Leading with Industrial Policy: Lessons for Decarbonization from Swedish Green Steel

February 12, 2024

By Jonas Algers

"State-owned entities can play a key role in strategically pursuing decarbonization objectives independently of short-term shareholder value maximization."

Introduction

Heavy industry is characterized by significant inertia and path-dependency, locking in unsustainable use of fossil fuels. Steel is a major industrial subsector, emitting 7 percent of global energy system emissions in 2019—10 percent including indirect emissions (IEA 2019). However, two “green steel” projects located in Northern Sweden are showing a way out of fossil lock-in; one is the Hydrogen Breakthrough Ironmaking Technology initiative—known as HYBRIT—and the other is the start-up H2 Green Steel. In this essay, I will trace the role of policy in enabling these two projects.

Globally, about 70 percent of steel is produced through what is called the primary route, using iron ore as the main input. This route reduces iron ore to iron, and later this iron is smelted together with other materials, turning it into the alloy steel. About 90 percent of primary steelmaking uses a blast furnace (BF) to reduce the iron ore into iron and a basic oxygen furnace (BOF) to turn iron into steel. Coking coal is used as a reductant in the BF, making this route emission-intensive, producing almost 3 tonnes of CO2 per tonne of steel directly and indirectly (IEA 2022). The remaining 30 percent of global steelmaking is done through the secondary route, using scrap as the main input and smelting the scrap in an electric arc furnace (EAF). This is a much less emission-intensive process, producing under 0.3 tonnes of CO2 per tonne of steel, most of which arise from electricity used. However, limits to availability and quality restrict the scope of scrap-based steel, making new, low-emission primary production processes necessary (IPCC 2022a).

The process detailed in this essay is the hydrogen direct reduction route, which produces direct reduced iron (DRI) that can later be smelted in an EAF, called the H-DR-EAF route (Vogl et al. 2018). Using green hydrogen from renewable energy as a reductant, hydrogen-based steelmaking can reduce emissions from primary steel by 95 percent compared to the BF-BOF baseline, and remaining emissions are a smaller innovation challenge (Vogl and Åhman 2019).

There are currently two hydrogen-based primary steel projects in Northern Sweden, the HYBRIT initiative and the start-up H2 Green Steel. HYBRIT is a joint venture between Swedish power utility Vattenfall, miner LKAB, and steelmaker SSAB. SSAB plans to replace its BFs in Sweden and Finland with a current steelmaking capacity of 6.4 million tonnes per annum (mtpa) with EAFs fed with DRI from LKAB which takes over the reduction step. This will remove about 8 million tonnes of annual CO2 emissions by 2030—10 percent of Sweden’s total emissions plus 7 percent of Finland’s emissions (SSAB 2022). However, the largest contribution to global emission reductions from HYBRIT is miner LKAB exporting direct reduced iron rather than iron ore. Currently, LKAB produces 80 percent of the European Union’s iron ore, and LKAB’s decarbonization plan will reduce annual emissions by 40 to 50 million tonnes, equivalent to Sweden’s total territorial emissions (LKAB n.d.b).

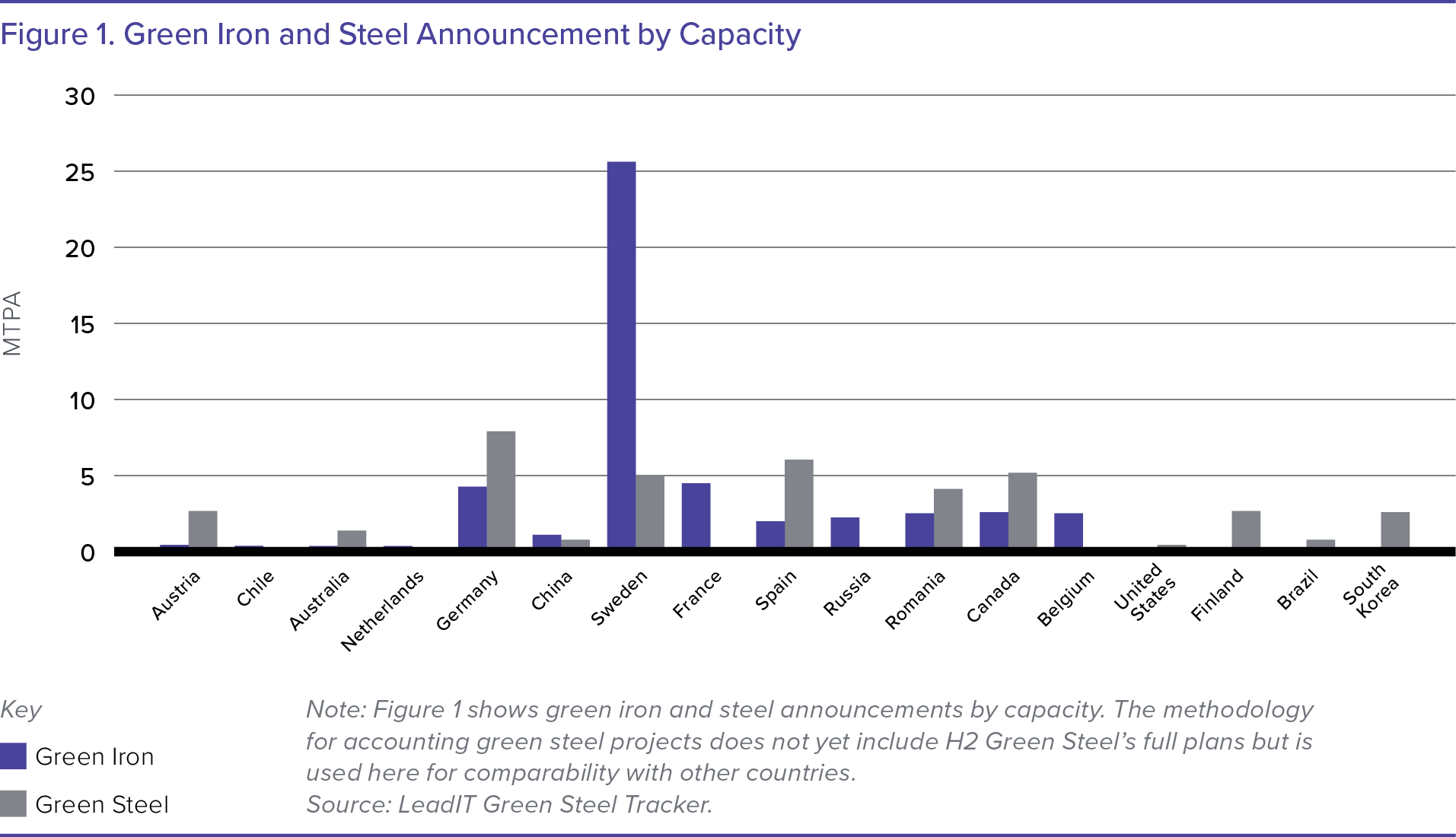

The second project is the start-up H2 Green Steel (H2GS), which plans to produce 2.5 mtpa by 2025 and 5 mtpa by 2030. H2GS was started by venture capitalist Harald Mix, who is also a key player behind Swedish battery maker Northvolt and is led by Henrik Henriksson, formerly CEO of Swedish truck manufacturer Scania. H2GS will expand Sweden’s steel capacity from 4 to 9 mtpa, aiming to replace emission-intensive, fossil-based steel abroad. These projects have propelled Sweden to the top of the globe among green iron and steel announcements, as can be seen in the figure below.

