What Record Quit Rates Really Mean

May 20, 2022

By Ira Regmi

In March 2022, 4.5 million people quit their jobs, up by 152,000 compared to February. In 2021, more than 47 million workers quit their jobs, up from the record high of 42 million in 2019. Corporations as well as journalists have deemed the current situation an unprecedented mass exit from the workforce, and taken to calling it the Great Resignation. However, coming off years of inequality and wage stagnation, what high quit rates really represent is a necessary reshuffling of jobs leading marginalized workers to pursue better working conditions and wages.

Journalists and economists alike have perversely called the Great Resignation an indicator of the economy running hot, almost ready to blow past full employment. Headlines have amplified increased rates of voluntary job quits as a case of disappearing workers, disenchanted by the idea of employment, and reluctant to reenter the labor market.

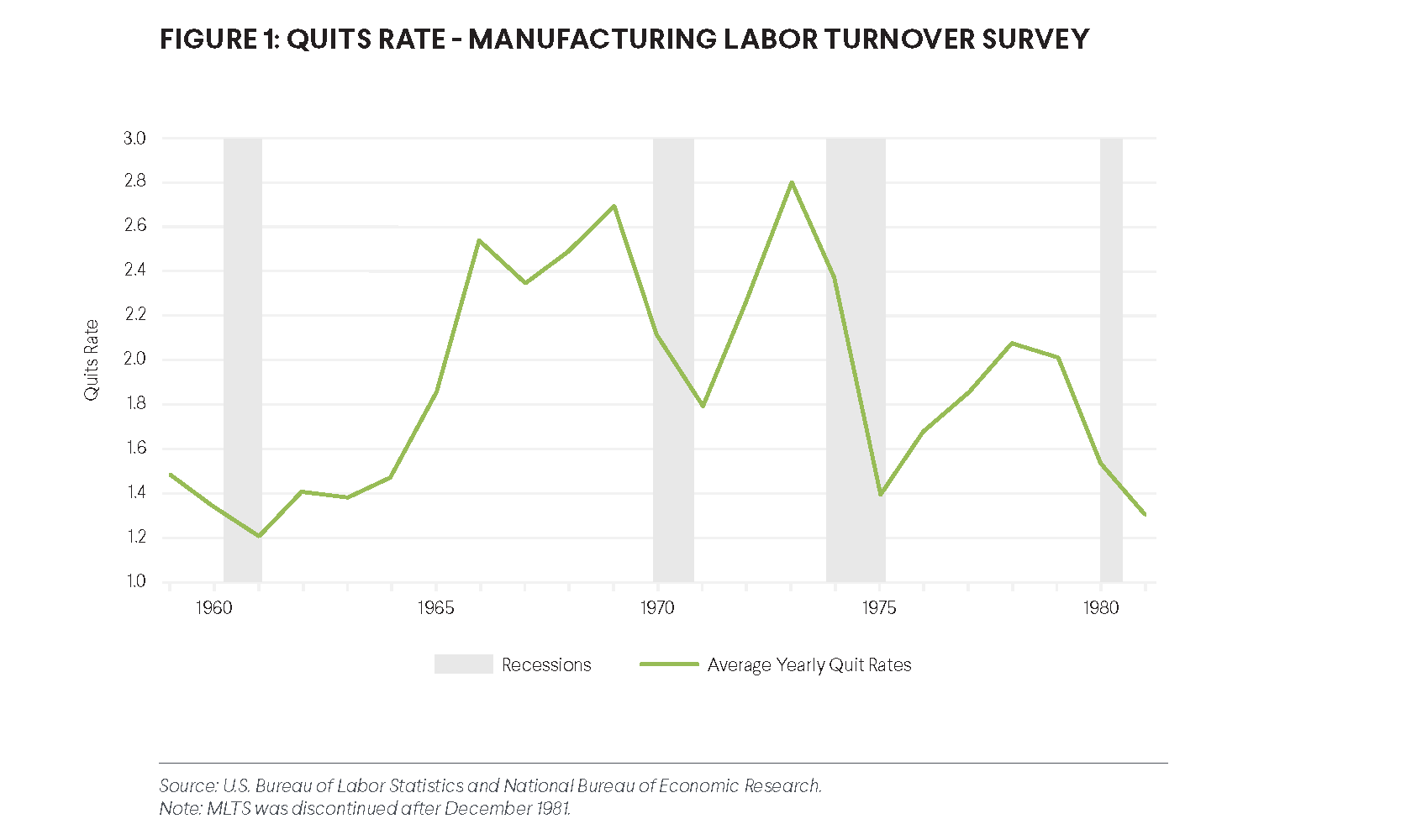

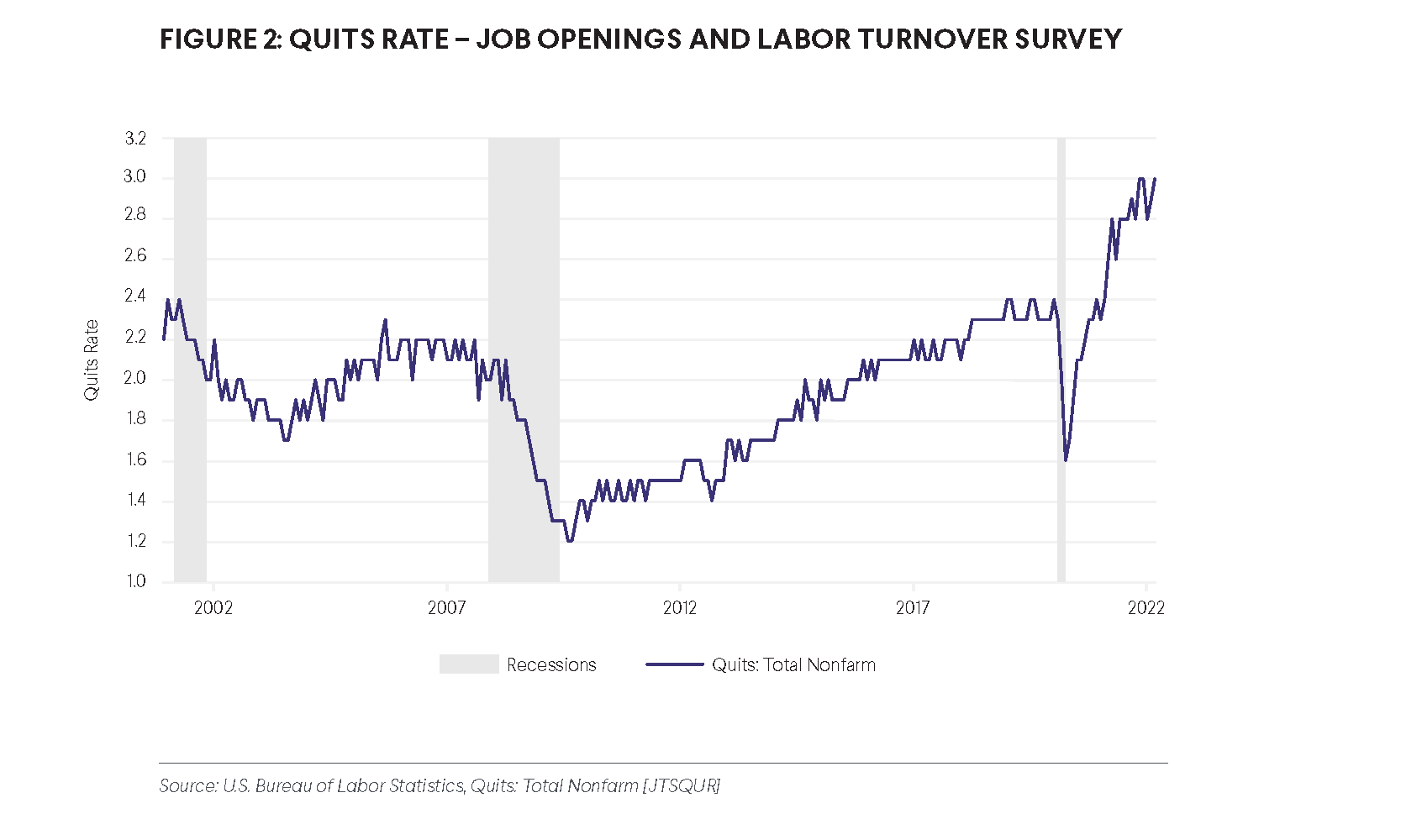

But given the current status of large race and gender gaps in employment levels, evidence suggests there is plenty more room for the job market to grow. As can be seen in historical data, increased quit rates are quite common during times of recovery. The claim that this phenomenon is unprecedented is true only because the numbers supporting the claim are being pulled from a source that goes back only to the 2000s: the Job Openings and Labor Market Turnover Survey (JOLTS). Observed in comparison to an older metric—the Manufacturing Labor Turnover Survey (MLTS), which covers the period from 1919 to 1981 and can be used as a proxy for the JOLTS quits—the current numbers are comparable to those of the 1960s and 1970s.

