Comparing Oranges to Onions: What Is Crypto “Market Structure,” and Why Is It Important?

September 24, 2025

By Brad Lipton

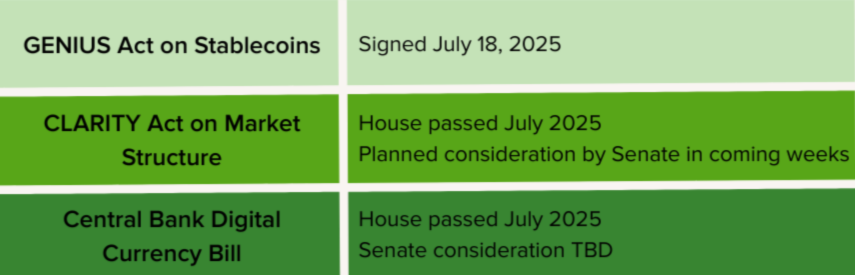

Congress is currently considering the second bill of its planned three-part trilogy on cryptocurrency. The first was the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, which President Donald Trump signed in July. In the coming weeks, the Senate expects to consider a so-called “market structure” bill, a similar version of which already passed the House. Both bills would create an entirely new framework for how cryptocurrency is regulated by the federal government. The Senate will likely also eventually consider the House-passed bill on “central bank digital currencies.”

Why is Congress contemplating this legislation, which some contend, without much exaggeration, could rip an enormous hole in our financial system and create the conditions that originally led to the Great Depression? If you could use a plain-language guide, we’ve got you.

This and my next blog post on the specifics of the pending market structure bills build on previous work from Roosevelt explaining the progressive case for crypto regulation.

What Is “Market Structure”?: Securities and Commodities

In this context, the phrase “market structure” just refers to how companies are classified for regulation, based on the assets they offer to investors. As you probably know, in the United States, different laws and rules enforced by different regulators apply to different types of companies, depending on what type of activity they engage in.

Cryptocurrency is a digital currency that can—at least theoretically—be used for a variety of purposes, including as an alternative payment system or speculative investment. This means that there isn’t one answer to “who regulates crypto”—it depends on how the crypto is set up, designed, and used.

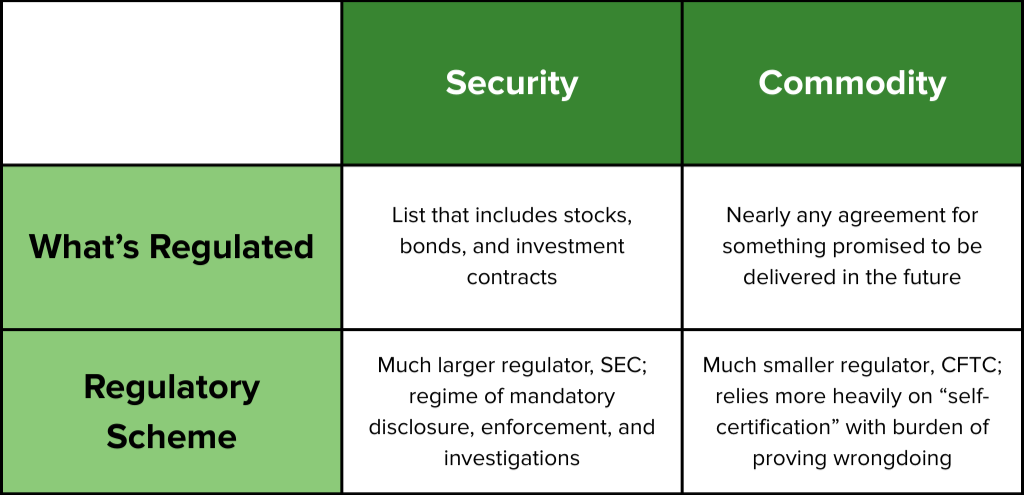

Existing law provides that companies that offer “securities” are regulated by the Securities and Exchange Commission (SEC) and must follow laws and regulations implemented by that agency. Companies that offer “commodities” are regulated by the Commodity Futures Trading Commission (CFTC). (Contracts for future delivery of commodities are known as “derivates.”)

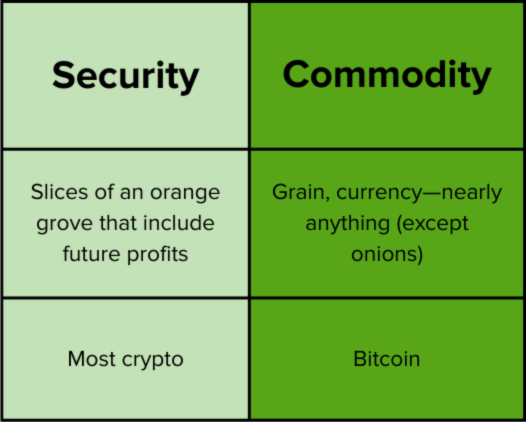

The law provides a list of securities that are regulated by the SEC, including stocks and bonds as well as the broad category of “investment contracts.” In the famous Howey case, the Supreme Court laid out the legal test for what constitutes an “investment contract.” In that case, a hotel sold segments of an orange grove to its guests and claimed it was just selling real estate. But the court found that the company was actually offering securities, because the purchasers also received profits from the company’s harvesting of the oranges. That made it an investment contract.