These two projects have very different profiles. H2GS is a start-up that has neither been publicly listed nor produced a single tonne of steel yet, while HYBRIT is a joint venture of 100 percent state-owned Vattenfall and LKAB, which in turn is the largest shareholder of SSAB. SSAB has produced steel for over 40 years while LKAB has produced iron ore for more than 130 years. SSAB was founded when the government restructured the steel industry in response to the steel crisis of the 1970s, and LKAB became a key shareholder when SSAB was listed in 1989.

However, the differences between these two projects show how distinct types of actors—with different types of state involvement—can play complementary roles across the same innovation system.

Why has Sweden reached a globally leading position on iron and steel decarbonization? And what has been the role of industrial policy in enabling the transition away from fossil-based steel? In the next section, I present how the Swedish steel sector moved toward hydrogen-based steelmaking. In the third section, I discuss the key policies that have mobilized finance for these projects. Finally, I draw conclusions for industrial policy supporting deep industrial decarbonization in the US steel industry.

The Climate Policy Framework

After the Paris Agreement was signed in 2015, the Swedish parliament agreed on a Climate Policy Framework binding parties from the Left and Right to long-term climate targets (Klimatpolitiska rådet, n.d.). The target set out in the Climate Policy Framework is to reach net-zero emissions by 2045, and net-negative emissions thereafter. This was a clear change in Swedish climate policy, as it committed both the Right and Left to policy not merely for reducing emissions, but for deep decarbonization. This Framework therefore set a clear marching order—or direction (Nilsson et al. 2021)—that Swedish companies should develop their business in line with zero emissions over the long term. For steel, that is a significant difference, as energy and material efficiency within a fossil-based system cannot reach net-zero emissions, instead requiring new production processes (even with carbon capture utilization and storage [CCUS], BF-BOF steelmaking still cannot reach sufficient emission reductions [Vogl and Åhman 2019]). In addition, the government launched a program for decarbonization called Fossil Free Sweden (Regeringen 2016) to coordinate business initiatives by sectors and institutionalize a relationship between government and business in which business could communicate policy needs to achieve the government’s targets, improving what political sociologist Peter Evans calls the “embeddedness” of the state with business (Juhász et al. 2023).

With the Paris Agreement signed and the Swedish Climate Policy Framework in place, SSAB had to consider how to respond to the push for long-term decarbonization. For a long time, carbon capture and storage (CCS) had been the favored route in the steel industry, despite CCS being insufficient in fully decarbonizing steel due to low capture rates (ICCP 2022a; IEA 2022). However, SSAB’s problem was that its coking plant (which turns coal into coke to be used in the BF) in Oxelösund had failed environmental permits due to air pollution and had only received an exemption until 2027 (Mark- och miljödomstolen 2019). Both retrofitting its plants with CCS and building a new coking plant was not appealing to SSAB, as it would lock in fossil fuel use without any realistic prospects to reach parliament’s target of zero emissions.

Renewable Energy Cost Declines Enable Hydrogen-Based Steelmaking

While problems with CCS persisted, hydrogen-based steelmaking was a known alternative among key players at SSAB, including CTO Martin Pei. But while the hydrogen route was a familiar idea, it hadn’t been tried at scale, as it requires vast amounts of electricity to replace energy derived from coal, increasing costs and making green steel uncompetitive.

However, with the cost declines for renewable energy seen in the 2010s, this problem was becoming surmountable. Studies found that future costs would be up to about 20 percent higher per tonne of steel produced in the H-DR route than in the BF-BOF route, highly subject to electricity costs (Material Economics 2019; Vogl et al. 2018). Northern Sweden’s ample hydropower and significant wind power opportunities therefore give the region significant competitive advantages for hydrogen-based steelmaking. In addition, as steel is an intermediary input, cost increases for green steelmaking were found to be minor for final goods, ranging from about 0.3 to 2.1 percent of total costs (Delasalle et al. 2022; Rootzén & Johnsson 2016). Because hydrogen-based steelmaking requires a different value chain, using electricity over coal and DRI rather than iron ore, SSAB reached out to miner LKAB and power utility Vattenfall to integrate the rest of the value chain in its plans and to coordinate a transition. LKAB produces 80 percent of the EU’s iron ore and almost all of Sweden’s iron ore, and Vattenfall owns 41 percent of all power capacity in Sweden (Lejestrand 2023). Getting both of them on board for decarbonizing steel was key due to the companies’ significant influence on the innovation system as a whole.

Importantly, hydrogen-based steelmaking was also a way to please LKAB’s and Vattenfall’s owners: the state. Both companies are 100 percent state-owned, and the state had set a clear direction toward decarbonization. In 2016, as the Climate Policy Framework was being developed, Vattenfall announced an “action plan” for emission reductions that included the sale of coal assets, and an intention to focus on “enabling customers to reach their climate targets” (Vattenfall 2016), meaning businesses purchasing power from Vattenfall such as iron and steelmakers.

HYBRIT

Together, SSAB, LKAB, and Vattenfall launched HYBRIT, creating a common research platform to decarbonize the entire iron and steel value chain. Meanwhile, the government set up the The Industrial Leap (Industriklivet n.d.)—a program under the Swedish Energy Authority to support decarbonization initiatives in heavy industry. While the initial funds were relatively small, they were important in funding early research. Universities and research institutes were invited to research several aspects of the steel transition, from technical to market effects (HYBRIT n.d.b).

The pace of development increased in 2020, when HYBRIT launched a pilot plant for testing H-DR (HYBRIT n.d.a). By the end of the year, LKAB announced plans to invest 400 billion Swedish Krona (SEK) (roughly $40 billion) over 20 years to transition from producing iron ore to DRI. This would enable zero emissions from all products and processes by 2045—slashing 40 to 50 million tonnes of annual CO2 emissions (LKAB n.d.b). In January 2022, SSAB declared that it would invest SEK 45 billion (roughly $4.5 billion) in decarbonizing its facilities (SSAB 2022).

