What Does Social Security Do?

August 14, 2025

By Oskar Dye-Furstenberg and Lena Bilik

Social Security is a form of social insurance. Participants pay into the program through federal payroll taxes, and in return they receive coverage against specific threats to their and their families’ economic well-being: old age, disability, or death. When one of these conditions is met, the program provides monthly monetary compensation to beneficiaries. The goal of Social Security is to mitigate economic risk, particularly the risk of poverty when someone loses their ability to receive market-based income through employment. All people age, and no one can foresee with absolute certainty when death or disability may occur. Because these events are inevitable, yet the timing is unpredictable, it makes sense to protect against them.

Social Insurance vs. Private Savings and Insurance

The National Academy of Social Insurance has articulated the ways that Social Security covers risks that private insurance is not equipped to handle. To begin with, social insurance is better suited for risks that surpass an individual’s capacity to control or plan for. For instance, if someone becomes disabled at a young age and lacks family support, they do not even have a chance to save enough to insure against their economic losses. Individuals can face similar challenges if a family member dies suddenly or if they live longer in retirement than expected. Many vicissitudes of life are simply beyond an individual’s capacity to prepare for alone.

Social insurance also does a better job of including vulnerable groups. Private insurers have an incentive to exclude high-risk people who are more expensive to insure, and social insurance lacks that incentive, allowing for fairer coverage. Providing coverage to such a large swath of society also allows for economies of scale that lower the administrative cost per insured person. In addition, social insurance, unlike private insurance, does not need to spend money measuring risk, maximizing low-risk participation, or advertising its services.

Moreover, social insurance is better suited for risks that exceed the timescales that a private company may be able to guarantee coverage for (like a working life of 40 or 50 years). Businesses come and go, but government programs can be guaranteed by law. Social insurance is also a more effective mechanism for risks that are concentrated, like when many workers become unemployed all at once due to an economic downturn. In that scenario, private companies may be overwhelmed by costs and unable to pay. Lastly, it is to our collective benefit for the government to limit the destitution that elderly, disabled, and unfortunate individuals may face due to lack of resources, unforeseen events, or limited familial means; Social Security benefits lift more people above the poverty line than any other program in the US, keeping them from needing additional government support.

What Does Social Security Provide?

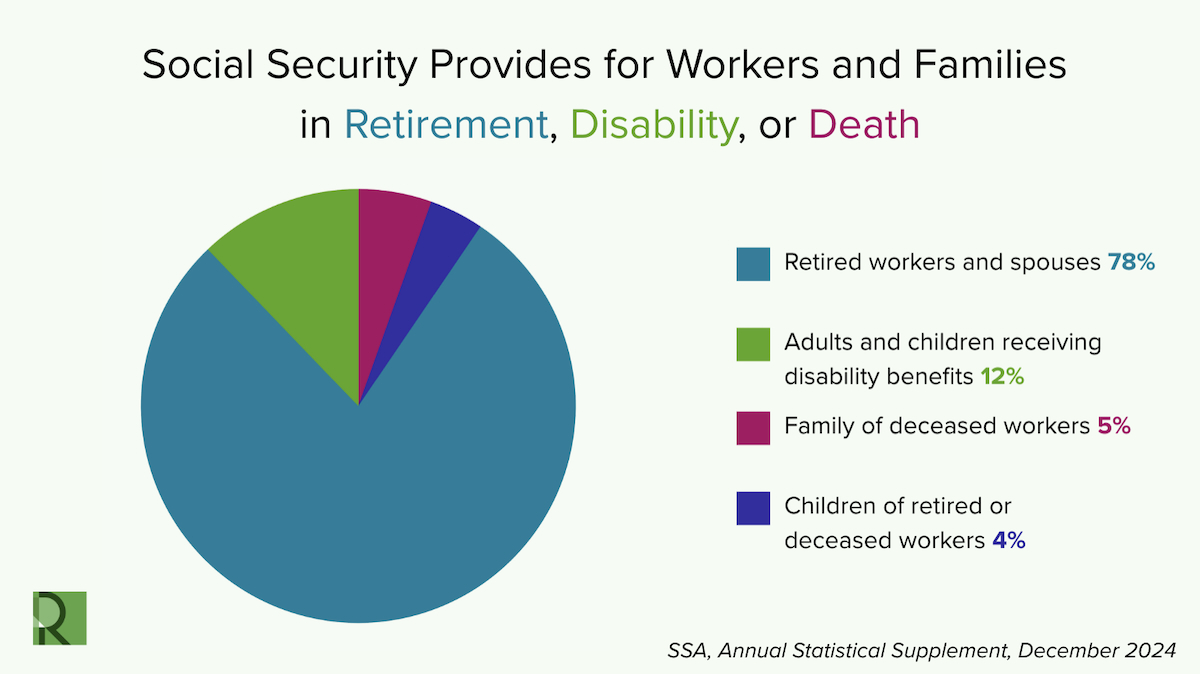

Social Security is a social insurance program run by the Social Security Administration (SSA), an independent federal agency. Social Security provides monthly payments to eligible persons in retirement, those with a qualifying disability, and to survivors or family members of people in these categories. Payments are primarily sent electronically via direct deposit or prepaid debit card. In March of 2025, President Donald Trump signed an executive order directing the Department of the Treasury to cease using paper checks by September 30, 2025, for all federal disbursements, including benefit payments.

