Can China Break Nuclear Power’s Cost Curse—and What Can the US Learn?

September 17, 2025

By Shangwei Liu

This piece is part of a new blog series that explores the approaches various countries and industries are taking to implement clean energy technology and facilitate large-scale decarbonization.

Roosevelt Institute Director of Industrial Policy and Trade Todd N. Tucker sets the stage for the first installment:

The US and global economies are at a turning point. After a few years of the Biden administration going big on an “all-of-the-above” approach to the technologies that could be used for the energy transition, the second Trump administration has taken more of a “picking-winners-and-losers” approach, with nuclear in the former category and solar in the latter. But the rest of the world is not standing still, with countries like China continuing to leap ahead on a wide range of decarbonizing technologies.

We’re launching a periodic blog series to better understand how different countries and industries are attempting to meet the moment—and what we can learn from these experiences. We are particularly interested in learning more about technologies that have polarized public opinion in the past or present, but which are likely to play an important role in attempts to navigate big structural changes in the economy. I can’t think of a better author or topic to kick us off than Shangwei Liu, one of the top emerging scholars of how China is navigating the energy transition, writing about nuclear power. Liu , gives us insight into a recent piece in Nature he coauthored with Gang He, Minghao Qiu, and Daniel M. Kammen on the construction costs of nuclear power.

One of the main takeaways, for me: Industrial policy can be wildly successful for transitioning to renewable energy while also deepening domestic supply chains, as “Buy American” in the US context or “indigenization” in China shows. However, for all the seeming novelty of these new or revived types of government intervention in markets, countries can also seek advantage through means that are as old as capitalism itself: low wages. While Liu casts doubt on that factor being the primary explanation here, figuring out high-road strategies that boost wages while also building competitive industries is a key challenge in building a truly progressive abundance agenda.

Governments and tech giants are once again placing big bets on atomic energy. In the US, the White House and Department of Energy are pushing forward efforts to streamline reactor licensing, aiming to quadruple nuclear capacity by mid-century. France, Italy, the UK, and many emerging economies have announced new plans for nuclear expansion. Meanwhile, companies like Amazon, Google, and Microsoft are turning to nuclear to meet surging electricity demand driven by AI.

But despite renewed interest, the sobering reality is that most countries have barely built any new nuclear plants since the 1990s. In the US, only three new reactors have come online in the past three decades. While public debate often centers on safety and waste, the fundamental reason for the stall is simple: Nuclear is too expensive to build.