With these plans, the companies’ power demand will increase to 20 Terawatt-hours (TWh) by 2030 and 70 TWh by 2050—about half of Sweden’s total production today and nearly the amount of electricity generated in the state of Missouri.

H2 Green Steel

The second green steel project in Sweden is the start-up H2 Green Steel (H2GS), launched in 2020 by venture capitalist Harald Mix and his investment firm Vargas Holding. Mix had been involved in the battery start-up Northvolt and it had become clear that steel would be the next step in the decarbonization of the vehicles industry. Green steel would enable carmakers to offer an even “greener” car to climate-conscious early adopters, and costs would only increase by a few hundred dollars that could be passed on to consumers.

H2GS was announced in early 2021. The plan is to build a facility that includes production of hydrogen, iron, and steel in the town of Boden in northern Sweden. Production is set to start in 2025, gradually increasing capacity to 5 mtpa by 2030—doubling Sweden’s current steelmaking capacity.

Mix and his team’s most significant challenge was creating a start-up reliant on large investments in unproven technology in the highly inert steel industry. Their strategy has been based on getting upstream and downstream actors to buy in on the success of the company. They recruited Henrik Henriksson, former CEO of the truck-making company Scania, to lead the new company. Then, H2GS worked the market to get offtake agreements with major steel purchasers. Scania was one of the first customers, together with machinery makers Miele and Electrolux. In 2022, H2GS announced that it had sold 1.5 out of the 2.5 million tonnes worth of initial annual output over 5 to 7 years—orders worth over 100 billion SEK ($9.5 billion) (Svensson 2022). In June 2023, Scania announced that it will buy an undisclosed amount of green steel from H2GS as part of its plan to use 100 percent green steel by 2030 (H2 Green Steel 2023a). Upstream firms such as Kobe Steel, the owner of Midrex, one of the two companies that manufacture H-DRI furnaces (H2 Green Steel 2022) and cable and grid technology manufacturer Hitachi Energy have both purchased equity in the company. These contracts and offtake agreements have been important to secure funding, as H2GS could show that there is demand for the product in negotiations with banks to lower capital costs. In October 2022—a year and a half after the company was announced—H2GS had secured €3.5 billion in debt financing, out of its goal of €5 billion (H2 Green Steel 2022).

Financing the Transition

The state has had a direct engagement in fostering the development of green steel in Sweden. As mentioned earlier, the Climate Policy Framework gave clear directionality for the Swedish iron and steel industry toward deep decarbonization, and the Fossil Free Sweden also formalized a framework for coordinating business initiatives for decarbonization with policymakers. Furthermore, the state—both at the national level and at the EU level—has played a key role in taking on risk and financing the transition through several channels, listed and discussed below.

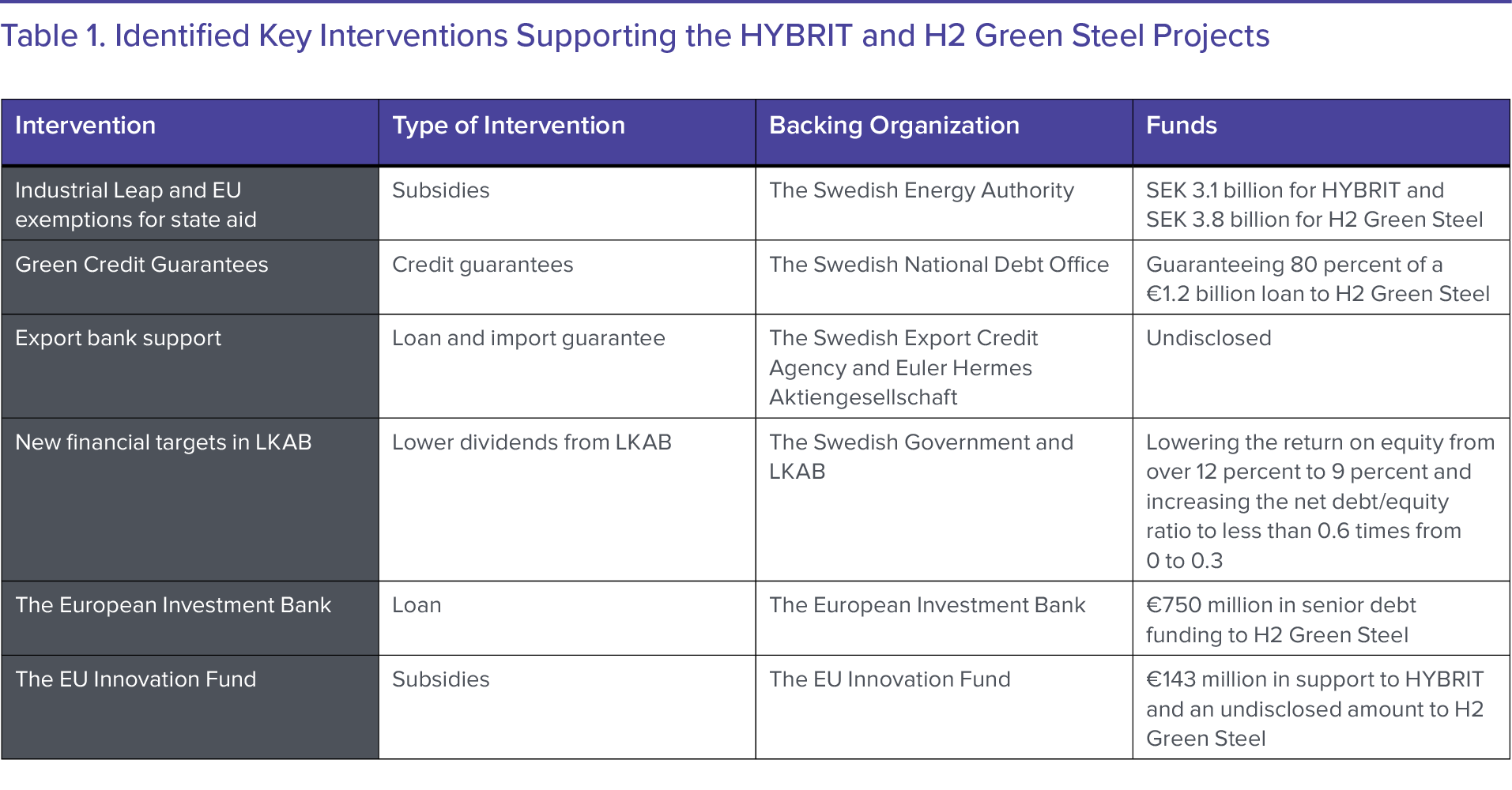

The Industrial Leap and EU Exemptions for State Aid

In 2016, the government set up The Industrial Leap, run by the Swedish Energy Authority, which supports investments in clean technologies and research on an application basis. As mentioned earlier, this program was important for initial research in the HYBRIT initiative but has also given SEK 30 million for initial technical work at the H2 Green Steel site.

