May Jobs Report Puzzles to Come

May 30, 2025

By Michael Madowitz

Next week, we’ll get the first jobs data to reflect the damage done by the so-called Liberation Day tariffs. Intuitively, we should look for significant effects in multiple sectors that are heavily exposed to trade, including sectors like transportation and warehousing, but less appreciated are the risks to sectors that are highly sensitive to global economic conditions, like energy, which are impacted by a secondary effect of tariffs—a slowdown in global growth.

These two broad groups of sectors are worth keeping an eye on, in part to see what is most affected by the delayed economic activity that followed the implementation of these tariffs as well as to assess the potential impact of more moderate tariffs that remain in place and seem likely to slow the economy for the foreseeable future.

Domestic manufacturing more broadly relies on a lot of intermediate goods—many of which are imported—so durable goods producers could show slowing job growth in May, and in coming months, due to both softening demand and higher input costs.

But most exposed to tariff impacts are consumer-facing manufacturers, who must confront a demand-side hit from slowing growth and higher costs on the supply side. Auto production, along with most durable goods manufacturing, is cyclical. But automakers face a near-perfect storm: being exposed to higher input costs, a growth slowdown, and higher interest rates. Of course, this storm is not unique to automakers or manufacturers: Residential construction—among others—also faces cost, demand, and interest rate risks.

Some cyclical patterns change over time. For example, as the US went from a major energy producer to a net oil importer and then back to a net exporter again, the correlation between employment in “mining and logging,” which includes oil and gas, moved from positively to negatively correlated with GDP growth and back again. The downturn in expectations for global growth since “Liberation Day” has depressed oil prices and may impact US energy jobs very soon.

Other industries that are heavily dependent on exports are also likely to show trade impacts, even if tariffs do not implicate them directly. While nonfarm payrolls can’t show a direct hiring impact from agricultural trade barriers, industries like food manufacturing and fishing are significant exporters and are reported in monthly jobs numbers.

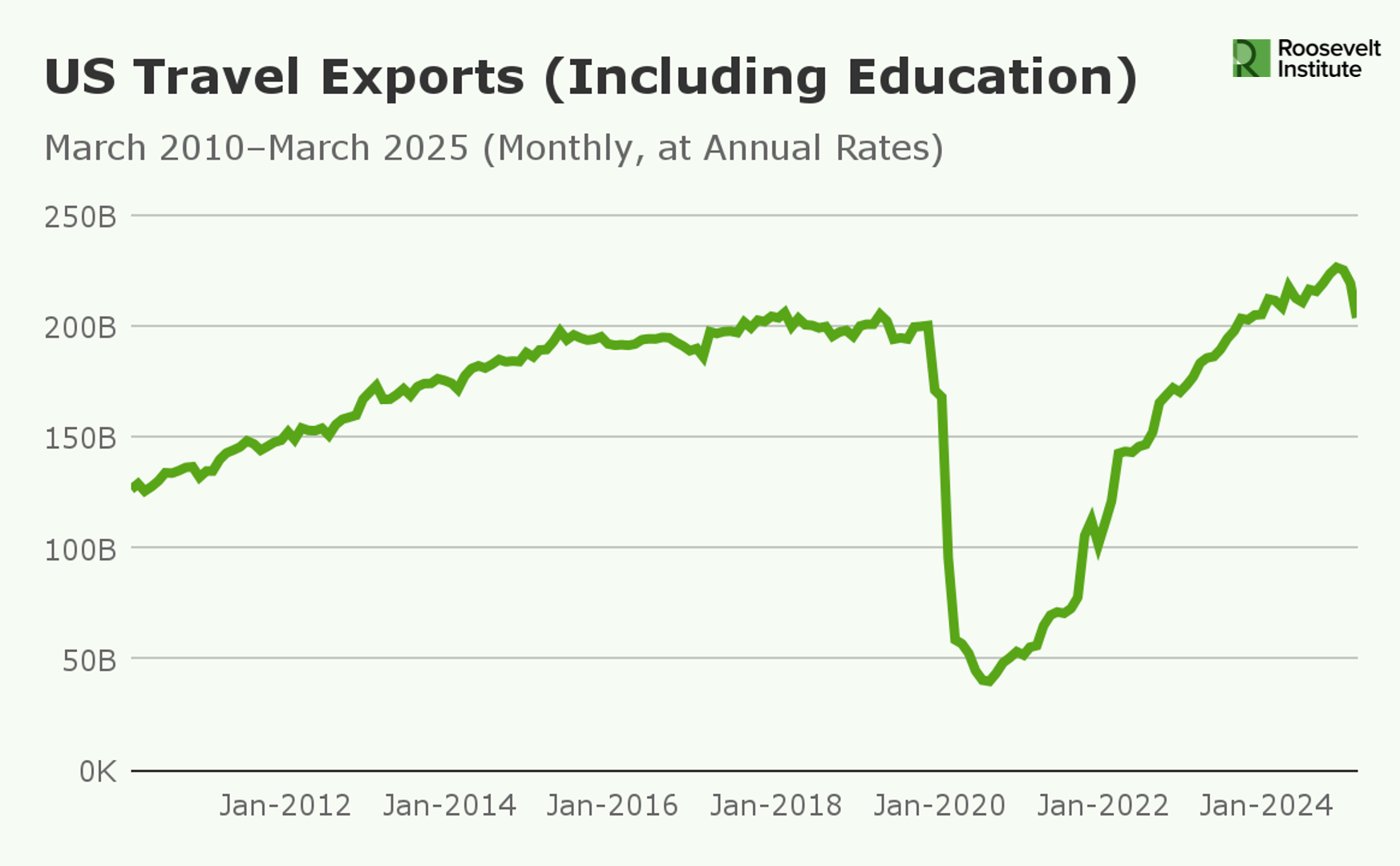

And though exports are not subject to retaliatory tariffs from adversaries yet, some of the United States’ largest export sectors are affected by other administration policies in addition to tariffs. The $215 billion in exports the US gets from foreign tourists visiting the country is expected to shrink considerably this summer, putting pressure on 14.3 million accommodation and food services jobs. While education hiring is unlikely to be as deeply affected in the next few months, exports in this sector have declined dramatically in 2025 so far (see graph above), and job losses for the 4 million private education workers as well as the 2.6 million state government education workers—who are concentrated at colleges and universities—seem likely if this downturn is not reversed.

Top-line jobs numbers in export industries can give some signals about the impacts of tariffs, but economy watchers shouldn’t read too much into this month. The first impacts of the administration’s policies are unlikely to be the most persistent or most important. The bigger concern, this month and through the end of 2025, will be knock-on effects materializing in other indicators from the real economy.

Author