Against Manufacturing Doomerism: Why and How Making Stuff Matters

May 5, 2026

By Todd N. Tucker and Oskar Dye-Furstenberg

This is a web-friendly preview of the report.

Five Reasons to be Bullish on American Manufacturing

- Manufacturing continues to punch above its weight.

- Past and current US national security and economic security strategy relies on and supports the domestic manufacturing base, and vice versa.

- Addressing the climate crisis means moving toward primarily manufactured (rather than primarily mined) energy.

- Changes in technology may make manufacturing work relatively more attractive.

- There are some areas where the sector remains important in employment terms.

Executive Summary

Unless you are in the middle of the wilderness, almost everything you see is manufactured. Your laptop, pen, car, drywall, cabinet—anything that was not directly plucked from the ground or a tree is a manufactured product. And yet, in recent years, voices across the political spectrum have indulged in what we call “manufacturing doomerism”—the idea that it doesn’t matter (and/or we can’t change) what we make as a country, or even whether we make anything at all. One type of doomer goes beyond the old economic idea of comparative advantage (that countries shouldn’t try to manufacture everything themselves, and that specializing in some goods and trading for others is beneficial) and instead questions whether we even need to worry about manufacturing goods or workers at all, since most workers are in the service industry. Other doomers value manufacturing, but believe that globalization has so hollowed out America’s industrial base that we have ceded our manufacturing destiny to other economic superpowers like China.

This report argues against manufacturing doomerism, showing that the sector has greater importance to the US economy than a simple focus on its job numbers would suggest. Despite employing less than 10 percent of workers, the US manufacturing sector is still the second largest in the world, the second most important in domestic output, the leading funder of research and development (R&D), the top export sector, and the second largest employer of engineers. Manufacturing contributes more than other sectors on a per-job basis to value added (76 percent greater), exports (688 percent greater), and R&D spending (1,288 percent greater). Manufacturing has a particularly large employment multiplier: Every manufacturing job created supports four times as many jobs in communities and supply chains as do jobs created in other sectors. And while the so-called manufacturing wage premium has gone down (along with the prices of manufactured goods) over the globalization era, manufacturing jobs continue to pay more than other jobs on average, and are more likely to be unionized than jobs in other private-sector industries.

Finally, the manufacturing sector will be just as (if not more) important in the future, as the economy shifts from extracting energy to producing it in factories and as geopolitical tensions reduce the dependability of some trade partners we rely on to produce goods. As such, it is essential that the US continue to have an active manufacturing policy.

Introduction

Over the last century, manufacturing has by some measures gone the way of agriculture. Just as agriculture once employed the majority of Americans (an estimated 90 percent in 1790, compared to less than 0.9 percent today1), manufacturing has gone from a peak of employing 37.5 percent of Americans in the mid-20th century to a mere 7.5 percent in 2024.2 In raw numbers, 19.4 million Americans worked in manufacturing in 1979,3 compared to only 12.6 million today—even as the population grew from 225 million to 340 million.4 Despite politicians’ championing of manufacturing,5 it seems that the service sector—the remaining sector of the economy in this three-part conception of the economy—is king, employing 91.4 percent of Americans.6

Understandably, this has led some observers to question whether manufacturing matters, and to ridicule those who say it does (or might). This is the first flavor of what we call “manufacturing doomerism.” At Vox, Eric Levitz has written that pro-manufacturing allies of President Donald Trump

believe that they can bend the arc of history back toward that golden age by dramatically increasing US manufacturing employment. But this is a fantasy. America can only return to the mid-century industrial economy in the sense that it can return to subsistence farming: It is technically possible to embrace an anachronistic mode of production, but only at immense economic cost.7

In 2024, Dylan Matthews at Vox ridiculed the Joe Biden administration’s “foreign policy for the middle class” policy of tariffs on electric vehicles, writing:

The idea that this policy helps the American middle class overall is laughable. Less than one percent of Americans work in auto or auto-parts manufacturing. But over 90 percent of American households have a car, and surging car prices were a huge contributor to the 2021–2023 rise in inflation. Barriers to importing cheap cars make inflation worse and reduce the real incomes of the middle class.8

Also at Vox, Constance Grady made a more sociopolitical argument, claiming that “the incels [involuntary celibates] supporting Trump’s tariffs . . . read Trump’s economic policy as a project of redistributing money and jobs away from women and back to men, ultimately for men’s sexual gain.”9

Some of this backlash is understandable, in light of fairly sweeping and provocative claims made in support of the supposed virtues of manufacturing. Shortly after Donald Trump’s announcement of blanket tariffs in April 2025, on what he called “Liberation Day,” right-wing provocateur Milo Yiannopoulos wrote that “men are depressed and addicted and broken because they have nothing to do. They get no stimulation or satisfaction from BS email jobs. I’m telling you, white Americans will love working in factories again. Making things, in the image and likeness of God the Maker.”10 Trump administration Commerce Secretary Howard Lutnick celebrated that “the army of millions and millions of human beings screwing in little screws to make iPhones, that kind of thing is going to come to America.”11 More concretely, in 2017 Trump trade advisor Peter Navarro said, “We envision a more Germany-style economy, where 20 percent of our workforce is in manufacturing.”12 The Biden administration, for its part, seemed to invite a focus on manufacturing jobs, circulating a fact sheet with endorsements of its climate agenda that mentioned “jobs” 53 times and “manufacturing” 12 times, compared with 3 mentions of “emissions” and 2 mentions of “construction”—where the near-term job creation was concentrated.13

And it is worth remembering that while the US is no longer the world’s top manufacturing nation (that role now belongs to China), it is today still the second largest—producing nearly three times as much manufacturing value added as the number-three country.