The Industrial Leap has now been expanded and can give larger subsidies for major investments. It was the Swedish government’s contribution to the EU’s Recovery and Resilience Facility in 2021 (Energimyndigheten 2023a). HYBRIT and H2 Green Steel have applied for SEK 3.7 billion and SEK 3.8 billion, respectively, under the program (Björkland 2023), and the Energy Agency has approved SEK 3.1 billion for HYBRIT (Energimyndigheten 2023b). This form of state aid was previously banned in the EU, but this ban has been lifted on state aid that supports the EU’s goals of a clean economy (European Commission 2021).

Green Credit Guarantees

In 2021, the government gave the Swedish National Debt Office (SNDO) the mandate to issue “green credit guarantees” in SEK, euros, or dollars to guarantee up to 80 percent of the loan for an investment that contributes to lower emissions (Riksgälden n.d.). By guaranteeing a loan and thus taking over risk, the government can show commitment to a project and lower its capital costs. The SNDO has now approved a green credit guarantee for H2 Green Steel for a €1.2 billion loan (Riksgälden 2023).

Export Banks

In October 2022, H2 Green Steel announced that it had received debt financing of €3.5 billion in an agreement with the Swedish Export Credit Agency (SECA) and a number of private banks (H2 Green Steel 2022). In 2020, the government tasked the SECA with investigating how it can contribute to the global climate transition and help Sweden reach its targets under the Climate Policy Framework (EKN 2021). Energy sector exporters in Sweden can now apply for funding from the SECA (Svensk Exportkredit n.d.a), and the agency has established a Scientific Climate Council to support and advise its operations to align export finance with climate targets (EKN 2021). The SECA now has a target that 50 percent of issued loans should be green by 2030 (Svensk Exportkredit n.d.b).

New Financial Targets in LKAB

In October 2021, LKAB held an extraordinary general meeting with the state during which new financial targets were agreed upon (LKAB 2021). The government stated that “to support the strategy and increase flexibility in the upcoming transformation” (LKAB 2021), the government would increase the allowed net debt/equity ratio to <0.6, up from 0-0.3, and lower the targeted return on equity from 12 to 9 percent. Through its direct and full ownership, the state has been able to allow for higher debt and lowering the target return on equity, thus supporting LKAB to achieve its transition by lowering revenue to the state budget rather than by increasing expenditure via subsidies.

The European Investment Bank

The EU has also been an important direct player in the Swedish green steel transition. In 2019, the European Investment Bank (EIB) received an updated mandate to turn it into “the EU climate bank” in line with the Green Deal of 2019 (EIB 2020). This new mandate emphasizes low-carbon projects such as H2GS. The EIB came out as a financial intermediary for H2GS in 2021, and in 2022 it was announced that EIB had received board approval of €750 million in senior debt funding for H2GS (H2 Green Steel 2022).

The EU Innovation Fund

Under the EU’s Emission Trading Scheme (ETS), firms have to pay for emissions in the EU. Revenue from this scheme funds the EU Innovation Fund, which funds the deployment of green technologies. The Fund announced in April 2022 that it would support HYBRIT with €143 million (Vattenfall 2022) and in July 2023 H2GS announced that it had been chosen as one of 41 projects in the EU receiving €3.6 billion (European Commission 2023; H2 Green Steel 2023b).

Discussion: Directionality, Risk-Taking, Ownership, and Competition

Sweden is currently a leader in steel decarbonization. But why has steel decarbonization reached so far in Sweden, and not in other countries with similar endowments of renewable energy and iron ore? What lessons can be learned from Sweden for industrial decarbonization elsewhere?

In the interviews and document analysis conducted for this early study, four policy factors stood out: 1) clear directionality with broad political backing on where iron and steelmaking should be heading, 2) risk-taking by the state in the innovation process, 3) ability to influence the innovation system through its direct ownership, and 4) competition bringing speed and diversity to the transition.

Directionality

The scientific literature on innovation for industrial transitions points to directionality as a key pillar enabling transformations (Grillitsch et al. 2019; Mazzucato 2016; Nilsson et al. 2021). Innovation is inherently uncertain and bears significant risks, especially when associated with heavy industries using large production units that are heavily reliant on infrastructure and that invest over very long time horizons. To manage such risks, the state should not pick a “winning” technology but rather set a “direction of change” and allow experimentation and learning from industry and other stakeholders (Mazzucato 2016). This process allows the different parts of the innovation system to coalesce around a path to decarbonization and collaborate across the value chain in its development.

The Swedish Climate Policy Framework created this directionality and long-term policy stability, and the creation of Fossil Free Sweden established an institution through which learning and cooperation across private firms, the state, and other stakeholders could be developed. The wider development in the EU with the EU ETS and phase-out of free emissions credits have further enhanced this directionality.

Risk-Taking

Second, rather than merely “fixing” the market by putting a price on externalities, i.e., pricing carbon, the state has been pushing innovation by actively taking on and sharing risk along with private firms (Lazonick and Mazzucato 2013; Mazzucato 2013). Such risk-taking based on a path toward decarbonization can enable innovation, create new markets, and thus help break out of fossil dependency.

There is an ongoing debate on the recent turn to industrial policy and what has been dubbed as the “de-risking state”—when the state takes on risk to enable private investment. UK-based Professor of Economics and Macro-Finance Daniela Gabor, who has been a prominent participant in the debate, argues that a clear limit with this approach is that it “outsources the pace of decarbonisation to private capital, and in so doing, can amplify its disorderly expansion guided by shifting profit opportunities” (Gabor 2023). Indeed, in the Swedish case, the target of net zero by 2045 is set for the government, and apart from carbon pricing under the EU ETS, there are no extra penalties for firms that do not reduce their emissions to zero by 2045. However, de-risking has been important in the Swedish case specifically in increasing the pace of the transition by lowering capital costs for technologies that have been untested at scale, for example electrolysers for H2 Green Steel imported from Germany (Martin 2023), and for accessing finance of the size required. HYBRIT did not plan to apply for the relatively larger subsidies under The Industrial Leap in the original timeline of decarbonization by 2045, as technology risk was manageable in this slower pace. In the shorter timeline, subsidies became a key enabler.

