What Would the New Crypto “Market Structure” Bills Do, and What Dangers Do They Pose?

September 26, 2025

By Brad Lipton

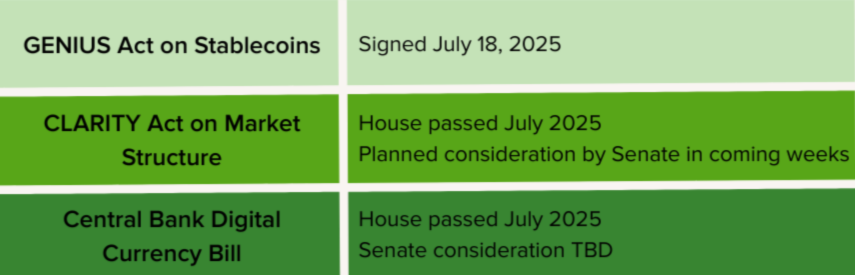

The Senate has announced that it will consider a significant bill on cryptocurrency in the coming weeks, the second in a planned trilogy of crypto laws. This bill would govern crypto’s “market structure”—how companies offering crypto are classified for regulation.

If you need a bit of a refresher on how the government regulates crypto under existing law, including what oranges and onions have to do with it, take a look at my previous blog post on this topic.

A version of this bill, the CLARITY Act, passed the House of Representatives in July, and the Senate Banking Committee released a draft of similar legislation a few weeks ago. Although some Senate Democrats voted for the first bill in the crypto trilogy—the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act—it is not clear whether they will support congressional Republicans’ “market structure” legislation. These “crypto-friendly” Senate Democrats have issued their own “framework” for market structure legislation.

This blog post summarizes the House and Senate bills and the potential effects they could have in plain language. The bills’ weak, patchy regulatory framework creates financial risks that could have vast implications for the economy and people—far beyond just the market for crypto. Indeed, these bills could dramatically undermine the way that the government protects investors more broadly in the United States. Critics of the bills note that loopholes and lax regulation like those proposed in these bills contributed directly to various financial crises in American history, including the Great Recession and Great Depression.

Why We’re Talking About “Market Structure”

As explained in my previous post, companies offering “securities” are regulated by the Securities and Exchange Commission (SEC) and must follow a regime established in the aftermath of the Great Depression and updated thereafter to inform and protect investors. Companies offering “commodities” for future delivery, by contrast, are regulated by the Commodities Futures Trading Commission (CFTC). (Commodities were historically physical products like grain, but now include “intangible” items in the world of finance.) Although courts, bipartisan policymakers, and even some industry players largely agreed about how crypto fits into this regime, crypto lobbyists have claimed that “regulatory uncertainty” is making their business difficult.

That said, the existing regulatory regime has significant gaps with respect to crypto—just not ones that the pending legislation focuses on. For example, under existing law, the CFTC has only limited authority to police fraud and market manipulation when commodities are being sought or sold for immediate delivery, rather than in the future. Modest tweaks to the regulation of securities could also better equip the SEC to oversee the crypto under its jurisdiction. Progressives have also stressed the need for crypto firms to be regulated like other financial institutions, such as banks, when they do things that those institutions do, like taking deposits.