In fact, quit waves of varied magnitudes seem quite common during recoveries, as seen in the periods of 1948, 1951, 1953, 1966, 1969, and 1973. The Great Resignation in this regard is a quit wave proportional to the scale of the recovery from the pandemic-driven crisis. The higher quit rates in 2021 compared to the early 2000s can be attributed to a relatively robust recovery that, unlike the recovery of 2009, has not been a jobless one. As Ioana Marinescu has described, the 2010s were a unique period in which workers entered the labor market during sluggish times and found it harder to climb back up the job ladder from wherever they fell. The current quit rates and resultant vacancies, on the other hand, are an indication of much lower levels of scarring (i.e., the long-term effects of a recession).

While JOLTS enables us to distinguish voluntary separations, described as quits from other forms of involuntary separations like employer-led termination; it does not differentiate a job switch from an exit from the workforce. The difference between workers quitting to abandon the labor market altogether versus to seek other opportunities has crucial implications, as the latter is more likely to imply a tighter labor market where workers have higher bargaining power. A sharp decline in unemployment, as well as record growth in payroll employment, is generally an indication of a strong recovery with increased worker bargaining power. Therefore, we can reasonably speculate that these quits are motivated by workers’ inclination and ability to shop around for better opportunities and are not an indication of a supply crunch caused by large-scale withdrawal from the labor market.

In order to compensate for the limits of the data from JOLTS, Bart Hobijn constructs a more descriptive proxy for quits using Current Population Survey (CPS) data. The study demonstrates a positive correlation between the changes in quit rates from November 2019 to November 2021 and employment growth in the 12 months preceding November 2021. He also finds no significant increase in industry- or occupation-switching, which further rules out the possibility of workforce abandonment or industry-wide changes spurred by broader reconsideration of employment and career decisions by workers.