A more important limitation with the de-risking approach in the Swedish case is the lack of conditionalities that distribute both risks and rewards (Lazonick and Mazzucato 2013). De-risking has been important in lowering capital costs for H2GS and helping attract investors, but there are no conditionalities on the distribution of rewards. While the start-up is building a new plant, and therefore by definition should create jobs and provide tax revenue, there is no guarantee of long-term success. There are ample opportunities for personal profiting even though the project struggles (see, for example, the battery manufacturer Freyr in bordering Norway, which received unconditioned support from the EU Innovation Fund as late as July 2023 after which the CEO took out the equivalent of $11 million in dividends and is now moving operations to the US). Support for H2GS and other industries could be combined with curbs on personal remuneration until the plant is operating commercially.

State Ownership

In addition to directionality and risk-taking, the Swedish state’s ownership in key firms enabled a deeper push for iron and steel decarbonization. Sweden has for the last few decades been governed in a market-oriented fashion, with privatization of welfare services and companies. However, LKAB and Vattenfall are exceptions to this trend and have remained state-owned. While the Swedish government cannot command its state-owned enterprises (SOEs), it can appoint board members in the companies and set general targets for SOEs through its ownership policy.

Due to state ownership of LKAB and Vattenfall, these companies can incorporate the long-term social (and not commercial) goal of decarbonization in their strategies, without having to please shareholders whose main concern is to maximize short-term financial returns (Lazonick 2015). While it is commonly argued that SOEs are less efficient than private firms, they can play a particular role as instruments of innovation policy in an innovation system by “combining risk-taking and long-term orientation” and acting as “coordinating or direction giving change agents” (Tõnurist and Karo 2016). The long-term orientation and risk-taking is indicated by LKAB’s new financial targets. The ownership structure also allowed the firms to coordinate the value chain and cooperate in negotiations with government, which is unusual.

State ownership has been shown to distort the steel market, and the OECD has found it to be related to subsidies and overcapacity (OECD 2018). At the same time, state ownership can play a particular role in innovation and decarbonization. The OECD has also found that “due to the use of SOEs by the state to further a ‘green’ agenda and use the SOE as an instrument to directly increase deployment of zero or low carbon electricity generation . . . SOE ownership has a positive effect on investment in the renewable electricity generation sector in OECD and G20 countries” (Prag et al. 2018). This is in line with other empirical studies (see, for example, Mazzucato and Semieniuk 2018). While SOEs may have market-distorting effects, they can be useful tools for innovation and decarbonization. Encouraging SOEs to take on an innovative role in the decarbonization process while avoiding damaging market distortions will be a difficult but important balancing act.

Direct and indirect state ownership has also disciplined LKAB, SSAB, and Vattenfall to follow the goal of decarbonization rather than pushing back to maximize shareholder value (Lazonick 2015; Palladino and Estevez 2022). This discipline complements the de-risking approach discussed above, avoiding the pitfalls described in Gabor 2023.

Competition

Finally, having two different types of projects that can both complement and compete with one another has sped up and diversified the decarbonization of the Swedish iron and steel industry.

First, HYBRIT’s pilot plant was an important enabler of H2GS. H2GS is a start-up, and spending years first on researching the technology and then piloting would not have been possible for a company without revenue. With HYBRIT having done much of the initial work showing that the H-DR-EAF steelmaking route was not only technically possible but could also be financially viable, it became possible for H2GS to credibly make the case for steelmaking using similar technology.

Second, H2GS has to get a revenue stream up and running as quickly as possible, and has therefore set itself a very tight deadline. While HYBRIT took on an early role in bridging green innovation from the step of early technology development to demonstration and deployment, H2GS put speed at the heart of the process. As H2GS needs to minimize the time during which it is spending venture capital before generating revenue, its incentives are aligned with the need for rapid action on climate. H2GS was announced in 2021, and this competition pushed HYBRIT to move forward its plans, sparing the atmosphere millions of tonnes of CO2. H2GS therefore responds to what Lazonick and Mazzucato 2013) call the “opportunity creation” of the Swedish entrepreneurial state, and reciprocates by speeding up the entire process.

At the same time, HYBRIT and H2GS have somewhat different profiles and customer segments. HYBRIT includes a transition of SSAB, building on established value chains and customer bases, but also ironmaking. This can enable transitions both in Sweden and abroad, as other steelmakers can replace their integrated BF-BOF mills with EAFs fed with DRI from LKAB. H2GS, on the other hand, is meeting a certain segment of early adopters across industries. This helps diffuse hydrogen-based steelmaking but will not be a strategy that’s possible for all steelmakers when all steel should be green steel.

Conclusion

The Swedish iron and steel transition is at the forefront of the global steel decarbonization process, and the state has played a key role via long-term directionality, risk-taking, and state ownership. While increasing carbon prices and the phase-out of free emissions credits under the EU Emission Trading Scheme (EU ETS) has of course played an important role in shaping the market, the Swedish approach has neither been simple carbon pricing nor passive subsidies for industry initiatives. Instead, use of industrial policy has been active and multifaceted, spanning from broad direction-setting to direct involvement in the innovation system.

We are still in the early phase of the decarbonization process and don’t know whether the projects will deliver on time or be profitable in the long term. How to meet expected power demand is also becoming a contentious issue; several officials in the new government have expressed the opinion that the projects should be paused until new nuclear plants are built, though officially the government continues to back the green steel plans. Furthermore, the distribution of risks and rewards via effects on labor markets, taxes, and profits are yet to be seen.

At this point, however, we can conclude that the relevant companies have committed to clear timelines and strategies, received financing for their plans, and have shown the potential of a green technology that is now a key component of the global steel industry’s path to decarbonization, highlighted as notable progress for the steel industry by the International Energy Agency (IEA n.d.).

So, what can we learn from the Swedish case for decarbonization of US industry?

The steel industries of the United States and Sweden differ significantly. The US steel industry is much larger and has more firms, a high share of scrap-based steelmaking, and no state ownership. The US political landscape is more polarized, further diminishing the prospect of long-term policy stability. The US power mix is also more carbon intensive than Sweden’s, and a simple transition from coal to hydrogen steelmaking would only provide emission reductions of 19 percent, relative to Sweden’s 95 percent (Blank 2019). In addition, the US also has a coal industry that is likely to resist a transition.