This takes us to the second flavor of doomer: those that see the impact of globalization as so totally destructive that US manufacturing is essentially dead. While they think that’s a bad thing (unlike the first doomer variant), both reinforce the idea that manufacturing is America’s past, not its present or future. As an example of the second type of doomer, consider centrist presidential candidate Ross Perot in 1992, who predicted that, if the North American Free Trade Agreement (NAFTA) were signed (as it was by President Bill Clinton a year later), there would be a “giant sucking sound going south” of all manufacturing to Mexico.14 Or more recently, Representative Jared Golden (D-ME) wrote that “America must once again become a nation of producers, not just consumers. Decades of globalization have transformed our country from an industrial superpower to one that relies on other countries for basic goods.”15 If we are no longer a producing nation, then it might be understandable that policymakers and analysts could see reshoring as a lost (or very expensive) cause, especially when China is happy to provide endless, cheap products.

This report argues against such manufacturing doomerism. Manufacturing still matters,16 and active government industrial policy can build more of it. Every country practices industrial policy, helping some industries survive and thrive while discouraging others. Even the World Bank—once the neoliberal citadel for industrial policy skeptics—now suggests the tool can be highly useful for developing manufacturing and other capabilities.17 While outside of the defense and agriculture sectors the US has struggled to have a consistent industrial planning process,18 the beginnings of one for the manufacturing sector were developed during the Biden administration,19 emulating and building on the practices of other advanced economies.20 And it is worth remembering that while the US is no longer the world’s top manufacturing nation (that role now belongs to China), it is today still the second largest—producing nearly three times as much manufacturing value added as the number-three country.

This report seeks to shed light on whether (and how) manufacturing matters. In Section 2, we define key terms and present descriptive statistics on the state of US manufacturing. In Section 3, we examine the economic importance of manufacturing for job quantity, job quality, affordability, national income growth, productivity, innovation, exports, and other sectors. In Section 4, we discuss five reasons to think manufacturing and manufacturing policy will continue to matter in the years ahead, including as a way to deal with the climate crisis and national security threats.

A Look at the Data: Defining and Describing the Manufacturing Landscape

The first step to answering “Does manufacturing matter?” is to define it. “Manufacturing” can be thought of as “anything you can make that you can drop on your foot.” Look around your desk or out your window: Virtually everything you see that fills your house and neighborhood was manufactured by someone, somewhere. Manufacturing scholar Tim Minshall puts it thus: “What happens in all factories can be framed in seven words: they take some inputs to do some kind of processing (people follow some method using machines and materials) to convert them into valuable outputs.”21 The other two sectors that comprise the economy are agriculture (which involves picking or growing, rather than making or assembling) and services (anything you can’t drop on your foot).22