Other studies have also found correlations between quit rates and unionization levels, with the highest quit rates in states with the lowest union density. States where the share of the unionized workforce is below the national average of 10.3 percent saw above-average quit rates. Similarly, states with union density above the national average saw below-average quit rates. Low union membership often coincides with meager working conditions and low wages, creating a strong incentive—especially in times of recovery—for workers to seek out better jobs. Workers living in states with high union density are likely to be more satisfied with their present working conditions.

Together, the quits data, CPS proxies, and unionization rates paint a picture of a rather mundane and almost cyclical increase in quit rates in response to a necessary recovery, and are in no sense akin to a distress-worthy anomaly. The desire to sensationalize this phenomenon and interpret it as an indication of an attitudinal shift in workers benefiting from expanded fiscal stimulus during the pandemic is inaccurate, unconstructive, and especially harmful to already marginalized Black, brown, and queer communities.

Arguments for cooling down the economy because of a supposed Great Resignation that has stalled labor supply are missing some important points. Who is the economy working for? The unemployment rate for Black workers is still 5.9 percent—2.7 percentage points higher than white workers’ 3.2 percent rate—making it very likely that the economy will be slowed down before it confers any meaningful gains to marginalized workers.

The notion of a Great Resignation gives unwarranted validation to the current panic regarding the labor market and stigmatizes important tools of economic recovery, such as fiscal stimulus, childcare benefits, and unemployment insurance. Implicating signs of a strong recovery as the culprits of a labor supply shortage is counterproductive and hinders the goal of reaching full employment for all. We need to recognize this moment for what it is: an opportunity to boost working conditions and wages for those who’ve been left behind.

Authors