A second Biden administration will have to ensure policy stickiness (see, for example, Meckling et al. 2015) to make it difficult for later administrations to simply dismantle decarbonization policies. As Sweden’s example shows, a key step to push primary and secondary steelmakers to decarbonize will be to enable value chain cooperation and to transform declining renewable energy costs into attractive paths to decarbonization. Lacking the advantage of a clean power mix, the US needs to both replace fossil energy in the power sector and expand the total power generated to electrify industrial processes. Though the Inflation Reduction Act provides a generous subsidy for green hydrogen, significantly improving the cost competitiveness of clean industrial processes (Department of Energy n.d.), the federal government could leverage its federally owned Power Marketing Administrations and Army Corps of Engineers to produce and deliver low-cost clean energy for steelmakers.

Regulations and economics will always limit the strategic options available for both investor- and state-owned entities. Notably, Vattenfall paused an offshore wind project in the UK citing higher costs without being able to raise revenue from power generation. But state-owned entities can play a key role in strategically pursuing decarbonization objectives independently of short-term shareholder value maximization. At the federal level, the five federally owned electric utilities and/or the Army Corps of Engineers could be authorized to build and operate clean energy generation in collaboration with energy-intensive industries, supported with a pause in US Treasury payments. They can also be mandated to prioritize low-cost energy to innovative industrial decarbonization projects. By doing so, they could support innovation, increase competition with investor-owned utilities, and develop crucial government capacity within clean energy and hydrogen management.

Furthermore, the US primary steel industry is dominated by US Steel and Cleveland-Cliffs. Japanese steelmaker Nippon Steel has made an offer to buy US Steel (de la Merced and Swanson 2023) though its bid will be reviewed by the White House and it is unclear whether Nippon Steel is sufficiently ambitious on decarbonization. Cleveland-Cliffs has been mentioned as a potential alternative buyer of US Steel (Bushey et al. 2023). Cleveland-Cliffs recently announced that it will reline a blast furnace, extending the lifetime of the furnace by another several decades and indicating that it does not believe it will need to decarbonize soon (Pete 2023). A Cleveland-Cliffs monopoly in the primary steel sector would yield shareholders in Cleveland-Cliffs outsized power to set the pace of US primary steel decarbonization, and the White House should carefully consider how any potential buyer of US Steel may affect how competition aligns with decarbonization in the sector.

The United States has started its journey toward a clean energy future. But to increase the pace of the transition, ensure policy stickiness, and minimize potential pushback, the next administration could learn from Sweden and complement the current de-risking-oriented approach established with the Inflation Reduction Act. Enabling value chain cooperation and ensuring competition from firms with different ownership and ownership types could be key steps moving the fight for a healthy planet forward.

____

This essay is based on interviews with Mårten Görnerup, former CEO of HYBRIT; Ola Hansén, director of Public Affairs at H2 Green Steel; and Per Bolund, former Minister for Financial Markets, and Minister for Climate, who I thank for their invaluable input. I also want to thank Joachim Peter Tilsted, Max Åhman, Max Jerneck, Chris DellaCamera, and Elisabeth Lindberg for commenting on an earlier draft of this essay, as well as Roosevelt Institute staff Suzanne Kahn and Todd N. Tucker for comments and Sonya Gurwitt and Claire Greilich for their editorial contributions.

References

Read the references

Björkland, S. 2023. “Svensk Stål-vd Vill Ha Miljardstöd: ‘Behövs Smörjmedel’”. Dagens Nyheter, March 7, 2023. https://www.dn.se/ekonomi/svensk-stal-vd-vill-ha-miljardstod-behovs-smorjmedel/.

Blank, Thomas Koch. 2019. “The Disruptive Potential of Green Steel.” Rocky Mountain Institute, September 2019. https://rmi.org/wp-content/uploads/2019/09/green-steel-insight-brief.pdf.

Bushey, Claire, Oetenca Aliaj, and Sujeet Indap. 2023. “Bid for US Steel Promises National Security through Consolidation.” Financial Times, August 18, 2023. https://www.ft.com/content/19ef2f73-8898-4999-a1f9-8c761f5ecaba.

Delasalle, Faustine, Eveline Speelman, Alasdair Graham, Rafal Malinowski, Hannah Maral, Andrew Isabirye, Marc Farre Moutinho, Laura Hutchinson, Chathurika Gamag, and Lachlan Wright. 2022. Making Net-Zero Steel Possible. Washington, DC: Mission Possible Partnership. https://missionpossiblepartnership.org/wp-content/uploads/2022/09/Making-Net-Zero-Steel-possible.pdf.

EKN. 2021. “EKN and SEK establish a Scientific Climate Council.” Press release, August 26, 2021. https://www.ekn.se/en/about-ekn/newsroom/archive/2021/press-releases/ekn-and-sek-establish-a-scientific-climate-council/.

Energimyndigheten. 2023a. “Industriklivet.” Accessed January 16, 2024. https://www.energimyndigheten.se/forskning-och-innovation/forskning/industri/industriklivet/.

Energimyndigheten. 2023b. “3.1 miljarder i stöd till Hybrit.” Press release, December 14, 2023.

https://www.energimyndigheten.se/nyhetsarkiv/2023/31-miljarder-i-stod-till-hybrit/.

European Commission. 2021. “State Aid: Commission Endorses the New Guidelines on State Aid for Climate, Environmental Protection and Energy.” Press release, December 21, 2021. https://ec.europa.eu/commission/presscorner/detail/en/ip_21_6982.

European Commission. 2023. “Innovation Fund: EU Invests €3.6 Billion of Emissions Trading Revenues in Innovative Clean Tech Projects.” Press release, July 13, 2023. https://ec.europa.eu/commission/presscorner/detail/en/ip_23_3787.

European Investment Bank. 2020. EIB Group Climate Bank Roadmap 2021-2025.

https://www.eib.org/en/publications/the-eib-group-climate-bank-roadmap.htm.

Department of Energy. n.d. “Financial Incentives for Hydrogen and Fuel Cell Projects.” Office of Energy Efficiency & Renewable Energy, Hydrogen and Fuel Cell Technologies Office. https://www.energy.gov/eere/fuelcells/financial-incentives-hydrogen-and-fuel-cell-projects.

Gabor, Daniela. 2023. “The (European) Derisking State.” Stato e mercato, Rivista quadrimestrale.

https://www.rivisteweb.it/doi/10.1425/107674.

Grillitsch, Markus, Teis Hansen, Lars Coenen, Johan Miörner, and Jerker Moodysson. 2019. “Innovation Policy for System-Wide Transformation: The Case of Strategic Innovation Programmes (SIPs) in Sweden.” Research Policy 48, no. 4 (May): 1048-61. https://doi.org/10.1016/j.respol.2018.10.004.