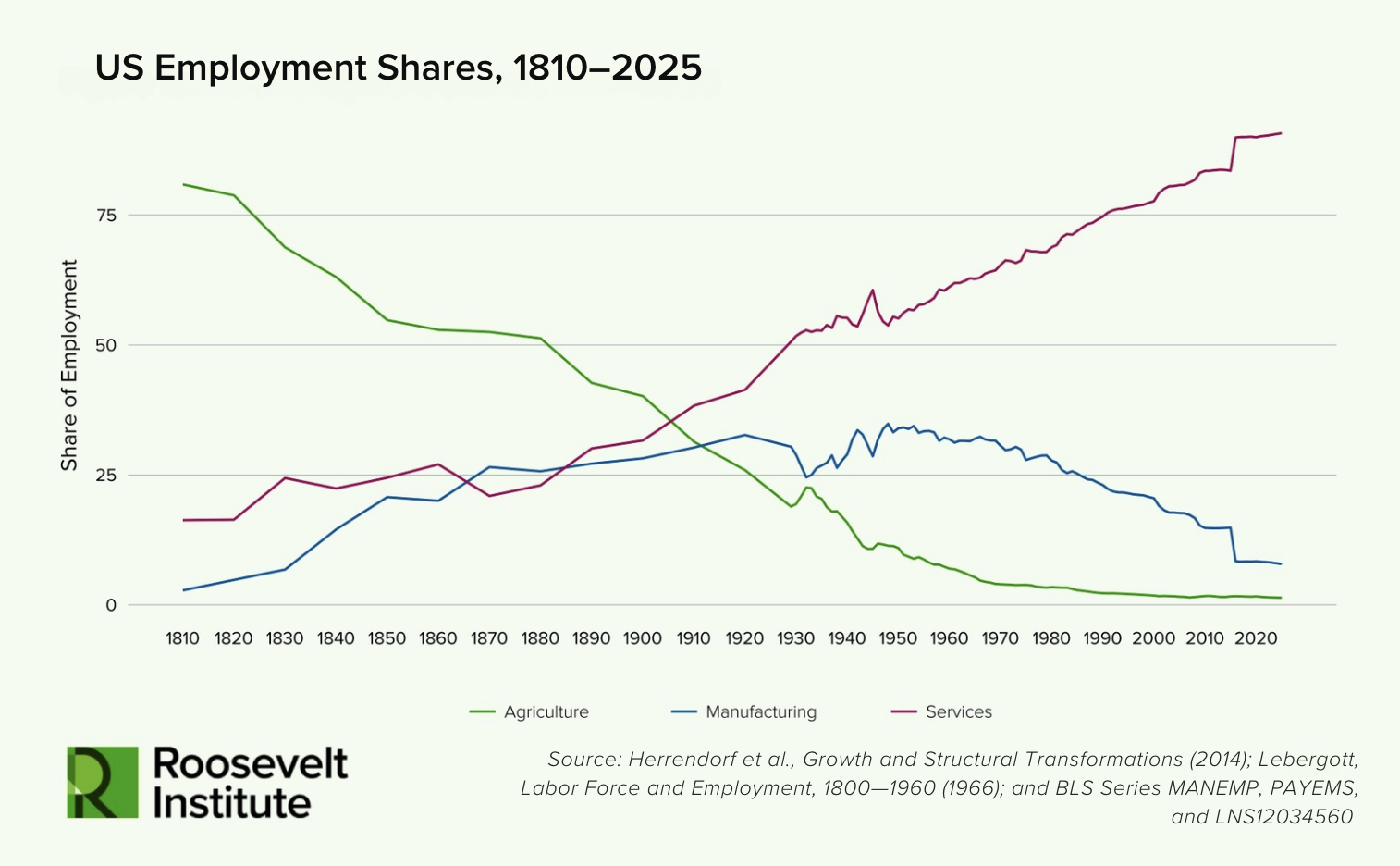

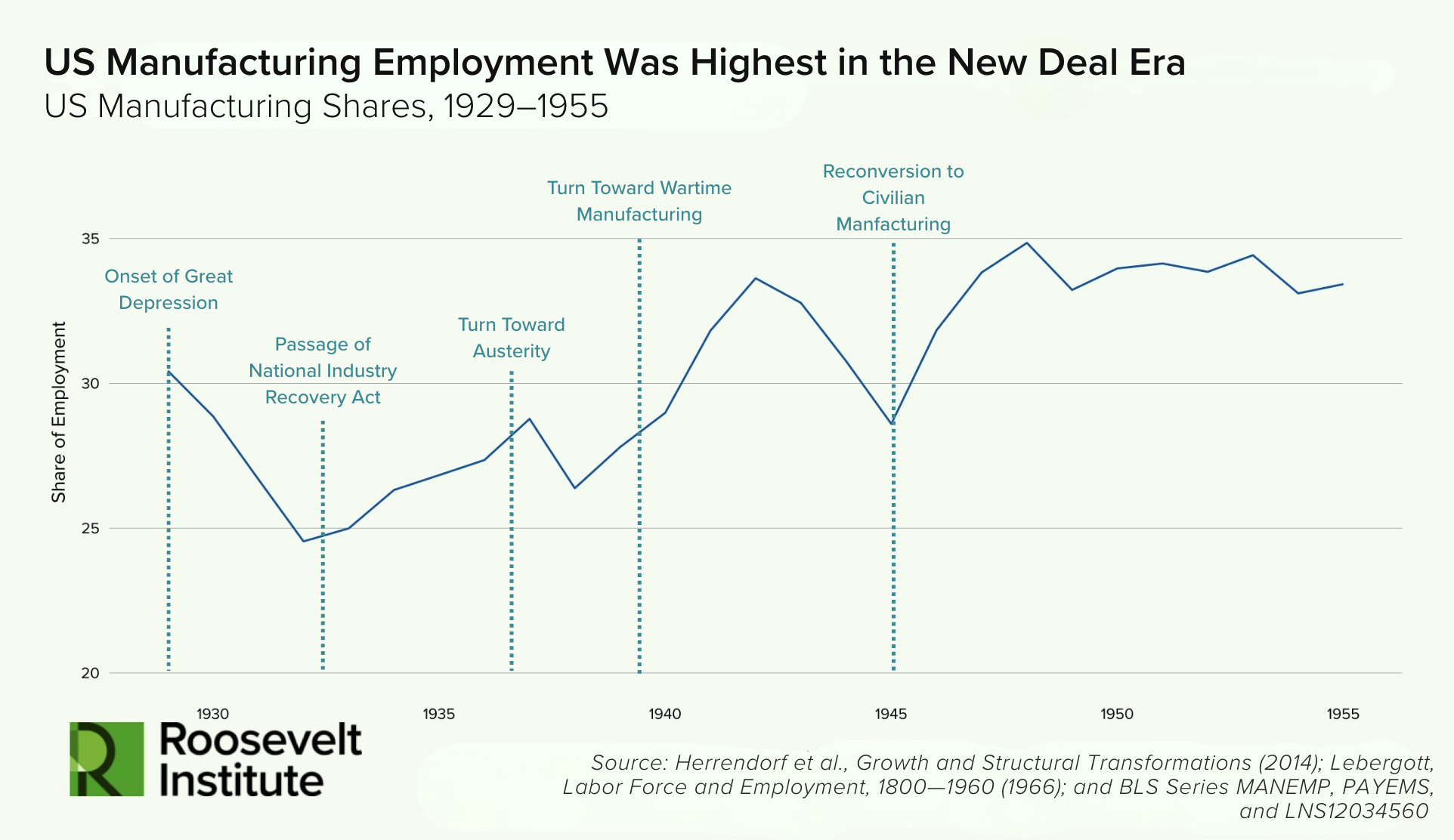

Figure 1a shows the relative importance of these three sectors in employment terms since 1810. As it shows, agriculture once employed the vast majority of Americans, but its employment share has declined every decade. The opposite trajectory is true of services, which has steadily increased its share of employment. Manufacturing, in contrast, has generally followed an inverse-U-shaped trajectory, expanding after the Civil War through the mid-20th century and declining since. The one disruption to this pattern was the New Deal era, when unprecedented public investments in manufacturing expanded the share of Americans working in the sector, as shown in Figure 1b. While the manufacturing employment share has been in a steady decline in the decades since, it is still far larger than agricultural employment.

