Few Signs of Immediate Change in September Jobs Data, but Broader Concerns Remain

September 3, 2025

By Michael Madowitz

August has been a structurally chaotic month for economic policymaking. But despite the erratic moves—firing the head of the Bureau of Labor Statistics (BLS), which produces both jobs and inflation data, and a historic power struggle over the Federal Reserve—the policy stakes for this Friday’s jobs data are surprisingly low. The odds that the Fed will cut rates by a quarter point are currently over 90 percent, just above where they’ve been for the month since August data revisions showed weaker job growth than previously reported. Forecasts for this month’s jobs report are about what they have been for the past few months.

There are real risks to the economy—higher and more uncertain tariffs, risks to the monetary policy independence of the past 100 years—but they are more of the structural, long-term variety. In the short term, the unusually negative revisions to employers’ reports of job growth last month are a cause for concern and for heightened focus on this month’s numbers. The short-term signals matter, but the larger story is how these immediate cracks connect to longer-term risks that could reshape growth and worker power.

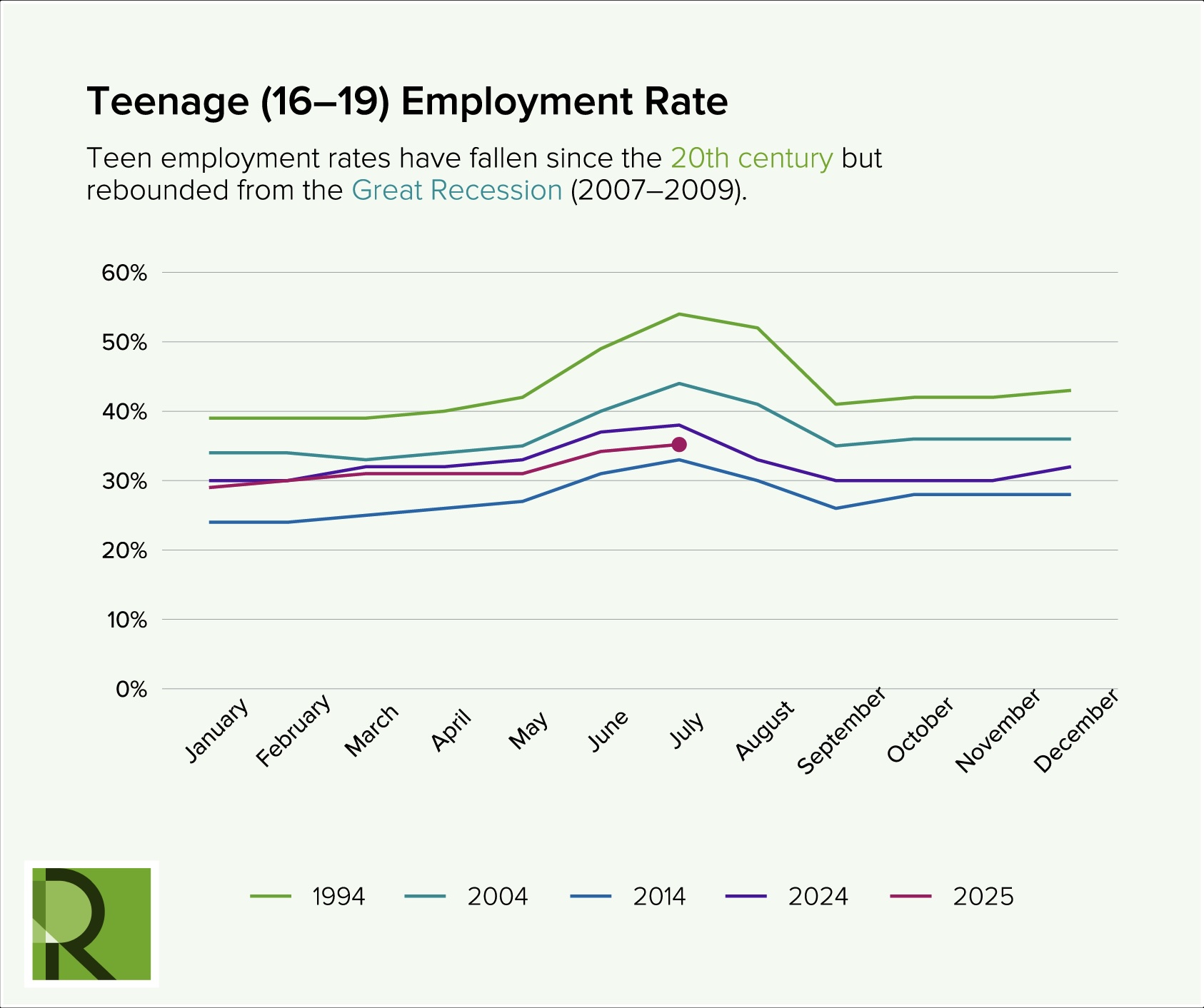

Across an economy that’s been cooling since the global freakout over inflation, the risk is that the US has chosen slower growth and a weaker job market that shifts power toward employers. Long-term unemployment is rising back toward levels where wage growth slows down. A dramatic slowdown in immigration means the economy will grow more slowly as the workforce shrinks and as falling demand—a result of less spending by working immigrants—reduces hiring. The labor market is softer in ways that look both structural and cyclical, with teenage employment set to turn in its weakest May–July surge on record.

Source: Bureau of Labor Statistics (via FRED)

This looks less like a rapid onset of a recession than a time to rethink how policy should work when one next occurs. The US currently has much higher tariffs than it has in recent history, the Fed is under more political pressure than at any recent point, and tax revenues are even lower than last time, so any fiscal response will face debt and inflation concerns. There is little margin for error, so these discussions need to start soon. The response to the last crisis—including the American Rescue Plan—proved how quickly strong policy can restore growth and protect workers. But today, fiscal space is narrower, and the margin for error smaller, which is why policymakers need to start reimagining their available policy options now.

Author