H2 Green Steel. 2022. “Leading European Financial Institutions Support H2 Green Steel’s €3.5 Billion Debt Financing.” Press release, October 24, 2022. https://www.h2greensteel.com/latestnews/leading-european-financial-institutions-support-h2-green-steels-35-billion-debt-financing.

H2 Green Steel. 2023a. “Scania Places First Green Steel Order in Further Step Towards Decarbonized Supply Chain.” Press release, June 27, 2023.

https://www.h2greensteel.com/latestnews/scania-places-first-green-steel-order-in-further-step-towards-decarbonized-supply-chainnbsp

H2 Green Steel. 2023b. “Great news! H2 Green Steel has been selected as one of the strategic green tech initiatives…” LinkedIn post, July 13, 2023. https://www.linkedin.com/posts/h2greensteel_the-innovation-fund-activity-7085574611181944832-BONd/?trk=public_profile_like_view.

HYBRIT. n.d.a. “Pilot Scale Direct Reduction with Hydrogen.” Accessed January 13, 2024. https://www.hybritdevelopment.se/en/a-fossil-free-development/direct-reduction-hydrogen-pilotscale/.

HYBRIT. n.d.b. “Collaborative Research.” Accessed January 16, 2024. https://www.hybritdevelopment.se/en/research-project/collaborative-research/.

Intergovernmental Panel on Climate Change (IPCC). 2022a. Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge, UK: Cambridge University Press. https://doi.org/10.1017/9781009157926.013.

______ 2022b. “Summary for Policymakers.” In Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge, UK: Cambridge University Press. https://doi.org/10.1017/9781009157926.001.

International Energy Agency (IEA). 2019. Iron and Steel Technology Roadmap. Paris: IEA.

https://iea.blob.core.windows.net/assets/eb0c8ec1-3665-4959-97d0-187ceca189a8/Iron_and_Steel_Technology_Roadmap.pdf.

______ 2022. Achieving Net Zero Heavy Industry Sectors in G7 Members. Paris: IEA. https://iea.blob.core.windows.net/assets/c4d96342-f626-4aea-8dac-df1d1e567135/AchievingNetZeroHeavyIndustrySectorsinG7Members.pdf.

International Energy Agency (IEA). n.d. “Steel.” Accessed January 13, 2024. https://www.iea.org/energy-system/industry/steel.

Industriklivet. n.d. “Industriklivet.” Retrieved October 13, 2023. https://www.industriklivet.se/.

Juhász, Réka, Nathan Lane, and Dani Rodrik. 2023. “The New Economics of Industrial Policy.” Working Paper no. 31538. NBER Working Paper Series. Cambridge, MA: National Bureau of Economic Research. https://www.nber.org/papers/w31538.

Klimatpolitiska Radet. n.d. “The Climate Policy Framework.” Retrieved October 13, 2023. https://www.klimatpolitiskaradet.se/en/the-climate-policy-framework/.

Lazonick, William. 2015. “Innovative Enterprise and Shareholder Value.” Law and Financial Markets Review 8, no. 1 (May): 52-64. https://doi.org/10.5235/17521440.8.1.52.

Lazonick, William, and Mariana Mazzucato. 2013. “The Risk-Reward Nexus in the Innovation-Inequality Relationship.” Industrial and Corporate Change 22, no. 4 (August): 1093-1128. https://doi.org/10.1093/icc/dtt019.

Lejestrand, Anna. 2023. “Vem äger elproduktionen? – Energiföretagen Sverige” Energiföretagen. February 20, 2023. https://www.energiforetagen.se/energifakta/elsystemet/produktion/vem-ager-elproduktionen/.

LKAB. 2021. “Extraordinary General Meeting of LKAB – Decision on New Financial Targets.” Press release, October 27, 2021. https://lkab.com/en/press/extraordinary-general-meeting-of-lkab-decision-on-new-financial-targets/.

LKAB. n.d.a. “Webbinarium om LKAB:s koldioxidfria framtid.” Retrieved October 13, 2023. https://lkab.com/press/webbinarium-om-lkabs-koldioxidfria-framtid/.

LKAB. n.d.b. “LKAB and the Climate.” Retrieved October 13, 2023. https://lkab.com/en/what-we-do/our-transformation/lkab-and-the-climate/.

Mark- och miljödomstolen. 2019. “Mark-och miljödomstolen DELDOM.” Retrieved October 13, 2023. https://www.naturvardsverket.se/4a43c8/contentassets/45c088b2988549d6b2506cd05c0b7b2c/2019-10-18-mmd-nacka.pdf.

Martin, Polly. 2023. “World’s First Commercial-Scale Green Steel Plant on Track for FID after Ordering 700MW of Hydrogen Electrolysers.” Hydrogen Insight, May 22, 2023. https://www.hydrogeninsight.com/industrial/worlds-first-commercial-scale-green-steel-plant-on-track-for-fid-after-ordering-700mw-of-hydrogen-electrolysers/2-1-1454069.

Material Economics. 2019. Industrial Transformation 2050 – Pathways to Net-Zero Emissions from EU Heavy Industry. Stockholm, Sweden: Material Economics. https://materialeconomics.com/material-economics-industrial-transformation-2050.pdf?cms_fileid=303ee49891120acc9ea3d13bbd498d13.

Mazzucato, Mariana. 2013. The Entrepreneurial State: Debunking Public vs. Private Sector Myths. London: Anthem Press.

______ 2016. “From Market Fixing to Market-Creating: A New Framework for Innovation Policy.” Industry and Innovation 23, no. 2 (May): 140-156. https://doi.org/10.1080/13662716.2016.1146124.

Mazzucato, Mariana, and Gregor Semieniuk. 2018. “Financing Renewable Energy: Who Is Financing What and Why It Matters.” Technological Forecasting and Social Change 127 (February): 8-22. https://doi.org/10.1016/j.techfore.2017.05.021.

Meckling, Jonas, Nina Kelsey, Eric Biber, and John Zysman. 2015. “Winning Coalitions for Climate Policy.” Science 349, no. 6253 (September): 1170-1171. https://doi.org/doi:10.1126/science.aab1336.

de la Merced, Michael J., and Ana Swanson. 2023. “U.S. Steel to Be Bought by Japanese Rival After Takeover Drama.” New York Times, December 18, 2023. https://www.nytimes.com/2023/12/18/business/us-steel-nippon-steel-deal.html.