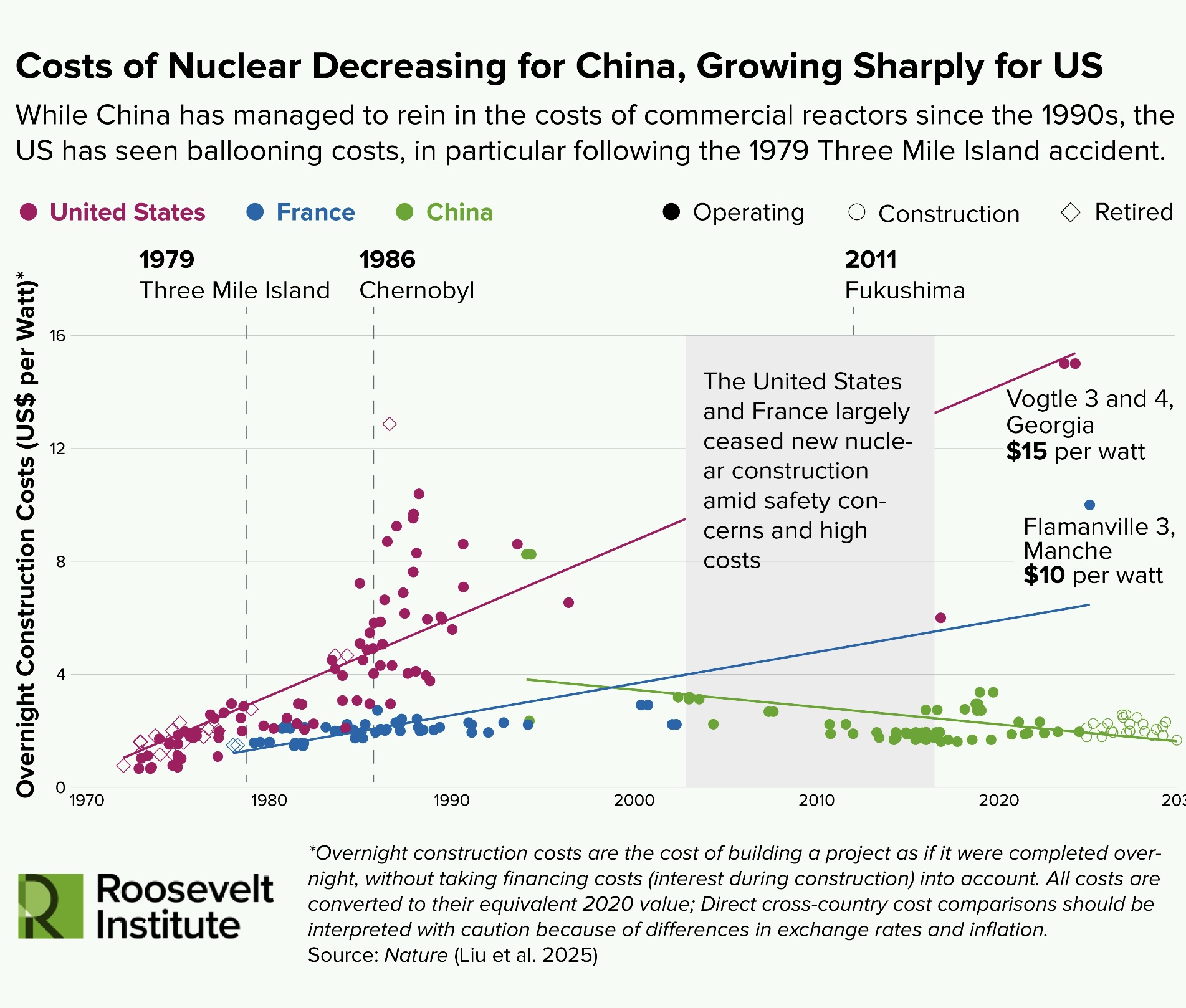

Although nuclear power was once promised to deliver electricity “too cheap to meter,” construction costs have consistently risen in most countries, including the US, France, Canada, and Japan. The increase was most dramatic in the US, where overnight construction costs (upfront capital costs excluding financing costs) rose from $1–2 per watt in the early 1970s to $4–10 by the late 1980s (in 2020 dollars). The recently completed Plant Vogtle in Georgia topped $15 per watt after more than a decade of delays. Financial costs also soared, driven by longer construction timelines and heightened investment risks, overwhelming savings from a global decline in interest rates since the early 1980s. Figure 1 shows the declining costs of nuclear construction in China in contrast with the rising costs in the US. France serves as an additional point of comparison.

Why is nuclear power so costly?

Several factors are widely believed to account for the cost escalation. In the US, rising labor and material costs were key contributors. The US market’s reliance on custom-built reactors further hindered standardization and blocked economies of scale. Safety regulations became more stringent, especially after the 1979 Three Mile Island accident, triggering frequent design changes and rework. Combined with a deteriorating supply chain, these disruptions caused delays, pushed up labor demand, and reduced productivity. One study of nuclear cost drivers found that labor productivity losses were a major factor: Workers were idle for as much as three-quarters of scheduled hours, mainly because of poor construction management such as missing materials or tools, overcrowded worksites, and scheduling conflicts among different trades.

Nuclear power’s cost escalation is often described as a curse. While most energy technologies, such as wind, solar, and batteries, get cheaper with more deployment, nuclear has been the exception. Paradoxically, building more reactors has often meant higher, not lower, construction costs.

Whether this “cost curse” is inevitable remains a long-standing debate. Some argue it stems from the nature of nuclear itself—large-scale, risky, and complex—making it resistant to the kind of learning in other energy industries in which additional experience drives down costs. Others contend that with stable regulations and standardized designs, nuclear costs can decline over time.

Recent developments in civil nuclear power may shed new light on this long-running debate. One country stands out as a counterexample while most others scale back: China. Over the past two decades, it has been the only nation to consistently and significantly expand its nuclear fleet, with 58 reactors now in operation. Between 2022 and 2025, China has approved an average of 10 new reactors per year and is on track to surpass the US as the world’s largest nuclear power producer by 2030.

How did China pull this off, and with what cost trajectory?

