July’s Jobs Report: Strong Numbers across the Economy, but a Full Recovery Will Take Continued Support

August 6, 2021

By Mike Konczal, Aaron Sojourner

Beating the forecasts with 943,000 new jobs, and positive developments on multiple fronts, today’s jobs report was excellent— evidence that spending by policymakers, with the goal of a faster recovery, is paying off in a strong labor market. In particular, today’s jobs report shows strong developments in employment and labor force participation rates, and in broad-based job growth across industries. However, there is work to be done, as unemployment rates for Black and Latinx workers—particularly women—remain unacceptably high.

Positive Developments on Jobs, Participation, Unemployment, and Industries

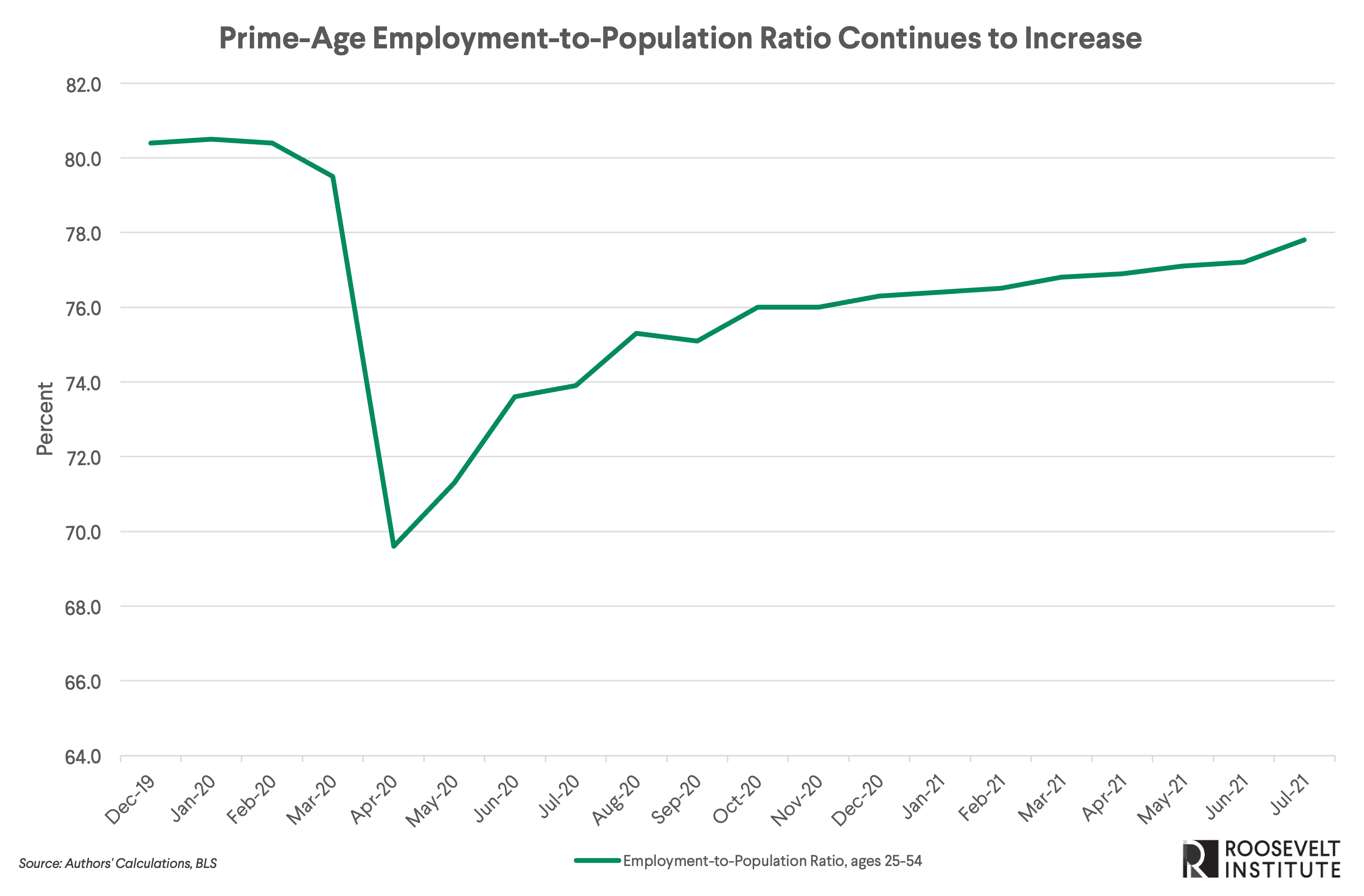

Today’s jobs numbers show positive developments when it comes to employment and labor force participation rates. The headline labor force participation rate stayed roughly the same at 61.7 percent—still 1.6 percentage points lower than in February 2020. However, the employment-to-population ratio increased 0.4 percentage points to 58.4 percent and is up a full percentage point since December 2020. This is a promising acceleration. In particular, the share of adults in their prime working years (ages 25 to 54) who are employed rose very quickly, from 77.2 percent to 77.8 percent. This measure omits people on the margins of retirement or school, and reflects core strengthening in the labor market.