Nilsson, Lars J., Fredric Bauer, Max Åhman, Fredrik N. G. Andersson, Chris Bataille, Stephane de la Rue du Can, Karin Ericsson, Teis Hansen, Bengt Johansson, Stefan Lechtenböhmer, Mariësse van Sluisveld, and Valentin Vogl. 2021. “An Industrial Policy Framework for Transforming Energy and Emissions Intensive Industries Towards Zero Emissions.” Climate Policy 21, no. 8 (July): 1053-1065. https://doi.org/10.1080/14693062.2021.1957665.

Organisation for Economic Cooperation and Development (OECD). 2018. “State Enterprises in the Steel Sector.” Working Paper no. 53. OECD Science, Technology and Industry Policy Working Papers Series. Paris: OECD. https://www.oecd-ilibrary.org/docserver/2a8ad9cd-en.pdf?expires=1703943511&id=id&accname=guest&checksum=25051AD2F0570A63E369BA53D4D70973.

Palladino, Lenore, and Isabel Estevez. 2022. “The Need for Corporate Guardrails in US Industrial Policy.” Roosevelt Institute, August 18, 2022. https://rooseveltinstitute.org/publications/the-need-for-corporate-guardrails-in-us-industrial-policy/.

Pete, Joseph S. 2023. “Cleveland-Cliffs to Reline Blast Furnace in 2025.” Times of Northwest Indiana, May 31, 2023. https://www.nwitimes.com/news/local/business/cleveland-cliffs-to-reline-blast-furnace-in-2025/article_25131a98-ffdf-11ed-8393-7f5bd7ca2248.html.

Prag, Andrew, Dirk Röttgers, and Ivo Scherrer. 2018. “State-Owned Enterprises and the Low-Carbon Transition.” Working Paper no. 129. OECD Environment Working Papers Series. Paris: OECD. https://www.oecd-ilibrary.org/docserver/06ff826b-en.pdf?expires=1703943114&id=id&accname=guest&checksum=D6E55E28829C9707318E254CE877628C.

Rootzén, Johan, and Filip Johnsson. 2016. “Paying the Full Price of Steel – Perspectives on the Cost of Reducing Carbon Dioxide Emissions from the Steel Industry.” Energy Policy 98 (November): 459-469. https://www.sciencedirect.com/science/article/abs/pii/S0301421516304876.

Regeringen. 2016. “Initiativet Fossilfritt Sverige.” Press release, July 8, 2016. https://www.regeringen.se/rattsliga-dokument/kommittedirektiv/2016/07/dir.-201666/.

Riksgälden. n.d. “Credit Guarantees for Green Investments.” Last reviewed December 21, 2023. https://www.riksgalden.se/en/our-operations/guarantee-and-lending/credit-guarantees-for-green-investments/.

Riksgälden. 2023. “Green Credit Guarantee for a Loan to H2 Green Steel.” Press release, December 22, 2023. https://www.riksgalden.se/en/press-and-publications/press-releases-and-news/news/2023/green-credit-guarantee-for-a-loan-to-h2-green-steel/.

SSAB. 2022. “SSAB planerar för nytt produktionssystem i Norden och tidigarelägger den gröna omställningen.” Press release, January 28, 2022. https://www.ssab.com/sv-se/nyheter/2022/01/ssab-planerar-fr-nytt-produktionssystem-i-norden-och-tidigarelgger-den-grna-omstllningen.

Svensk Exportkredit. n.d.a. “Sustainability.” Retrieved October 13, 2023. https://www.sek.se/en/sustainability/.

Svensk Exportkredit. n.d.b. “Energy. ” Retrieved October 13, 2023. https://www.sek.se/en/promotion/sweden-the-worlds-first-fossil-free-wellfare-country/.

Svensson, Mikael. 2022. “H2 Green Steel har redan order på 100 miljarder kronor.” Bergsmannen, May 11, 2022.

https://www.bergsmannen.se/nyheter/e/5556/h2-green-steel-har-redan-order-pa-100-miljarder-kronor/.

Tõnurist, Piret, and Erkki Karo. 2016. “State Owned Enterprises as Instruments of Innovation Policy.” Annals of Public and Cooperative Economics 87, no. 4 (February): 623–648. https://onlinelibrary.wiley.com/doi/abs/10.1111/apce.12126.

Vattenfall. 2016. “Vattenfalls års- och hållbarhetsredovisning.” Retrieved October 13, 2023. https://group.vattenfall.com/se/siteassets/sverige/om-oss/finans/arsrapporter/2016/vattenfall_arsredovisning_2016.pdf.

Vattenfall. 2022. “HYBRIT Receives Support from the EU Innovation Fund.” Press release, April 1, 2022. https://group.vattenfall.com/press-and-media/pressreleases/2022/hybrit-receives-support-from-the-eu-innovation-fund.

Vogl, Valentin, Olle Olsson, and Björn Nykvist. 2021. “Phasing Out the Blast Furnace to Meet Global Climate Targets.” Joule 5, no. 10 (October): 2646-2662. https://www.sciencedirect.com/science/article/pii/S2542435121004359.

Vogl, Valentin, and Max Åhman. 2019. What Is Green Steel? Towards a Strategic Decision Tool for Decarbonising EU. Lund, Sweden: Lund University. https://lucris.lub.lu.se/ws/files/66962032/What_is_green_steel_P532.pdf.

Vogl, Valentin, Max Åhman, and Lars J. Nilsson. 2018. “Assessment of Hydrogen Direct Reduction for Fossil-Free Steelmaking.” Journal of Cleaner Production 203 (December): 736-745. https://doi.org/10.1016/j.jclepro.2018.08.279.

Wesseling, Joeri, Stefan Lechtenböhmer, Max Åhman, L.J. Nilsson, Ernst Worrell, and Lars Coenen. 2017. “The Transition of Energy Intensive Processing Industries Towards Deep Decarbonization: Characteristics and Implications for Future Research.” Renewable and Sustainable Energy Reviews 79 (November): 1303-1313. https://doi.org/10.1016/j.rser.2017.05.156.

Explore the Series

The Role of State Ownership: Overview of State-Owned Entities in the Global Economy

by Kyunghoon Kim

Finance as a Tool of Industrial Policy: A Taxonomy of Institutional Options

by Saule T. Omarova

Just Energy Transition in the Time of Place-Based Industrial Policy: Patch or Pathway to the Green Industrial Transformation?

by Andrea Furnaro

Fair Transition Funds, Employer Neutrality, and Card Checks: How Industrial Policy Could Relaunch Labor Unions in the United States

by César F. Rosado Marzán

Electric Vehicles: How Corporate Guardrails Can Improve Industrial Policy Outcomes

by Lenore Palladino

About the Author

Jonas Algers

Guest AuthorJonas Algers is a PhD candidate at the division for environmental and energy systems studies at Lund University where he studies the political economy of steel industry decarbonization.