We Still Need Stimulus: How the CBO’s New Report Captures the Urgency of This Moment

February 1, 2021

By Mike Konczal, J.W. Mason

Today, the Congressional Budget Office released its latest 10-year economic projections in An Overview of the Economic Outlook: 2021 to 2031. The most important part of this document, for current debates, is the estimate that the output gap—the difference between actual GDP and potential—will be smaller over the coming years than previously expected. The CBO made this estimate based on a projection of stronger growth this year while still maintaining a smaller decline in long-term potential GDP.

Opponents of the Biden administration’s $1.9 trillion stimulus and relief package are using this forecast to argue that a major stimulus bill is no longer needed and that a scaled-down bill would suffice. But this is false; further examination of the report’s arguments only reinforces the urgent need for a significant economic response.

There are three problems with the report as a justification for a smaller stimulus package.

- First, the CBO is overly optimistic that there will be a rapid recovery in the next two years. They assume a growth rate of 3.7 percent over the next year, even without additional stimulus. But there is little reason to expect that such rapid growth will happen on its own. This is faster growth than the economy ever reached during the last recovery and expansion.

- Second, the CBO is needlessly pessimistic about the possibility of long-term growth. They predict that unemployment will never fall below 3.9 percent, even though it was well below 4 percent for two years, reaching 3.5 for a sustained period, prior to the pandemic. They assume that the economy in January 2020 was already operating well above potential, even though there was no sign of inflationary pressure at that time and the Fed was in fact cutting rates. They also still project a lower level of potential output than they did prior to the pandemic, implying that the pandemic has permanently reduced the economy’s productive capacity in ways that strong growth cannot overcome.

- Third, the CBO is disturbingly complacent about a forecast that the economy will not reach what they consider full employment and potential output until 2025. There is no reason we should accept an additional four years of depressed incomes and elevated unemployment. So even taken at face value, the CBO’s numbers imply that the economy is still in need of major stimulus.

The optimism about actual growth appears unwarranted, especially as the recovery has faltered in recent months. The pessimistic conceptions of full employment and economic potential ignore the repeated failures of similar forecasts before the pandemic. The suggestion that we should complacently accept half a decade of needless unemployment and lost production is unacceptable.

What the CBO report really shows is a still-broken economy that will cause needless pain for years to come if we fail to take action. Rather than offering an argument against a broad stimulus bill, it demonstrates the need for bold, sustained efforts to combat the ongoing crisis.

The CBO is too optimistic about growth.

The new CBO report predicts that “real GDP expands rapidly over the coming year, reaching its previous peak in mid-2021 and surpassing its potential level in early 2025.” This is based on the assumption that real growth will reach 3.7 percent over 2021—a growth rate the US has not seen since 2004—and remain strong in the following years.

But as recent estimates from the Economic Policy Institute, the Brookings Institute, and Groundwork Collaborative find, the economy will continue to struggle in the next two years without a substantial spending package.

Growth slowed sharply in the fourth quarter of 2020, employment has stalled well below its pre-pandemic levels, and economists worry that unemployment will begin to inch up again.

These are warning signs: Even if the virus is brought under control, a strong recovery is not guaranteed. And given the uncertainty of vaccine rollouts and new coronavirus mutations, we cannot assume the virus won’t still be with us in late 2021.

The CBO produces a single estimate, as is its mandate, but policy can and should take into account the range of possible risks, which at this moment are far greater on the downside. Even if we agreed that the CBO’s growth forecast was the most likely one, there would still be a strong argument for “excessive” stimulus as an insurance policy. It is much easier to rein in a hot economy, if that indeed becomes a problem, than to restart the economy once a deep recession is allowed to begin.

