Since Kalshi’s Launch, Ordinary Users Have Lost Half a Billion Dollars

July 7, 2026

By Brad Lipton and Toyosi Odusola

Prediction markets offering contracts on virtually every topic are one of the fastest-growing industries in the United States, just trailing behind AI. Who wins and loses in these markets? How is their operation shaping our society? And what rules do we need to manage them?

In a new four-part series, The Hidden House: Prediction Markets and How They’re Shaping Society, we will explore these questions and more. This first installment explains how ordinary participants in prediction markets systematically lose money to the most sophisticated traders, who use distinct methods to capture the vast majority of gains.

- The second will look beyond the consumers who participate in prediction markets to the effects these markets are having on our society more broadly.

- Next, we’ll show how rapidly embedded these markets are becoming throughout key institutions such as the media, finance, and sports, highlighting the threat of path dependence—the idea that decisions made early on in the trajectory of an institution can make changing course later on harder to achieve—and the consequent urgency of regulation.

- The final installment will compare the rules that apply to prediction markets to those that apply to traditional gambling.

Prediction markets advertise that their platforms are better than traditional gambling because users are betting against each other rather than against a “house.” But the reality is that ordinary people participating in prediction markets are largely betting against professional traders using sophisticated methods. And the evidence suggests that ordinary users seem to do even worse in prediction markets than in traditional gambling contexts.

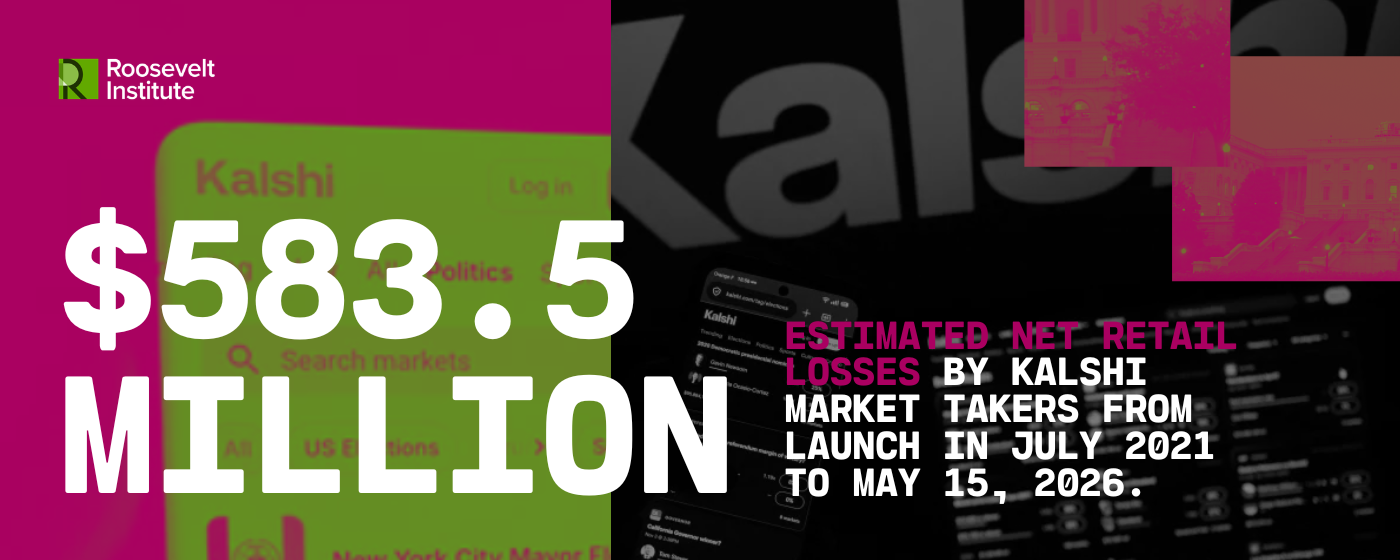

Our first-of-its-kind analysis of data on Kalshi, now the largest prediction market in the United States, found that ordinary users of the platform have lost more than half a billion dollars from its launch in July 2021 to May 2026. What’s more, when retail traders made money, it was mostly on a small number of the largest wagers.

The trading volume on Kalshi and Polymarket (the next largest prediction market platform) grew to $24.2 billion in April 2026, up from $1.8 billion a year ago. The industry is projected to reach $1 trillion in trading volume by 2030.

While prediction markets have been around for a long time in some form or another, they have exploded in popularity since the 2024 election, and more recently, the start of the NFL season in the fall of 2025. Two recent high-profile cases of insider trading on Polymarket have also increased their notoriety. In the first, a US soldier, Gannon Ken Van Dyke, was charged with allegedly using nonpublic information to make over $400,000 predicting the capture of Venezuela President Nicolas Maduro in January 2026. That was followed shortly after with a charge against Google employee Michele Spagnuolo, who allegedly used internal company data to make over $1.2 million betting on Google’s Year in Search 2025 results in December 2025.