Figure 1a

Figure 1b

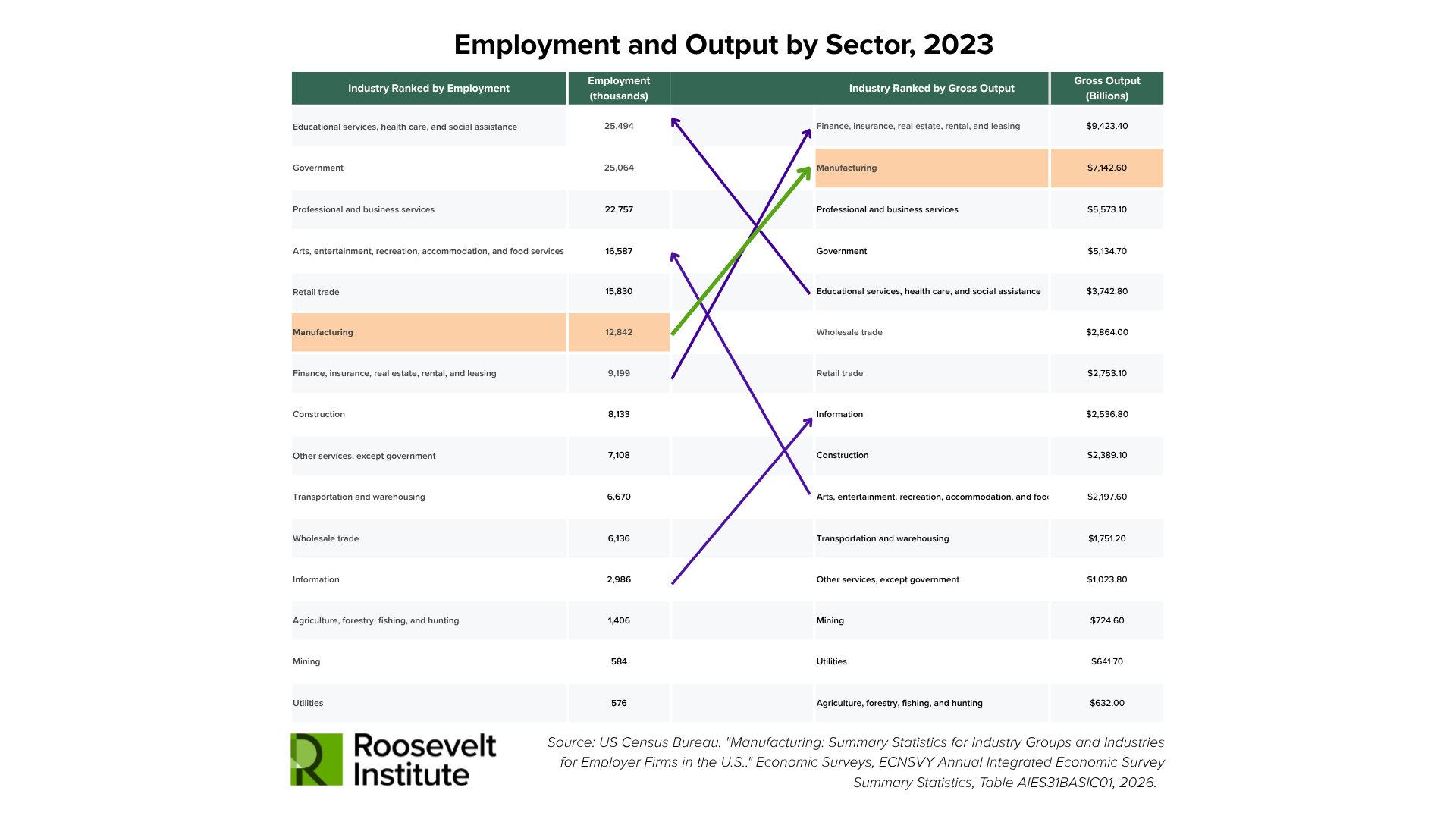

The “services” category aggregates a lot of distinct activities. Federal statistical agencies use the North American Industrial Classification System (NAICS) to sort sectors and industries at two-, three-, four-, five-, and six-digit levels of aggregation.23 At the two-digit level (the highest level of aggregation), there are 20 sectors, including one each for manufacturing, agriculture, and mining; the remaining 17 sectors comprise services.24 Table 1 shows the relative importance of each sector in employment and gross output terms. As can be seen on the leftmost columns, manufacturing is the sixth most important group overall, and the fifth most important private one. This is a significant change since 1979, when more workers worked in manufacturing (23.4 percent) than either the public sector (17.8 percent) or any other private industry.25 Looking at employment measures alone, however, understates the economic importance of manufacturing. The rightmost columns