In contrast, the CFTC regulates nearly any agreement in which “literally anything,” tangible or intangible, is promised to be delivered in the future. (There’s an exception for onions and a few other things.) These contracts have their origins in risk management for agricultural products. For example, a grain producer might sell part of next year’s harvest, to smooth out its income stream. Today, the CFTC regulates a dizzying variety of contracts in agriculture, minerals, energy, finance, and many other industries. The CFTC also has limited authority to police fraud for commodities being bought or sold immediately, rather than in the future.

How Crypto Fits In

Although crypto is new, and some of the legal issues are complicated, courts, regulators, and even the crypto companies themselves weren’t having a lot of trouble applying the existing legal framework to crypto. Most courts that considered the issue found that most types of cryptocurrencies were securities, and prominent regulators from both political parties agreed. There was also bipartisan agreement that some types of cryptocurrencies—most notably Bitcoin—were not securities but rather commodities. The distinction has primarily been based on whether one corporation is offering the crypto and cultivating it as an ongoing investment, making it a security. That isn’t the case, for example, with Bitcoin, which isn’t “cultivated” by a particular company on an ongoing basis.

Some companies offering crypto accepted this state of affairs and began to comply with the securities or commodities rules, where appropriate. However, other crypto companies have been pushing for years, largely unsuccessfully, to avoid treatment as securities. They have primarily argued that “uncertainty” about crypto’s treatment under the law makes it difficult for them to do business. Those arguments aren’t particularly credible, given that the SEC explained how the law applied to crypto and offered to provide any needed additional guidance.

Why Crypto Doesn’t Want to Be Considered a Security

Nonetheless, with a Republican White House and congressional majority that have favored financial deregulation, crypto lobbyists are taking another run at having crypto treated as anything other than a security regulated by the SEC. Among other deregulatory efforts, they would prefer that crypto be regulated by the CFTC instead.

As Roosevelt has explained, classification as a security triggers the SEC’s proactive—and protective—mandatory disclosure, enforcement, and investigations regime. Many of these provisions date to the New Deal, after thousands of families lost their life savings in bogus securities leading up to the Great Depression. The SEC subjects all participating entities—which, for crypto, includes issuers of crypto, exchanges, brokers, and digital wallet platforms—to these requirements. In contrast, the CFTC relies more heavily on “self-certification” and often has the burden of proving wrongdoing before it can act.

The CFTC doesn’t have experience regulating markets in which companies raise trillions of dollars from investors. The CFTC today mostly regulates a largely business-to-business market of sophisticated players. The SEC also has historically had a budget and staff somewhere between six and eight times larger than the CFTC’s. Without a significant investment of more resources in the CFTC, there is a real concern that CFTC regulation of much more of the crypto market would be close to no regulation at all.

Why the Crypto Regulatory Framework Is So Important

Right now, only 17 percent of Americans have ever used cryptocurrency. Even so, crypto is starting to creep into the mainstream, including through retirement accounts. Indeed, the Trump administration is pushing for more crypto investment in retirement savings, like in 401ks. If people’s retirement security is on the line, it will be crucially important for crypto investments to be safe and regulated. The worst-case scenario is if people think that crypto assets are secure when they’re actually not.

Weakening the protections surrounding crypto could also have big consequences for our economy and financial system. At present, companies raise a lot of money for their endeavors through the capital markets regulated by the SEC by issuing products like stocks and bonds. But if crypto becomes an attractive loophole precisely because investors don’t receive critical protections, that could trigger a stampede of companies using crypto to raise money instead. So weak regulation of crypto could blow a hole in our financial system that sucks in people who don’t normally invest in crypto when they invest in regular companies.

The result could be a massive shift in our economy toward investments in which investors aren’t protected—the same circumstances that literally led to the Great Depression.

Related Resources on Crypto Regulation

What Would the New Crypto “Market Structure” Bills Do, and What Dangers Do They Pose?, Roosevelt Institute

By Brad Lipton Opens in new windowThe Progressive Case for Crypto Regulation, Roosevelt Institute

By Emily Divito and Joseph Miller Opens in new windowCrypto Skeptics’ Supreme Risk: The Danger of Relying on Courts to Decide Crypto’s Fate, Roosevelt Institute

By Todd Phillips Opens in new windowUnderstanding Crypto 10: DeFi: Shadow Banking 2.0?, The Rational Reminder Podcast

By Prof. Hilary Allen Opens in new windowThe SEC's Excellent Record on Crypto: Regulation & Enforcement

By Better Markets Opens in new windowCongress Must Not Provide Statutory Carveouts for Crypto Assets

By Center for American Progress Opens in new windowWritten Statement before the US Senate Committee on Banking, Housing, and Urban Affairs

By Lee Reiners Opens in new windowAuthor

Brad Lipton

Director, Corporate Power and Financial RegulationAs director of the corporate power and financial regulation program, Brad Lipton leads Roosevelt's work on the rules governing financial institutions and other corporations to produce a more equitable economy.