Another positive development: The headline unemployment rate dropped from 5.9 to 5.4. During the recovery from the Great Recession, it took until 2015 to get to this unemployment level. But this isn’t just the “disguised unemployment” many worry about, where unemployment is falling just because people have stopped looking for work and left the labor force—a dynamic that was a major challenge for the recovery during the early 2010s. Instead, the increase in the employment-to-population ratio means that unemployment is decreasing for the right reasons, in that people are finding jobs rather than quitting the labor force. Focusing on the employment-to-population ratio at this moment makes sense, as the pandemic and lockdowns have likely complicated traditional measurements of who is or is not considered unemployed and inside the labor market at any time. Even before the pandemic, there was increasing evidence that the distinction between being inside and outside the statistical definition of the labor force had less meaning. So focusing on the employment-to-population ratio gives a better sense of how truly strong the labor market is and how robust the recovery will be.

We also see a positive development in today’s job numbers in broad-based job growth across industries. There’s a noteworthy increase in jobs in leisure and hospitality services, with 380,000 jobs added—above the 347,000 jobs added on average each month for the previous three months. Restaurants can hire workers, despite what you read in the papers. It’s just that they’re all hiring at the same time so it’s not as easy as in the past. It’s still too early to tell what impact the elimination of unemployment insurance in many states and the rise of the Delta variant will have on the recovery, but the leisure and hospitality industry would be the first to feel its impact, and so far it’s holding steady.

A Long Road Ahead to Full Recovery

Even with these excellent numbers, there’s still a long way to go. Millions of American jobs are still missing compared to the pre-pandemic level or trend. Black unemployment remains at 8.2 percent, above it’s pre-pandemic low of 5.2 percent, which was still too high. Employment rates for Black and Latinx women remain the furthest below February 2020 levels. Employment-to-population ratios also remain below their pre-pandemic levels across all levels of education for those above the age of 25.