compare the relative positions of economic sectors by gross output, a measure of the total sales or revenue received by an industry. In gross output terms, manufacturing ranks second, behind only finance. The arrows indicate those sectors that jump the most in ranking when comparing their importance for employment versus their gross output. (The appendix features a similar graphic (Table A-1) with value added, a separate measure of economic activity.)

Table 1

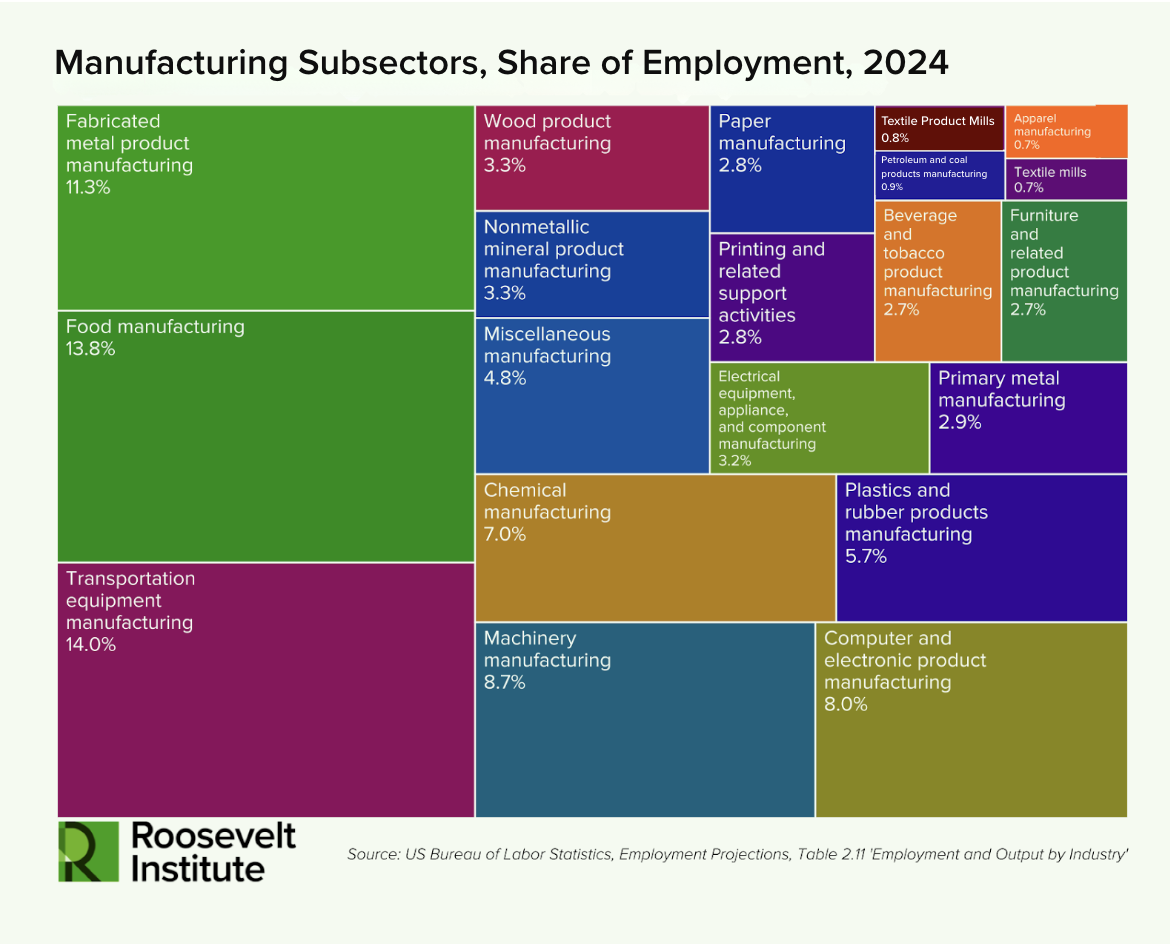

Let’s look further below the hood of the manufacturing sector. The NAICS data show that not all manufacturing matters equally in output and employment terms. Figure 2 breaks up the manufacturing sector into its 21 two-digit subsectors, from food manufacturing (code 311) to furniture and related products manufacturing (code 337). Transportation equipment (including auto, aerospace, boat, tank, and bicycle manufacturing) is the single largest manufacturing subsector, followed by food manufacturing and fabricated metal products.