Existing research, largely on Polymarket, suggests that the vast majority of people participating in prediction markets (retail traders) lose money, with the profits being captured by an extremely small number—the top 0.1 to 1 percent—of sophisticated users. These traders participate in these markets in ways that are entirely different from how the average user interacts with them. Our original analysis of data that was publicly available on Kalshi shows just how much money retail traders have lost on that platform, and how little of any winnings are from small bets. The lack of transparency about who is really on the other side of the bet—and is offering the contract at particular odds—may be part of the reason why people seem to fare worse in prediction markets than in traditional gambling, since in traditional gambling it is clearer what is going on.

While we were doing the research for this piece, an official Kalshi collaborator, a company called Dune, cut off public access to information about trades on Kalshi. This happened a few days after negative media coverage based on analysis of that data. Dune has announced that the information will now only be available for customers who pay $40,000. (According to Dune, the company prepared the policy change before the analysis was released.) Although there has been commentary about this change on Twitter/X, we have not seen any coverage of it in the media (except on Sportico, the site that published the original coverage).

Existing Studies: A Small Number of Bettors Take Everyone Else’s Money

Several existing studies, primarily of Polymarket data, have shown that sophisticated traders systematically take the money of ordinary users, who can fare worse in prediction markets than they do in traditional forms of gambling, such as sportsbooks or casinos. Multiple studies of Polymarket data have shown just how much of the money flows to a tiny group of people and away from everyone else. One study analyzing comprehensive data involving millions of users and more than half a billion trades from 2022 to 2026 found that the top 1 percent of users captured 76.5 percent of all trading gains. Following up on this research, the Wall Street Journal’s analysis of more than a million Polymarket accounts found that 67 percent of profits go to just 0.1 percent of users, with fewer than 2000 accounts netting almost $500 million since November 2022. Another study found that only the highest-volume traders—those with more than $500,000 in activity—recorded positive returns.

Research Shows Top Polymarket Users Capture Gains

| Users | Gains |

|---|---|

| Top 1% | 76.5%1 |

| Top 0.1% < 2000 Accounts | 67% Almost $500 million2 |

| Highest-volume traders (more than $500k in activity) | Only positive returns3 |

- Source: Akey et al. ↩︎

- Source: Wall Street Journal ↩︎

- Source: Finance Magnates ↩︎

Not nearly as much research has been published on Kalshi, but analysis of Kalshi transaction data has found a systematic wealth transfer from market “makers” to market “takers”—that is, from traders offering bets, with odds they believe are in their favor, to those who accept such offers. (In theory, anyone can offer such a bet, but the evidence shows that it’s largely professionals who do so—more on their methods below.) This dynamic exploded after the number of Kalshi users surged following a ruling allowing it to offer election contracts leading up to the 2024 election, and is strongest in categories that garner a lot of engagement and marketing push to retail consumers, such as sports and entertainment. Kalshi itself recently admitted that there are nearly three times as many people losing money as making it on its platform. Additionally, a recent analysis of parlays (bets that only pay out if a combination of two or more events occur) on Kalshi found that retail bettors lost roughly $117 million between just January and April 2026.

Kalshi itself recently admitted that there are nearly three times as many people losing money as making it on its platform.

With Kalshi overtaking Polymarket in monthly US trade volume ($6.2 billion on Kalshi compared to $718.2 million on Polymarket for the month of May 2026), capturing 90 percent of the US prediction market share, information about how users perform on Kalshi is increasingly crucial. To further fill out that picture, we performed our own, first-of-its-kind analysis of publicly available Kalshi data—until that source went dark.

The Dynamic on Kalshi: The Data Goes Dark

Until recently, Kalshi provided information about transactions on its platform to the public through its official partner Dune. (Unlike Polymarket, Kalshi has never provided detailed information about how individual users perform on its platform.) While researching this piece, we captured a snapshot of outcomes on Kalshi from Dune before they revoked public access. (Kalshi itself theoretically offers that information through a publicly available interface, but the huge amount of data there easily overwhelms programs running on a regular computer.)

We analyzed more than 400 million trades (with over $32 billion in total volume) on Kalshi from its launch in July 2021 to May 2026. The mean bet size was $75.20. The top trading category, by far, was sports, with nearly 280 million trades, followed by crypto (bets about crypto, not trades of crypto) with almost 79 million trades, and exotics—complex contracts, including most parlays—with more than 18 million trades.

We estimate that retail traders (market takers) on Kalshi have lost over half a billion dollars—$583.5 million. More than two-thirds of those losses ($371.6 million) were from sports alone. (Exotics and mention markets were also in the top five categories for retail losses, with over $100 million and $16 million in losses, respectively.) And when retail traders made money on Kalshi, it was mostly on a small number of the biggest bets. We find that 63.2 percent of all “taker” revenue on Kalshi flowed to just 6.3 percent of matched orders, those with a dollar value of at least $200.