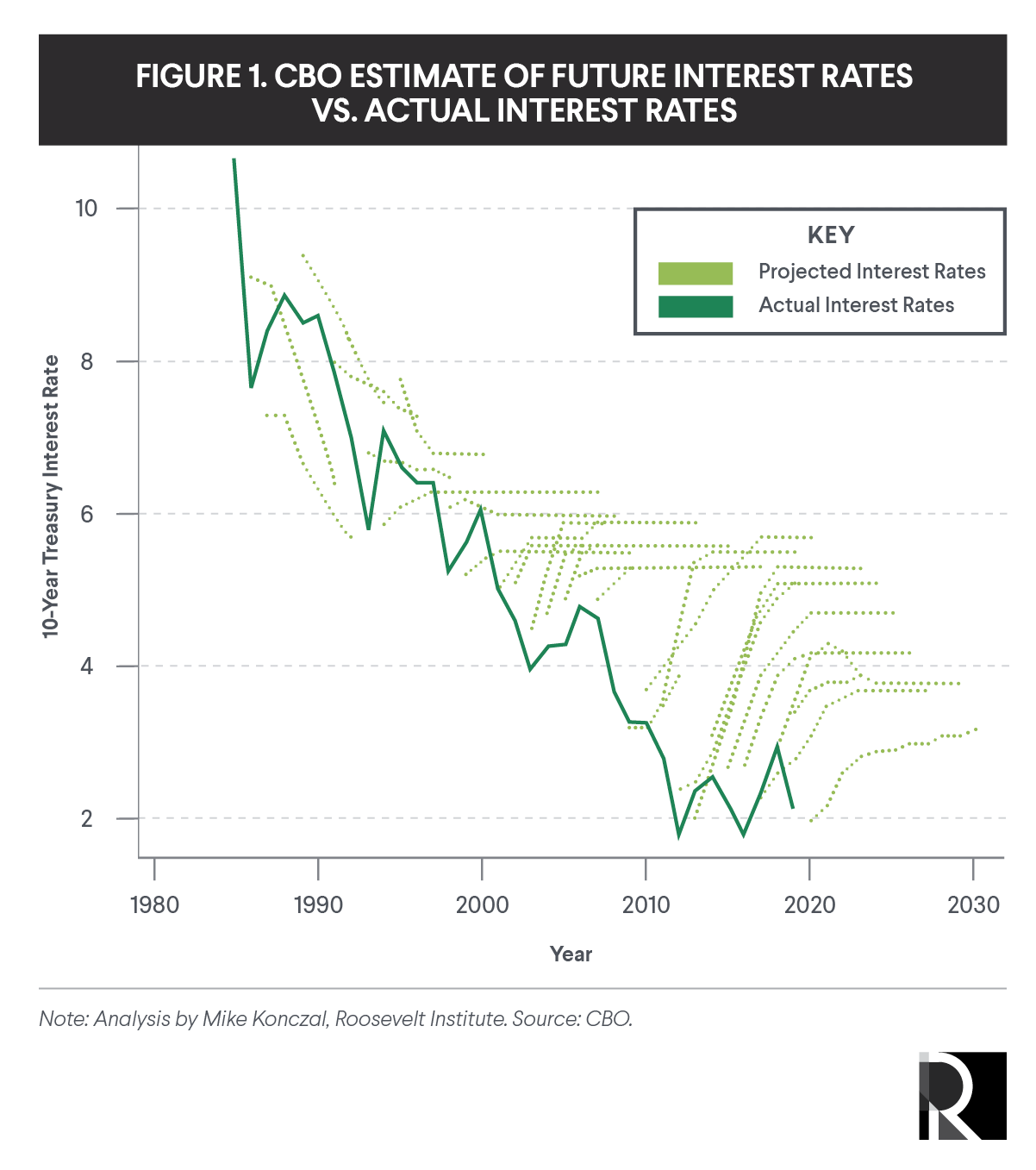

Nor does the CBO’s track record inspire confidence. On many occasions, the CBO has argued that recoveries are coming faster than they ever do. In the current report, the CBO has raised its forecast for the rate of interest, expecting rate normalization to correspond with an increasingly robust recovery. They also did that repeatedly during the Great Recession, falsely assuming that full recovery was just two to three years away each and every year. This consistent error on the side of faster growth and higher interest rates has been a feature of CBO modeling since the mid-1990s.