Figure 2

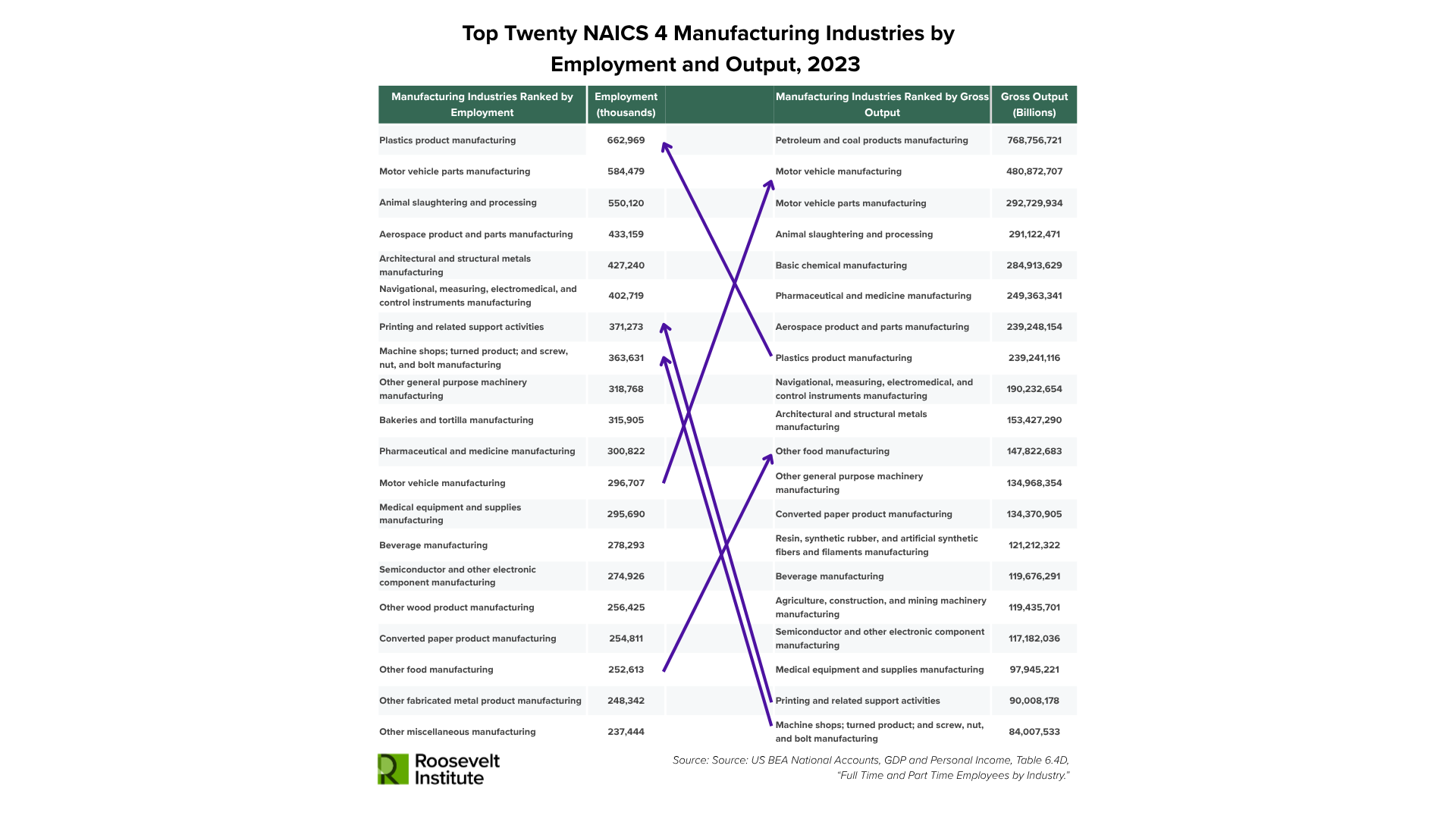

NAICS divides industries up still further, from the 21 manufacturing subsectors to 86 sub-subsectors, to 176 sub-sub-subsectors, to the full list of 346 manufacturing industries, ranging from dog- and cat-food manufacturing (code 311111) to burial casket manufacturing (code 339995). Table 2 lists the top 20 manufacturing sub-sub-subsectors for both output and jobs. Note that in employment terms, plastics, motor vehicle parts, and animal slaughtering and processing are the most important. In terms of gross output, petroleum and coal products and motor vehicle manufacturing are at the top, reflecting in part the high value of intermediate inputs in these industries. As can be seen in value-added terms in the appendix, pharmaceutical and medicine ranks at the top of the list, while petroleum and coal products come second—still high in the ranking but with a significant drop in dollar terms from their gross value.