Weak Protections for Investors

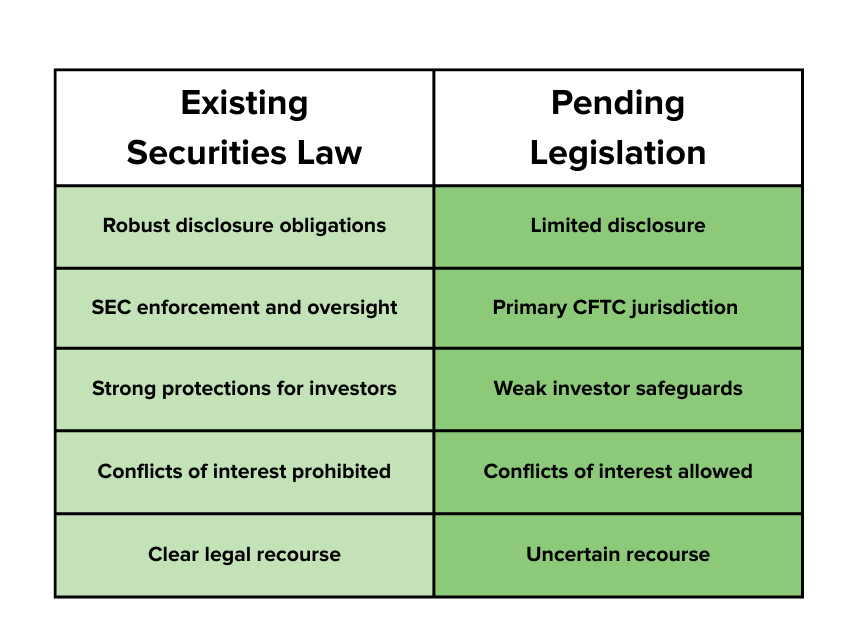

Although Republican leaders have sometimes derided legislation for being long, the CLARITY Act and its Senate counterpart are extremely lengthy and complicated, clocking in at over 150 pages. Both would create a whole new set of rules for crypto regulation that are weaker than the protections that typically apply to investments favored by individual people and largely strip the SEC of jurisdiction to enforce those rules, in favor of the CFTC.

Critics of the legislation have stressed the fundamental weakness of the rules that it would apply to crypto. This includes permitting conflicts of interest, where “a crypto exchange could manage trades in ways that benefit its high-paying customers over other customers.” In sum, as one leading expert testified: “Compared to the foundational securities laws, the CLARITY Act offers worse disclosures with lower standards of legal liability for issuers, lessens protections for investors when interacting with intermediaries like brokers, and would make buyers of crypto assets more subject to predation and manipulation on exchanges.”

The bills would also exempt certain categories of assets from even these rules. Although the CLARITY Act that passed the House and the current draft of the Senate bill have much in common, the Senate bill would, among other things, expand these exemptions.The bills also would both exclude certain types of crypto from state protections.

