Thinking Longer Term While We Wait for News: Previewing May’s Economic Data

May 5, 2026

By Michael Madowitz

May is set to be an eventful month in the economy. In spite of a lot of data last week, we’re still waiting to see the full impact of the Iran war on the numbers. The first ripples of the Hormuz shock on prices in last month’s Consumer Price Index and Producer Price Index data were significant, but small relative to the expected impact now that the crisis has lasted long enough to increase US energy exports. We haven’t seen a shock in jobs data so far—weekly unemployment insurance claims look pretty calm for April—and last month’s jobs report was a continuation of the ongoing trend.

Stepping back from the current crisis, this is an opportunity to focus on deeper questions while we can.

Questions Still Loom About New Fed Chair

First, there’s likely to be a new Federal Reserve chair at some point by June’s Federal Open Market Committee meeting, which raises questions about inflation, full employment, and how the central bank might respond to a potential recession. Kevin Warsh has been nominated to replace Jerome Powell after his term as chair expires next week. We don’t know much about what Warsh would do for jobs, even after his Senate hearing last month. Some of that could be attributable to the greater ambiguity he wants to bring to Fed policy, but most of it is due to an underwhelming Senate: The full banking committee was present at his hearing, but didn’t ask a single question about what he would do in a future recession.

Inflation remains a very important issue, but at today’s 3.5–3.75 percent federal funds rate, the Fed does not have room to cut the roughly 5 percentage points it has needed for modern recessions. This makes it critical to understand what the next Fed chair plans to do when needed most. Furthermore, Warsh has been highly critical of other tools the Fed began using since it ran out of room to cut rates during the 2008 recession.

Full employment was also low on the Senate’s agenda, to the extent it was on the agenda at all. A key question about full employment from Senator Raphael Warnock (D-GA) went entirely unanswered by the prospective next Fed chair, in deference to jokes about colleges. A nominee who wanted to signal a commitment to full employment might have tried to answer that question a bit harder.

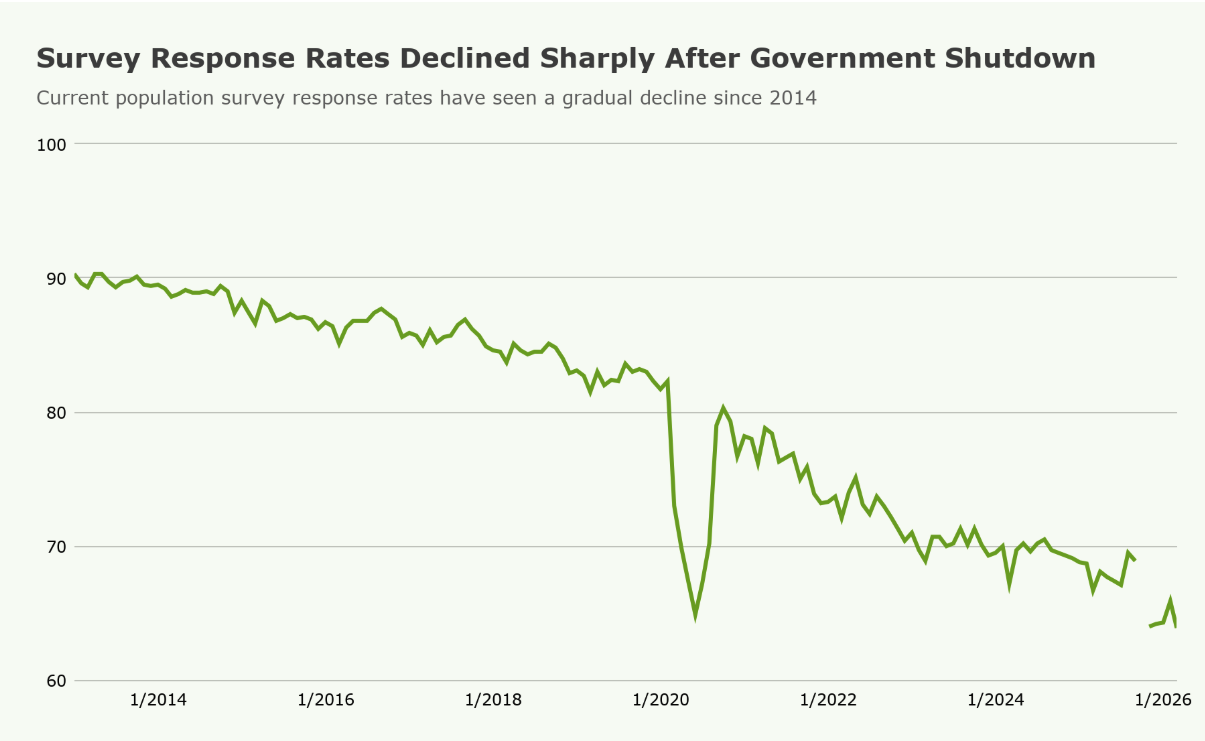

The Decline in Survey Response Rates

The other mystery to ponder this month will be in the jobs numbers. The payroll survey was good last month; the household survey was not. Some of the payroll gains came from striking health-care workers returning to work, but the household survey showed a third consecutive month of declining employment and labor force participation rates, with both falling to post-2021 lows. These data tend to move in the same direction over time. Although short-term divergences have happened before, with survey response rates at historic lows, it’s worth looking a little closer at the recent gap.

One question worth asking is whether the government shutdown has changed response behavior. Survey response rates have been declining over time in general, including response rates to the household survey, but the dropoff since the government shutdown in October and November of last year has been sharp: Responses are the lowest they have ever been. This raises questions about Bureau of Labor Statistics staffing levels and the retention of institutional experience over that period. If the gap between household data and payroll data continues to widen, it’s worth asking what it will take to fix response rates so we can continue to reliably cross-check the two data sources.

Author