Table 2

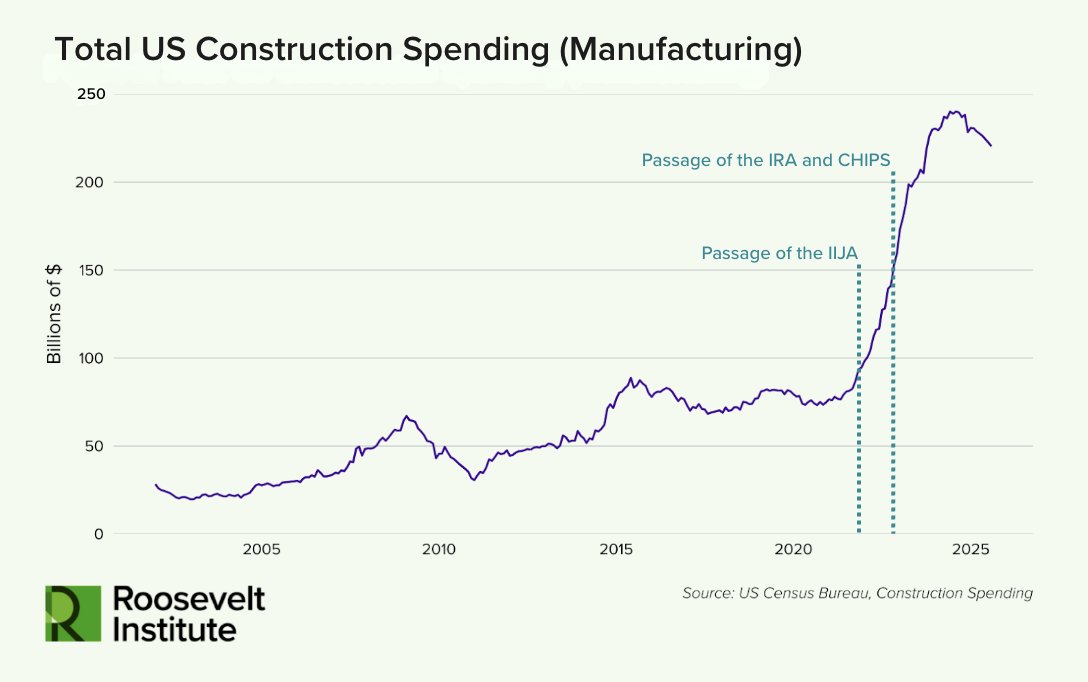

By some indicators, manufacturing had some of its best years over 2021 to 2024. Annual spending on the construction of manufacturing facilities increased nearly threefold between 2021 and the end of 2024, as shown in Figure 3. As explored in more detail in another recent Roosevelt Institute report, this increase was driven by federal incentives under the Biden administration, including the Inflation Reduction Act and the CHIPS and Science Act.26 However, this construction has not yet resulted in major new numbers for manufacturing employment, as factories must be constructed before they can start employing people and churning out products.27

Figure 3

Discussion: Five Reasons to Be Bullish on US Manufacturing

Despite the challenges the sector faces, there are reasons to believe manufacturing will continue to matter.