Eligibility to enroll in the program is based on specific criteria. Old-age or retirement benefits are typically available to those who have paid social security taxes for 10 or more years. Recipients can claim benefits beginning at age 62, but they will only receive 70 percent of the benefit. The percentage increases fractionally for every additional month that retirement is postponed, until the “full retirement age,” when 100 percent of the benefit amount can be claimed. Currently, this age is 67 for those born in 1960 or later (but lower for those born earlier).

The specific benefit amount is determined by calculating the average of an applicant’s highest 35 years of earnings, indexing this figure to wage growth, and updating annually according to price inflation as measured by the Consumer Price Index.

Social Security also provides income to the family members of those who receive old age and retirement benefits. Under specific conditions, spouses as well as children or other dependents are eligible to receive family benefits, which provide a portion (typically half) of the amount of the benefit received by their family member.

Survivor benefits are available to family members of a deceased worker who was eligible for Social Security. A surviving child or a spouse with a child under the age of 16 gets 75 percent of the worker’s benefit amount. Surviving spouses between age 60 and the full retirement age get between 71 percent and 99 percent, while those at full retirement age or older will generally receive the full amount. Social Security will pay a maximum of between 150 percent and 180 percent of a deceased worker’s benefit amount to a surviving family.

Social Security also pays benefits to those who can’t work because of disability, given that certain qualifying conditions are met. These benefits are provided through Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI). The SSA determines eligibility for disability benefits based on enrollees’ earnings history, length of work, and age at which the applicant developed their qualifying disability. Broadly, the older someone is when they develop their disability, the longer they are required to have worked in order to be eligible. Like old age and retirement benefits, disability benefit amounts are calculated using an average of the beneficiary’s earnings indexed to wage growth, then adjusted for inflation. Once recipients reach the full retirement age, their disability benefits convert to regular retirement benefits. This transition should generally not alter a recipient’s benefit amount unless they received workers’ compensation or other disability benefits that can reduce SSDI payments. In addition to workers, disabled children are eligible for benefits, as are certain family members of a disabled worker.