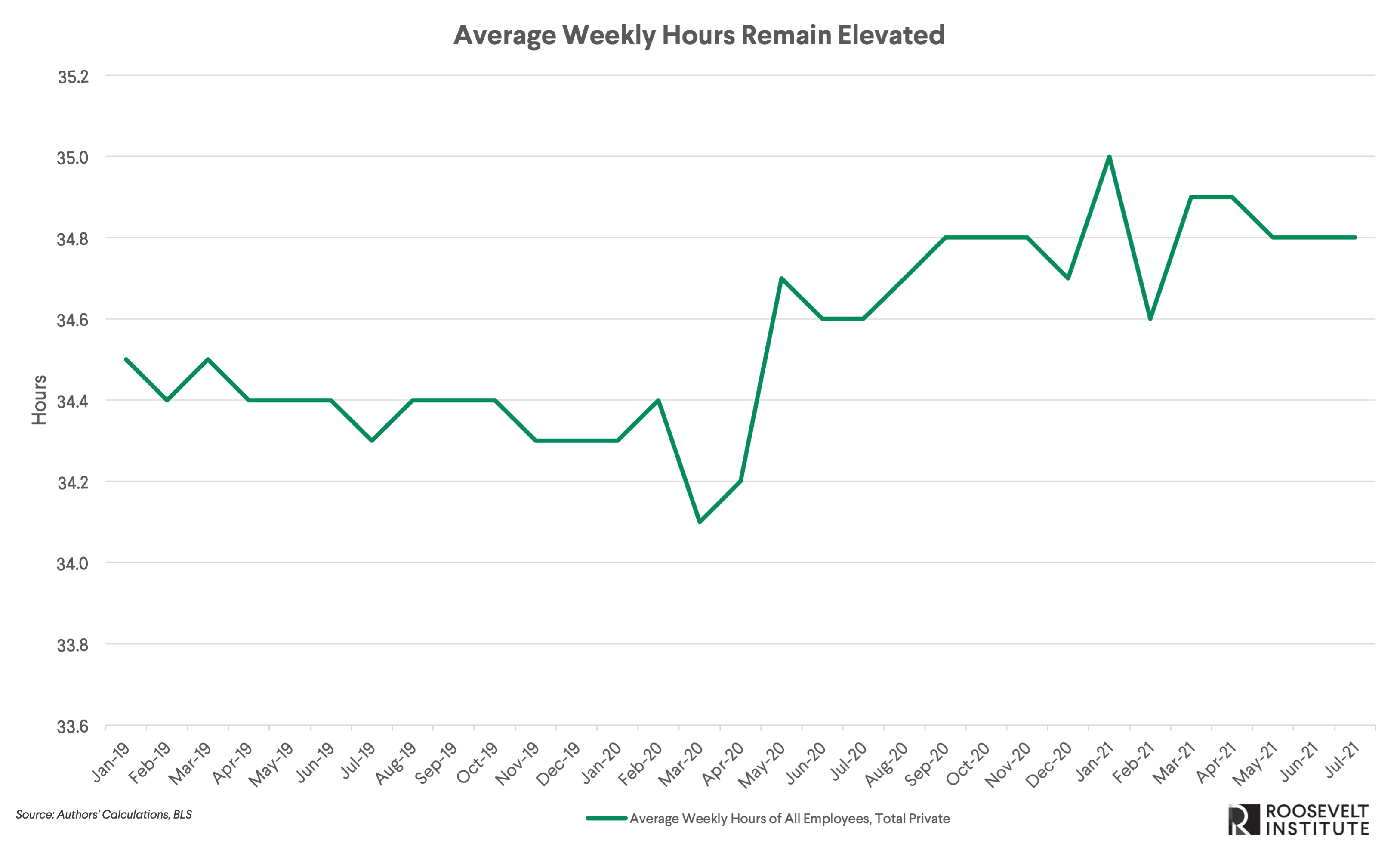

Another not as positive development is that average workweek hours remain elevated, suggesting that employers are choosing to have employees work longer hours rather than raising wages to hire faster. Since the data series reporting average workweek hours began in 2006, average workweek hours in the private sector never exceeded 34.6 hours until 2020. But now, hours have met or exceeded that level for a year straight. This increase to hours would translate to 1.4 million new jobs at pre-pandemic average hours.

There is a possibility that, rather than raise wage offers to new hires and prompt pressure from incumbents for raises to preserve pay equity, many employers are hoping to limp through the summer, minimize raises, and get the work done by fewer staff working more hours. Their hope may be that labor supply increases as schools reopen and enhanced unemployment insurance (UI) benefits expire. But so far, most of the early evidence has shown that cutting enhanced UI benefits has not had much effect on employment. Getting rid of enhanced UI benefits may increase labor supply, but it also decreases labor demand by pulling dollars out of the local economy. The effect on employment is therefore theoretically ambiguous, despite the unambiguous prediction that cutting enhanced UI will lower wages.

Finally, even at the current rate of increase, it will take until the end of 2022 to get to the pre-pandemic unemployment rate and employment trend. This is significantly better than what could have been, according to the CBO’s projections that it would have taken several additional years to achieve this speed of recovery without the American Rescue Plan. Yet policymakers should continue the supportive policies that are generating these numbers. The Federal Reserve should remain dovish in its approach, even as the economy adjusts to transitory inflation from supply-chain constraints. Congress should continue to support this recovery with necessary investments in infrastructure, care work, and climate mitigation. There’s well-deserved celebration about the level of spending that was achieved to keep nominal incomes steady throughout the pandemic. But as the Hutchins Center finds, fiscal policy is decelerating and moving from expansionary to contractionary in this quarter. This could have consequences next year, where the unemployment level the economy reaches will have major consequences for working people.

But good news is good news, and there’s a lot to celebrate. Today’s report builds off last month’s great jobs number (which turned out to be even better than first reported, as it was revised up 88,000 to now be 938,000), and shows that the fiscal and monetary support this year, most notably in the American Rescue Plan and the Federal Reserve’s commitment to keeping rates low, is working to speed up the recovery and get us to full employment faster. If we continue on this trajectory, we’ll have a recovery that will change the very way we think about how we respond to recessions.

Roosevelt Author

Mike Konczal

Former Director, Macroeconomic AnalysisAs former director of Roosevelt’s macroeconomic analysis team, Mike Konczal led research focused on achieving full employment, building an economy that truly works for everybody, and developing the next generation of economic ideas.