Next Week’s Social Security Report Likely Brings Bad News. Here’s What It Really Means.

June 5, 2026

By Stephen Nuñez

When the Social Security Trustees Report is released next week, we should likely expect bad news about the Social Security trust fund. Why?

The program depends on a healthy economy where people have steady work and rising wages, and one where a broad enough tax base can keep benefits flowing. When wage growth slows, and more income escapes Social Security taxation (as is true today), the trust fund takes a hit.

This does not mean that Social Security is failing. It means the economy is failing to support Social Security.

We need a radical reinvestment in the nation’s most reliable social insurance program. When you walk through how the program works and what it means for people who rely on it, it’s clear why.

The Trust Fund Keeps Benefits Whole

The Old Age and Survivors Insurance (OASI) Trust Fund is how the Social Security Administration (SSA) funds OASI (“Social Security”) benefits. Social Security is a “pay-go” system, meaning it uses current revenues, largely from Federal Insurance Contributions Act (FICA) payroll taxes, to pay for current benefits.

In years when revenue is greater than benefit payments, the excess is invested in interest-bearing Treasury bonds, creating a “reserve.” In years when benefit payments exceed incoming revenue, which has been the case for the last 17–18 years, the Social Security Administration draws on these reserves to make up the difference. This is the only option because, without congressional authorization, the Social Security Administration cannot borrow or draw on general tax revenue to make benefit payments.

The reserve depletion date, then, is the point at which the OASI Trust Fund reserve would no longer have sufficient funds to pay fully scheduled benefits on time. If the reserve were depleted without action by Congress, SSA would, given tax revenues, only be able to pay roughly 77 percent of current benefits. This is not “bankruptcy,” but it would create a dramatic shortfall that the government would have to deal with.

The Social Security Administration has known for at least 15 years that the trust fund reserve would reach this point sometime between 2033 and 2035 (last year’s report put that date at the first quarter of 2033). That range is about 30 years earlier than expected at the time the program was last reformed in 1983.

The Economy Broke the 1983 Math

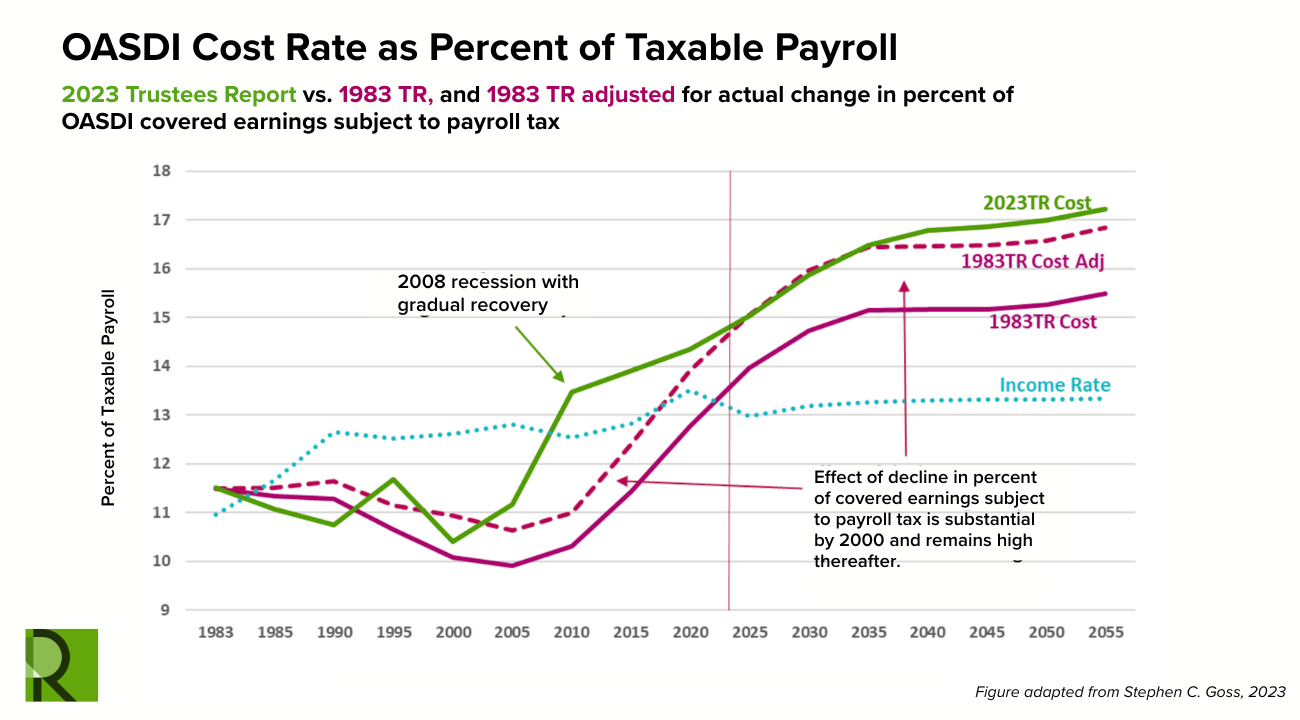

Contrary to popular belief, this is not due to the aging of our population, the so-called boomer retirement narrative. When Congress amended Social Security in 1983, it did so armed with demographic projections from the Social Security Trustees Report that have proven incredibly reliable. The Office of the Chief Actuary of the Social Security Administration accurately predicted demographic changes, including fertility, longevity, and immigration, between then and now (but see below for more recent immigration figures). And the reforms to OASI’s tax and benefit provisions that Congress passed also accounted for these trends.

If demographics were the only factor, then Social Security would have remained solvent until roughly 2063. But Social Security’s health is fundamentally tied to the health of the economy and of the American worker.