The Importance of Social Security

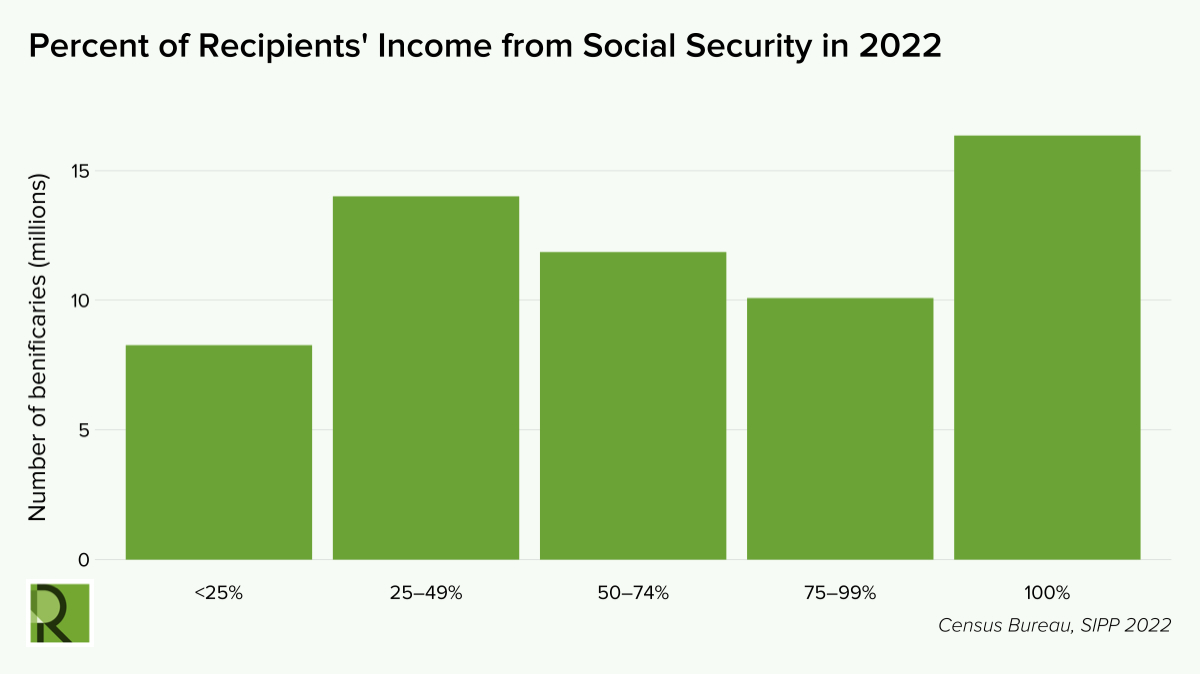

Social Security income is vital, protecting millions of Americans from economic hardship and poverty. In May of 2025, over 69 million people received some form of old-age, survivors, or disability benefits from Social Security, totalling over $129 billion. The most recent Census Bureau Survey of Income and Program Participation (SIPP) showed that, in 2022, Social Security constituted 75 percent or more of income for almost half of recipients, or over 26 million people. For over a quarter of recipients—more than 16 million people—Social Security constituted 100 percent of their income (see Figure 2 below). In addition, approximately 87 percent of people aged 65 and older receive Social Security, with these benefits constituting nearly a third of income for this group. The census survey further reported that more than 3.5 million children received Social Security payments in 2022.

The program’s overall effect on poverty reduction is significant. The Center on Budget and Policy Priorities reported that, in 2023, Social Security kept over 22 million people from falling below the federal poverty line. Research from the National Bureau of Economic Research finds that Social Security reduces the elderly poverty rate by 75 percent. In addition, Social Security lifted 959,000 children above the poverty line in 2023. For these reasons and more, the National Academy of Social Insurance calls Social Security “the most successful anti-poverty program in the United States.”

Demographic Considerations

Social Security is a vital engine for economic equity and poverty reduction, given its positive impact on people with disabilities, women, and people of color.

Many Americans with disabilities rely solely on their Social Security or SSI benefits and corresponding health coverage for basic day-to-day survival. This is not an insignificant number of people; for an insured worker who was 20 years old in 2022, the probability of becoming disabled between age 20 and the normal retirement age was 25 percent. In 2023, disability benefits were paid to more than 8.7 million disabled beneficiaries (disabled workers, disabled surviving spouses, and disabled adult children). Social Security benefits are critical lifelines for many people who are excluded from the economic security of employment to be able to live with dignity and safety.

Social Security is especially important for women, bringing 9.4 million older women above the poverty line. Because of systemic gender discrimination, women take more time off from paid work for caregiving responsibilities and face a persistent pay gap, leading to fewer savings and smaller pensions than men. And because women tend to live longer than men, they make up a large proportion of older people on Social Security; more than half of Social Security beneficiaries in their 60s and 7 in 10 beneficiaries in their 90s are women.

Social Security is also particularly important for Black and Latino workers, who are more likely to face poverty both during their working lives and in old age. These inequities are due to the negative impacts of systemic racism on economic and employment opportunities, as well as lower generational wealth. Black and Latino older adults are less likely to have workplace retirement plans and more likely to work low-income jobs, leading to less savings over time. Social Security helps address those inequities among these populations as they age. Without Social Security, the poverty rate among older Latino and Black adults would be nearly half (Instead, the poverty rate is 17.4 percent and 17.3 percent, respectively—which is still more than twice the rate of poverty among older white people.) Additionally, workers of color are particularly served by disability benefits, because Black and Latino workers are more likely to become disabled before reaching retirement age than white workers are (again, because of systemic racism’s impact on access to health care, food, affordable housing, and economic opportunity).

Is Social Security different from Supplemental Security Income? Yes. While the Social Security Administration also administers SSI, which provides monthly payments to those with minimal income or economic resources, SSI is distinct from Social Security, which provides general social insurance. Furthermore, the two programs have different funding sources. Social Security is funded primarily by payroll taxes, income taxes on the Social Security benefits of the highest-income earners, and investment returns from the accumulated assets of the program (known as the Social Security trust fund). SSI is funded by government revenue.

Is Medicare part of Social Security? Medicare provides health insurance for persons who are age 65 or older, have end-stage renal disease (ESRD), have amyotrophic lateral sclerosis (ALS), or get Social Security Disability Insurance benefits. Though Medicare is run by the Centers for Medicare & Medicaid Services, the SSA handles enrollment and collects premiums for many Medicare beneficiaries. Medicare relies on separate revenue streams from Social Security, other than a small portion of its funding that comes from taxes on the Social Security benefits of high-income earners.

What else does the SSA do? The SSA assists in the administration of programs run by other agencies. These programs include Medicaid, the Supplemental Nutrition Assistance Program (SNAP), federal benefits for veterans, and more.

Related Resources

Authors

Oskar Dye-Furstenberg

Senior Research AssociateOskar Dye-Furstenberg is a senior research associate at the Roosevelt Institute where he supports think tank staff and fellows in their research.

Lena Bilik

Program ManagerAs program manager, Lena supports think tank staff and fellows with research and project management.