Questions About Enforcement

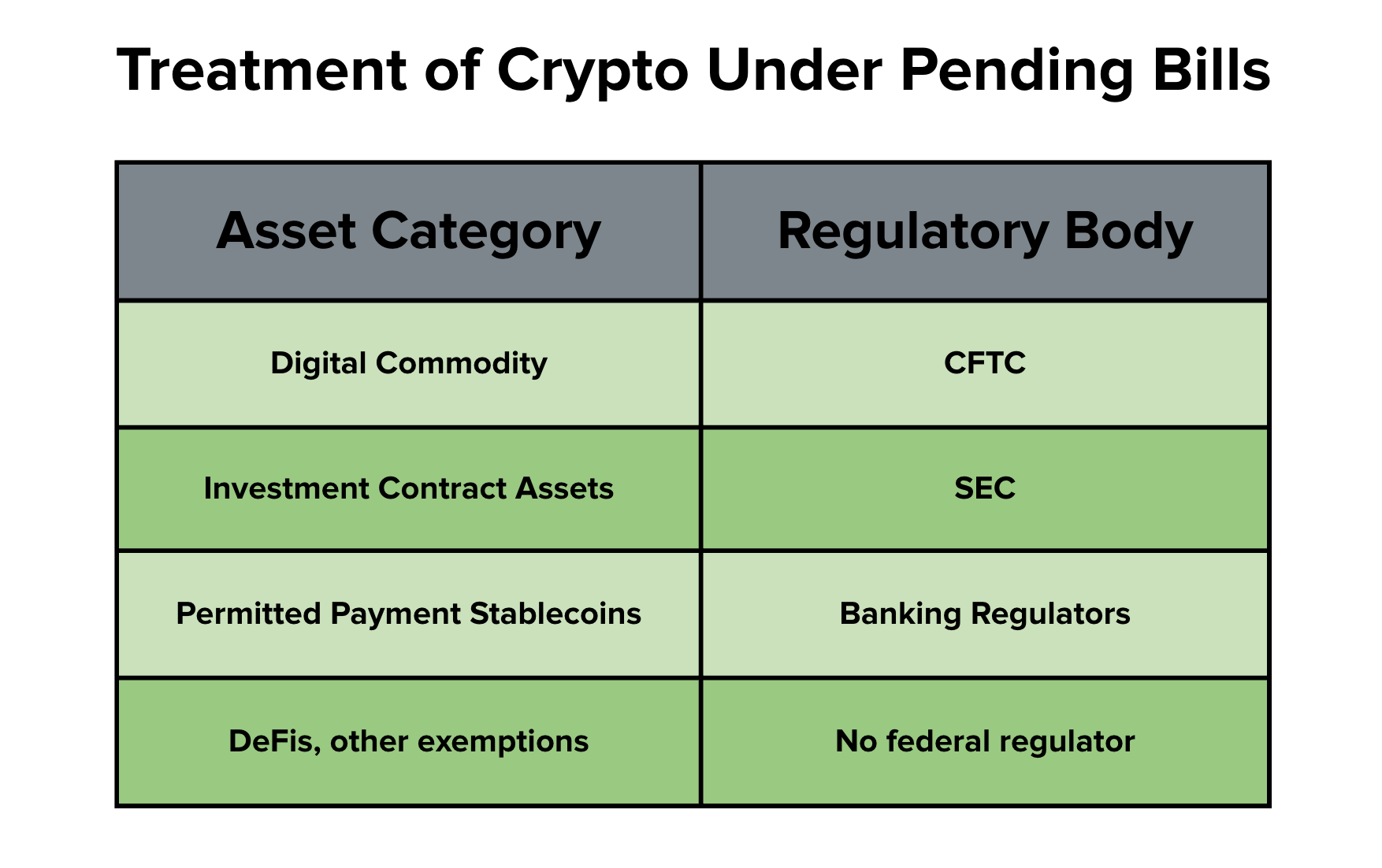

With respect to enforcement, the bills would divide crypto assets into three novel categories—“digital commodities,” “investment contract assets,” and “permitted payment stablecoins.” These categories would be based on complex distinctions regarding whether the cryptocurrency is “sufficiently ‘decentralized.’” (So, for example, the bills rely heavily on how much companies “intermediate” between users.) These distinctions are not really related to the economic reality of the investment. This means that companies—including “regular” companies that are not even in the crypto business—could superficially restructure how they raise money using crypto technology to get the different treatment under the law.

These changes would dramatically expand the CFTC’s role and narrow the SEC’s. The CFTC would regulate “digital commodities,” the SEC would regulate “investment contract assets,” and banking regulators such as the Office of the Comptroller of the Currency would have modest authority to regulate “permitted payment stablecoins” (which function largely like cash, but lack deposit insurance). Importantly, even the SEC’s regulation of “investment contract assets” would be quite limited—for instance, sales of those assets to individual investors after the initial offering of the crypto would largely be regulated by the CFTC as “secondary” transactions.

There is a real question about whether the CFTC would be able to enforce even the relatively weak rules that would apply to crypto. As explained in the previous blog post, the CFTC usually regulates transactions between big, sophisticated companies and investors, not markets in which companies raise trillions of dollars from individual people. The bills give the CFTC some authority to charge fees to crypto firms and hire additional personnel, but only for a few years. It is unclear how the CFTC would be able to keep up with its expanded and quite new set of responsibilities.

Potential for Catastrophe

The major concern with both versions of the bill is that this weaker regulatory regime for cryptocurrency could blow a gigantic hole in the financial system, with disastrous results for investors well beyond the crypto market. If these bills become law, many companies—including companies that have nothing to do with crypto—may use crypto to raise money just because a looser set of rules with fewer investor protections would apply. Accordingly, these bills could undermine not only protections that crypto investors receive but protections for investors much more broadly. In a very real sense, these bills aren’t even “about” crypto—they are about weakening the way that our government protects all investors.

There is no better warning on the dangers of leaving investors unprotected than American history. Lax regulation of high-risk financial products helped trigger the Great Recession. And the Great Depression saw thousands of Americans lose their life savings to shady investments with little safeguards, before the creation of modern securities regulations that protect Americans when they invest and build wealth.

The United States will probably eventually regulate crypto more seriously. What’s at stake now is whether we do it the first time or wait until Americans pay a price. If this legislation passes and a catastrophe occurs, nobody who supported it can say they were not warned.

Related Resources on Pending “Market Structure” Bills

Comparing Oranges to Onions: What Is Crypto “Market Structure,” and Why Is It Important?

By Brad Lipton Opens in new windowWritten Statement before the US House Financial Services Committee

By Timothy G. Massad Opens in new windowPrepared Statement, Minority Day Hearing on American Innovation and the Future of Digital Assets

By Hilary J. Allen Opens in new windowWritten Submission Before the US House Financial Services Committee

By Amanda Fischer, Policy Director and COO, Better Markets Opens in new windowLetter in Opposition to the CLARITY Act

By Coalition Opens in new windowTestimony for the US House Ways and Means Subcommittee

By Corey Frayer Opens in new windowAuthor

Brad Lipton

Director, Corporate Power and Financial RegulationAs director of the corporate power and financial regulation program, Brad Lipton leads Roosevelt's work on the rules governing financial institutions and other corporations to produce a more equitable economy.