We intended to perform further analysis of Kalshi data. However, on May 13, 2026, while we were researching this piece, Sportico published its article analyzing Kalshi data available on Dune and reporting that Kalshi retail bettors lost $117 million on parlay bets in 2026 alone. Two days later, on May 15, Dune disabled its public-facing Kalshi tables that offered detailed information on transaction outcomes. (Dune has denied that there is any connection between these events.)

On May 20, Dune launched a database of information for markets offered on Kalshi and Polymarket. As part of this launch, Dune has now placed formerly public-facing Kalshi data behind a $40,000 paywall. We reached out to Dune’s sales team on May 21 requesting access to future data for a one-time use case, but have not received a response. (Dune did tell us we could publish our analysis of the data we were able to pull previously.)

Why Sophisticated Traders Outperform Ordinary Bettors

In addition to the possibility of insider trading, the reason that sophisticated traders do so much better than anybody else on prediction markets is that their methods fundamentally differ from those of retail traders who make individual bets based on their intuitions or analysis of publicly available information. Unlike in a traditional sportsbook—where the odds are made by the “house”—everyday users in prediction markets are entering into contracts at odds offered by sophisticated traders, who are both on the other side of the bet and may take advantage of expensive information and elaborate software.

Sophisticated traders, also known as “sharps”, may spend hours researching, building models, and purchasing proprietary data to inform their bets. (The traders who predominantly make the market are sometimes called “dealers.”) Rather than excluding “sharps,” as casinos or sportsbooks sometimes do, prediction markets empower them to take advantage of ordinary participants using their sophisticated methods. For example, prediction markets provide financial incentives to “market makers” and allow them to operate with near-anonymity. As a result, the underlying dynamic may not be clear to ordinary users of prediction markets who receive little information about who they are betting against.

Top earners on prediction markets are also much less likely to bet that extremely low-probability events will happen, whereas casual traders lose a disproportionate amount of money on these types of bets. Some of the low-probability events popular with retail traders include so-called “mention” contracts—where people bet that someone will say a particular word in a particular venue—as well as extreme comebacks in sporting events and parlays.

Additionally, sophisticated traders pay significant sums of money for proprietary data streams, which they analyze to inform their trading. And they use technology such as AI to analyze this information and place frequent (even thousands of) bets over the course of a single day to take advantage of small shifts in odds. (The Wall Street Journal described one firm that spent more than $200,000 per year on data feeds and “AI coding agents and servers.”)

It isn’t clear that everyday participants in prediction markets know how sophisticated the person or the methods on the other side of the transaction are.

Sophisticated traders on prediction markets also have an important partner in their activities: the finance industry. Well-funded investors have thrown money at traders who exploit these advantages to profit at the expense of everyday people. For example, the parent company of FanDuel announced last month that it had started funding bets on a prediction market platform. (In addition to betting against professional traders, users on Kalshi might also be betting against the exchange’s trading arm, Kalshi Trading.)

The key point is that the deck is systematically stacked against everyday users participating in these markets, even if, as prediction markets commonly advertise, there is technically no “house” on the other side of the bet. It may look like betting against your buddy on the big game, but prediction markets are closer to playing slots—except when people pull the lever on a slot machine, they know they’re playing against a regulated casino. In contrast, it isn’t clear that everyday participants in prediction markets know how sophisticated the person or the methods on the other side of the transaction are.

Indeed, the evidence suggests that ordinary participants in prediction markets lose more money than participants in other forms of gambling. One study found that the median user on a sportsbook lost 5 percent of what they bet, as compared to 8 percent for the median user on prediction markets. Similarly, a study by the University of Nevada, Las Vegas found that the average slot machine in that state takes 6.55 percent of the money put in.

The evidence suggests that ordinary participants in prediction markets lose more money than participants in other forms of gambling.

Conclusion: Beyond Financial Harm

The harm to some people participating in prediction markets can go beyond the monetary. Researchers have raised alarm about addictive designs that may lead prediction market participants to develop addictive behaviors, betting more and more to earn back losses, leading to a spiral of financial harm, instability, and potential bankruptcy. Research also links sports betting, and particularly losses when betting on sports, to a rise in intimate partner violence, financial precarity, and adverse mental health outcomes.

These are just some of the ways that trading on prediction markets can hurt people. But prediction markets may also pose an even larger threat to our society. We will cover this and more in the second installment of this four-part series.

Authors

Brad Lipton

Director, Corporate Power and Financial RegulationAs director of the corporate power and financial regulation program, Brad Lipton leads Roosevelt's work on the rules governing financial institutions and other corporations to produce a more equitable economy.

Toyosi Odusola

Senior Research AssociateAs a senior research associate at Roosevelt, Toyosi Odusola supports think tank staff and fellows in their research.