The CBO is too pessimistic about potential output.

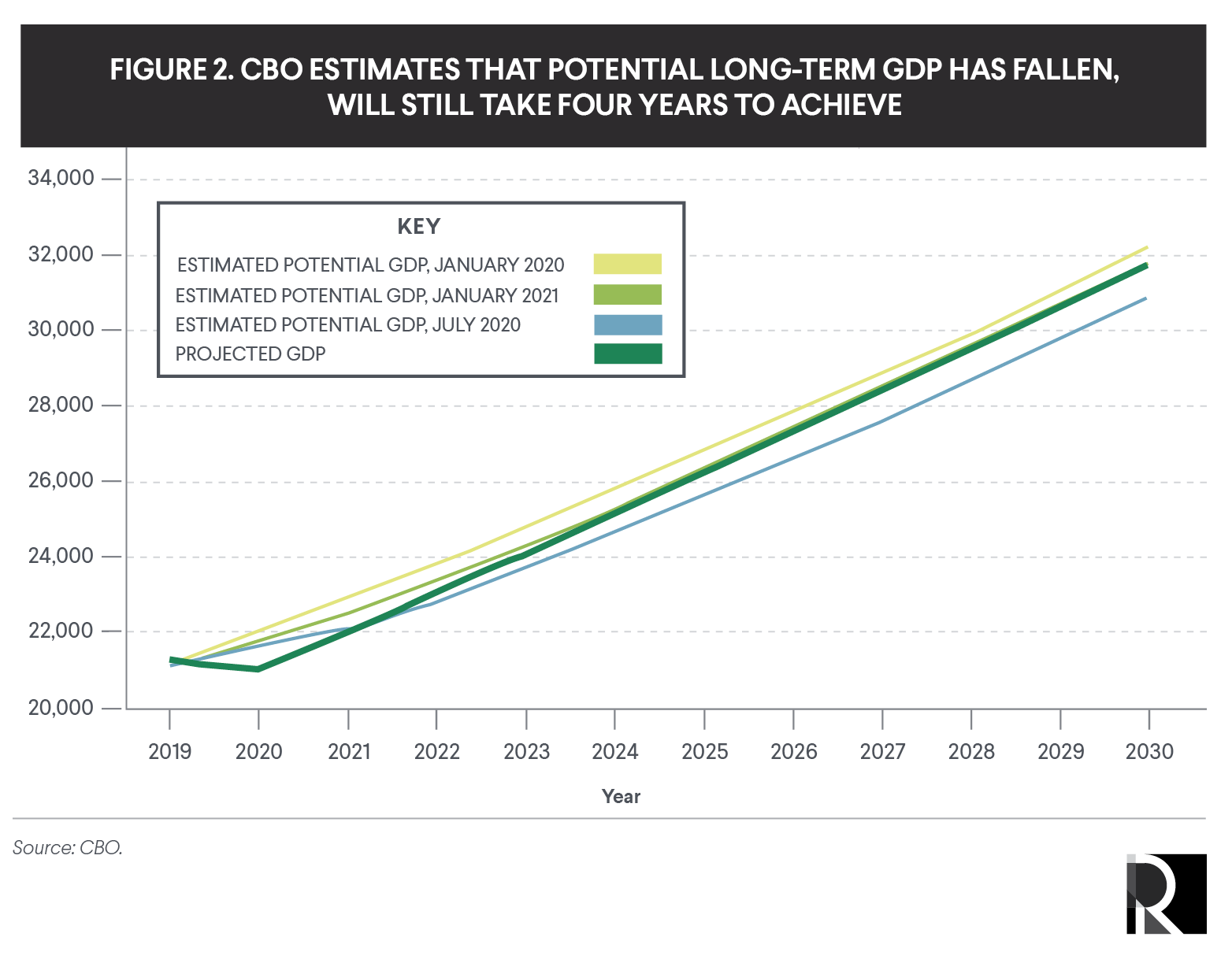

The optimistic forecasts for growth are not the only reason the CBO predicts a rapid return to full employment. In the CBO’s scenario, we reach full employment in large part through a fall in potential output—the amount of GDP our economy is capable of producing when we reach full employment—rather than through a GDP increase alone. If true, this means that the economy is permanently poorer as a result of the crisis.

