists are predicting increased inflation as a short-term result of tariffs, the longer-term economic outlook is more uncertain. “Which system is gonna be hurt the most when you jab a fork into a light socket? I don’t really know,” Principal Economist Mike Madowitz told Axios. “That’s why we don’t force forks into light sockets, traditionally.”

What FDR Teaches Us: Crisis Calls for a New Common Sense

“Ideas matter for making democracy and capitalism work together,” Roosevelt President and CEO Elizabeth Wilkins said this week during an expert town hall hosted by Patriotic Millionaires. “The ecosystems to make certain ideas the common sense are incredibly important,” she explained—for example, the ideas that government should shape markets and provide a safety net for the people. These were among the paradigm shifts that the New Deal put into motion. Facing today’s crises will require the same thoughtful effort of building and fighting for a new common sense.

As Wilkins explained, the US was at a crossroads in 1933. When Franklin D. Roosevelt was first sworn in, “he was walking into a world where the common sense was that government did not intervene strongly in markets.” The Great Depression had already upended millions of livelihoods, but to that point, the government’s response was to “[ask] politely for groups of business leaders to voluntarily step up to coordinate a response to an economic crisis,” Wilkins said. “And it wasn’t working.”

People questioned “whether our system of governance could deliver a basic sense of economic security and prosperity for ordinary people,” Wilkins said. It was President Roosevelt’s bold governance that finally began to change the common sense: Government could, and should, intervene in markets to advance the public good. It should raise and invest tax revenue and build worker power. It should uphold the social contract and protect its people from the excesses of corporate wealth.

The public’s faith in the economy and in democracy go hand in hand, and it was undermined again with the 2008 financial crisis. Now, as authoritarianism takes hold and economic turmoil is all but guaranteed, “people are looking for different ideas.” To put it simply, they’re looking for a new common sense.

What We’re Reading

- Even if Trump’s tariffs somehow succeeded in bringing manufacturing back to the US, it wouldn’t bring back the “good life”—at least, not without also expanding progressive taxes, strong unions, robust regulations, and a plan to include women and people of color in the economy, Roosevelt Fellow Jessica Calarco argues on MSNBC.

- The administration is planning to slash public investments across the country, including a $500 grant to steel company Cleveland Cliffs in Middletown, Ohio—the hometown of Vice President J.D. Vance. “You can’t cut your way to economic competitiveness,” Roosevelt Senior Fellow Sameera Fazili, who served in the Biden administration, said to CNN. “You have to make strategic public investments.”

- “What we were trying to do with these kinds of programs was to strengthen US economic competitiveness and reshore manufacturing, which aligns really well with the Trump administration and its energy abundance agenda, reshoring manufacturing agenda,” said Fazili. “And instead, the Trump administration has just had this slash-and-burn policy.”

- A new report from Groundwork finds that top companies’ shareholder returns eclipsed their federal taxes paid since Trump’s 2017 tax law went into effect.

- Roosevelt Senior Fellow Lenore Palladino told The Guardian that stock buybacks are merely a symptom of shareholder primacy—“It’s the legal fact that corporations exist solely to make money for shareholders,” she said. “That’s their purpose.”