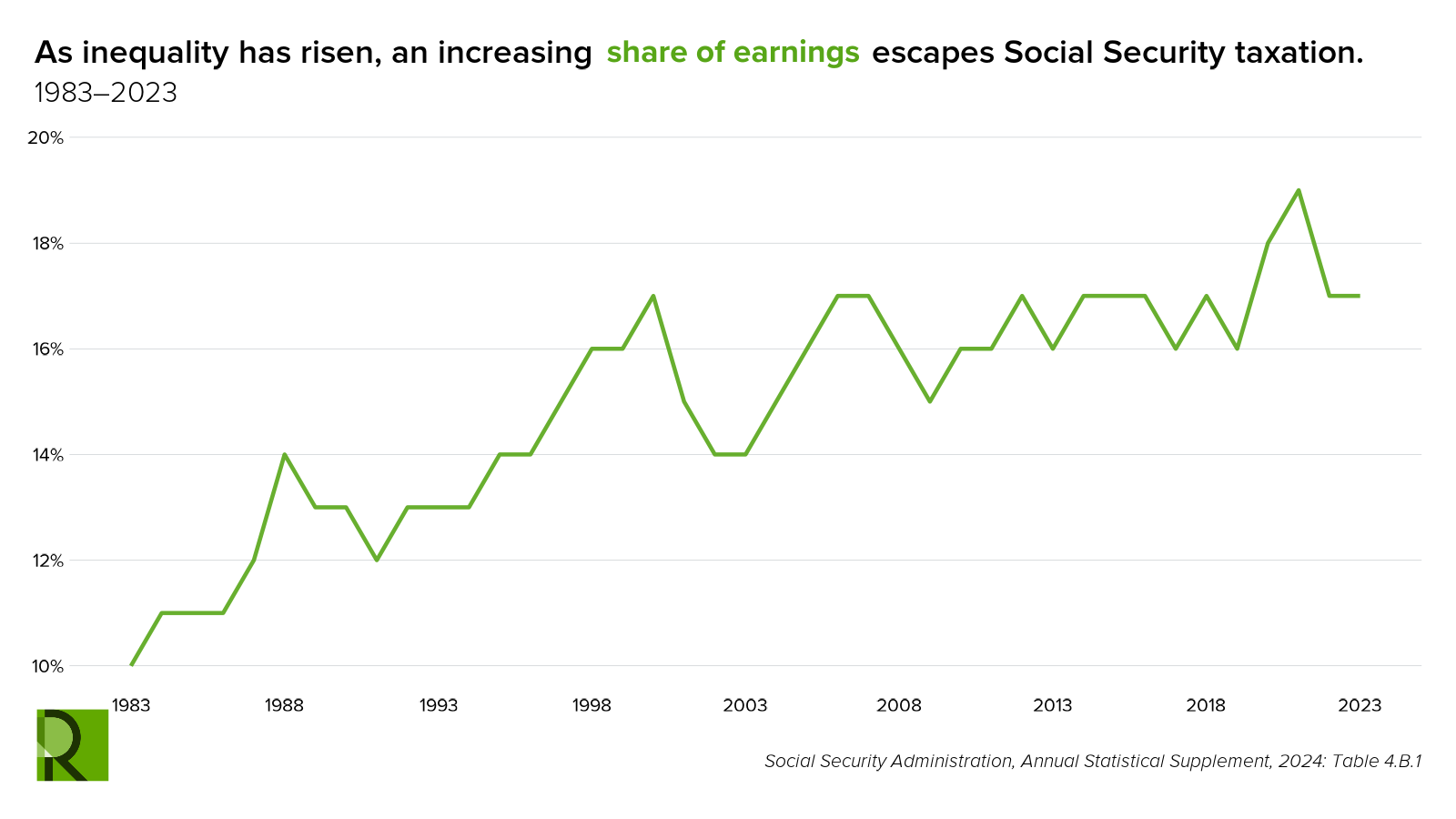

This accelerated insolvency date is, instead, due in large part to rising income inequality and the depth and slow speed of recovery from the Great Recession, neither of which were accounted for in the 1983 amendments. Rising income inequality starved the fund of expected revenue (and the opportunity to build reserves) because the vast majority of earnings gains went to workers with earnings that exceeded the FICA tax cap, which did not grow fast enough to capture them. And the slow recovery from the Great Recession led to a prolonged period of higher unemployment, slower earnings growth, and more early retirements than expected.

This year’s Trustees Report will very likely show the reserve depletion date coming sooner rather than later. While long-run demographic and macroeconomic trends dictate the approximate range of the depletion date, the health of the economy in the immediate run-up to depletion can shift it slightly forward or backward. And current deteriorating economic conditions, including somewhat higher unemployment, slower earnings growth, and the first period of net negative immigration in over 50 years, are enough to cost us a year or two of solvency, which only accelerates the challenge Congress will soon face.

Congress Can Protect Benefits

The SSA has never failed to meet its payment obligations. Since it has never happened before, it is unclear what legal flexibility the Social Security Administration would have to prioritize payments if Congress did not act. It may be able to stagger payments or focus on maintaining full payments to lower-income households. Or it may be required to institute an across-the-board cut greater than 20 percent to all benefit payments.

This is not a crisis that calls into question the viability of Social Security. That’s precisely why people should not hear “depletion date” and expect their checks to simply stop. But our leaders must act and should be prepared for what comes next.

The math is not difficult. Several different reform proposals could close the fiscal gap. But only some of these protect retirees and their families and deliver on the original, Rooseveltian promise of the program. Congress has a choice: shrink the program through benefit cuts and a higher retirement age (selling out future generations), or protect benefits by raising new revenue and requiring the wealthy to pay their fair share.

Authors