The CBO’s estimate of potential output for 2025 is now about 2 percent lower than its estimate from last January. If we compare its projections for GDP growth to the potential estimate from a year ago, the economy would not return to full employment for another three years, until 2028.

It is not clear what has happened in the past year that should lead to a lower estimate for the productive potential of the US economy; while the pandemic has been terrible in many ways, it certainly has not removed 2 percent of the labor force, or destroyed our capital and technical knowledge. Instead, the reduction in potential output appears to be the mechanical result of adjusting the estimate of potential in response to any change in actual output.

And even the estimates of a year ago were clearly too conservative. The CBO still believes that the lowest sustainable long-term unemployment rate is 3.9 percent, and that as of January 2020, the economy was operating above potential, or overheating.

But this flies in the face of what we know about actual economic conditions before the pandemic. Despite the low measured unemployment rate, there was no sign of accelerating inflation, which remained stubbornly below the target level of 2 percent. Wage growth, while stronger than in the immediate aftermath of the Great Recession, was still nowhere near fast enough to bring the labor share of national income back up to its historical levels. And the Federal Reserve, far from taking action to slow the economy down, was already cutting rates in an effort to stimulate it further. An estimate of potential GDP that tells us that a weakening economy was in fact an overheating one is not an estimate that should be relied on for policy.

In 2016, the CBO said the economy was near potential and that unemployment, at 4.8 percent, would fall to just 4.5 percent before increasing and leveling off at 5 percent by 2020. Fortunately, policymakers did not move aggressively to rein in growth, and as a result, unemployment was able to fall another point-and-a-half through 2020.

If instead they had tried to keep growth within what the CBO thought were sustainable limits, 2.5 million fewer people would have had jobs in January 2020. And even then, we were not yet at full employment.

Underestimating potential output carries real risks, which policymakers need to take seriously. Depressed output and employment are serious and immediate problems. One of the most important results of “overheating” is wages rising relative to productivity. If real wage growth is never allowed to exceed real labor productivity growth, it is impossible for the wage share of national income to ever rise.

The CBO is too complacent about a persistent output gap.

As we have argued above, the CBO paints too bright a picture of where the economy is likely to be over the next few years, and too bleak a picture of where it will end up.

The challenge is clear for policymakers: There is still a large economic gap between their projections and full employment.

Even using the CBO’s estimate of a 3.9 percent minimum unemployment rate, by their estimate we will not reach that level for another five years. This implies an immense amount of avoidable hardship, insecurity, and wasted potential.

Elevated unemployment is particularly damaging for Black and Latinx people, who consistently face higher unemployment rates—currently 9.9 and 9.3 percent, respectively—than the national average of 6.7 percent. If unemployment stayed elevated throughout this period, Black and Latinx people would be the last to secure better jobs and higher wages: an inequitable and unacceptable outcome.

An immense amount of evidence over the past decade has shown that in an economy operating well below potential, deficit spending is an effective and reliable means of boosting demand. Indeed, this has become the overwhelming consensus view among macroeconomists.

Meanwhile, with interest rates still at zero, the Fed has limited tools available to boost demand. For this reason, Fed Chair Jerome Powell has repeatedly called on Congress to be more aggressive in the use of fiscal stimulus. Given that we have the tools to close the output gap quickly, there is no reason to accept the idea that the economy must remain depressed for many years to come.

Authors

Mike Konczal

Former Director, Macroeconomic AnalysisAs former director of Roosevelt’s macroeconomic analysis team, Mike Konczal led research focused on achieving full employment, building an economy that truly works for everybody, and developing the next generation of economic ideas.