Our new study, recently published in Nature, compiles and analyzes plant-level data from a wide range of public sources. We find that China’s nuclear construction costs declined sharply in the 2000s, remained stable through the 2010s, and have avoided the dramatic cost increases seen in the US.

I was genuinely surprised when I first saw this trend. Does this suggest that the cost curse of nuclear energy is breakable, and that China may have found part of the remedy? The answer is that China’s new data offers a very mixed picture for both nuclear optimism and pessimism, and I believe we should be cautious in drawing broad conclusions from it.

On the one hand, our results show that nuclear costs don’t inevitably rise with scale. It is possible, at least to some extent, to rein in the cost escalation that has plagued other countries. Our results also confirm that regulatory stability and coordinated industrial policies played important roles in China’s successful build-out of nuclear power.

But on the other hand, our findings also highlight that the learning curve in nuclear construction differs fundamentally from that in solar and wind. Cost reductions are largely limited to the initial several units and do not result in a continuous decline. More experience with the same reactor design does not necessarily lead to much lower costs. This challenges assumptions from some engineering studies, which posit that building 10–15 units sequentially will lead to significant, continuous cost declines.

In fact, we find that China’s recent shift to advanced reactor designs, many of which are still under construction, has actually pushed costs upward. This highlights the need to balance cost control with other critical objectives, such as innovation and safety.

More importantly, we need a deeper understanding of the forces driving nuclear construction costs, whether in the US, China, or elsewhere. In China’s case, our research finds a strong correlation between rising domestic content (materials and inputs) and falling construction costs. Numerous news reports and anecdotal evidence further support that replacing foreign equipment with Chinese domestically produced components has substantially reduced nuclear costs. This suggests that indigenization—i.e., building a domestic supply chain and skilled workforce—has been key to China’s ability to avoid cost escalation. This may also explain why, in both China and South Korea, when a unit’s domestic content rate exceeds 75 percent, its costs appear to stabilize.

Why does indigenization make Chinese nuclear power cheaper—and can other countries replicate it? Several factors may be at work: labor costs, economies of scale in supply chains, financing, explicit or hidden subsidies. But the available data make it difficult to pin down the exact mechanism.

Solar provides a useful comparison. A previous study of US and Chinese solar panel costs found that China’s edge stemmed less from cheap labor or subsidies than from massive manufacturing scale and the supply-chain efficiencies that followed. In other words, if the US could expand solar production to Chinese levels, American-made solar panels could be nearly as inexpensive. The broader lesson is that lowering the cost of clean technologies may hinge less on wages or subsidies than on whether—and how—an industry can scale enough to unlock supply-chain efficiencies.

What can the US learn?

For nuclear power in the U.S., that suggests two critical tasks. First, rebuild the industry and its supply chain at scale. Second, curb cost escalation through stable regulations and standardized designs.

There are reasons for optimism that both are possible. The broader zeitgeist around nuclear power is shifting. Public support for nuclear energy has been rising and has stayed above 50 percent since 2021. That support is also bipartisan. After two decades of flat electricity demand, consumption is climbing again—driven by AI, data centers, and electrification—drawing new investment in firm, low-carbon power. Streamlining regulatory frameworks and emerging financial models could further help jump-start a US nuclear revival.

Another relevant trend is that China and the US are pursuing very different technological paths to maintain or rebuild their nuclear industries. In China, the strategy is clear: deploy advanced large reactors over the coming decades to supply the national grid.

In the US, the technological direction remains uncertain. Some advocate for continuing with proven large reactors, replicating the recently completed Vogtle AP1000 units at scale in hopes of driving down costs. But there is little clarity on how this would work in practice, both from a business and institutional standpoint.

Others, including tech giants and new nuclear start-ups, are betting on emerging small modular reactors (SMRs). Their modular design may enable factory-based production of key reactor components, potentially avoiding the high cost overruns and delays associated with large, site-built reactors. However, most SMRs remain paper designs. They lack economies of scale, are currently far more expensive, and face major questions: When, how, and at what cumulative cost can SMRs become commercially viable?

Without greater clarity on the technological roadmap and stronger alignment on how to rebuild supply chains, much of today’s enthusiasm for a US nuclear revival risks remaining little more than hot air.

Author

Shangwei Liu

Guest AuthorShangwei Liu is a postdoctoral research fellow at the Belfer Center for Science and International Affairs at the Harvard Kennedy School.