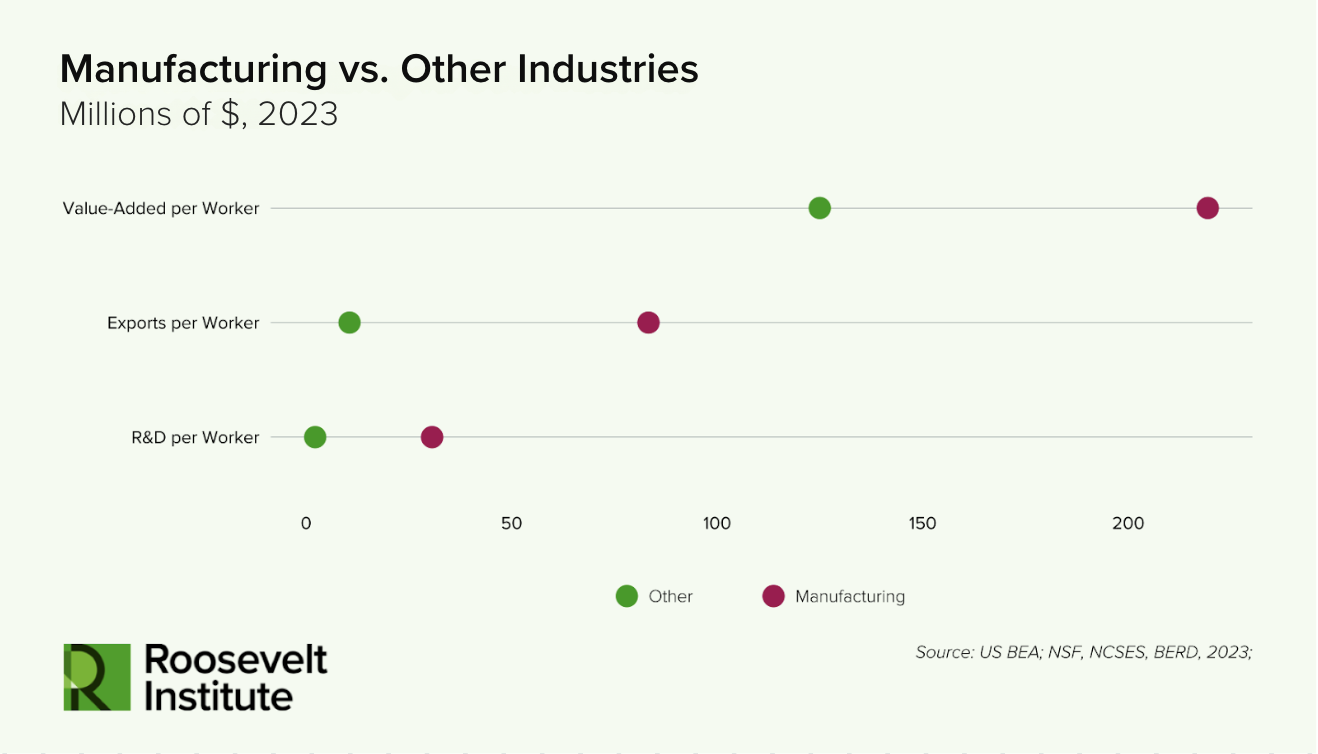

First, manufacturing continues to punch above its weight. While 9 in 10 workers in the economy work in services, manufacturing contributes more on a per-job basis to value added (76 percent greater), exports (688 percent greater), and R&D spending (1,288 percent greater). These statistics are shown in Figure 4, which summarizes the findings of Section 3.

Figure 4

Second, past and current US national security and economic security strategy relies on and supports the domestic manufacturing base, and vice versa.

Key manufacturing industries like steel, shipbuilding, and semiconductors emerged as a result of demand by government for national defense purposes: Military planners have an initial demand for warfighting or technological capacities, which functions as a type of infant industry policy. New firms emerge to supply that demand, which can over time either stay close to the military as part of what President Dwight D. Eisenhower called the military-industrial complex, or increasingly see their interests in supplying their goods to private markets. Often, military planners themselves are keen on having robust private markets for the goods they demand, so as to ensure that the firms they rely on for defense purposes remain profitable and that capabilities remain onshore. If domestic factories exist and are run by owners that are willing (or able to be coerced), these facilities can be repurposed into meeting national needs, whether that is car companies making tanks for the Roosevelt administration during World War II, or textile companies converting to making PPE during the COVID-19 crisis.28

This intertwining between public/defense and private/profit is reflected in national law. For instance, the Trade Expansion Act of 1962 allows trade restrictions to be instituted to protect domestic industries vital for national security—even when they’re not currently being used for national defense. It instructs the president to:

in the light of the requirements of national security and without excluding other relevant factors, give consideration to domestic production needed for projected national defense requirements, the capacity of domestic industries to meet such requirements, existing and anticipated availabilities of the human resources, products, raw materials, and other supplies and services essential to the national defense, the requirements of growth of such industries and such supplies and services including the investment, exploration, and development necessary to assure such growth, and the importation of goods in terms of their quantities, availabilities, character, and use as those affect such industries and the capacity of the United States to meet national security requirements. [He] shall further recognize the close relation of the economic welfare of the Nation to our national security, and shall take into consideration the impact of foreign competition on the economic welfare of individual domestic industries; and any substantial unemployment, decrease in revenues of government, loss of skills or investment, or other serious effects resulting from the displacement of any domestic products by excessive imports shall be considered, without excluding other factors, in determining whether such weakening of our internal economy may impair the national security.29 (emphasis added)

A similarly expansive definition of “national defense” is included in the Defense Production Act, which in addition to tending to immediate defense needs, also instructs the executive branch to maximize the domestic supply of conventional and renewable energy—for both defense and civilian purposes.30

And yet, the defense industrial base has faced several notable changes during the neoliberal period. The US defense industrial base has lost 40 percent of its small-business suppliers in recent decades, following the so-called “Last Supper” during the Clinton administration, where the Secretary of Defense called on military contractors to contract and consolidate—mirroring concentration patterns in the private sector.31 Employment levels have also declined among defense contractors, tracking trends in the rest of manufacturing. Unionization rates used to actually be higher in defense contractors than in manufacturing overall, but are now lower at some major contractors than manufacturing as a whole.32 A Biden administration supply chain report by the Defense Department bemoaned that 86 percent of manufacturers surveyed by the military earn less than 10 percent of their profits from defense purposes, while private capital wants higher and quicker returns than US manufacturing provides today—leading to further offshoring risk.33

Adding are the challenges now posed by what historian Daniel Immerwahr has called Trump’s regime change nihilism.34 The US and Israel’s unprovoked attack on Iran has led to an apparently unplanned-for escalation that has led to the latter’s closure of the Strait of Hormuz. This has now strained a key global chokepoint for all sorts of manufactured, mined, and agricultural products, including aluminum, urea, and potash. The US has limited domestic capacity to produce these products, but they are increasingly the focus of industrial policy planning.35 The rapid depletion of munition stocks—mirroring a similar depletion during Russia’s war on Ukraine—is leading some military analysts to raise concern that US military capacity would be strained moving forward, particularly in the event of a US-China war for dominance in the Asia-Pacific region.36 If such a war were to take place, it is estimated that it would cost over $10 trillion in damages to the global economy, eclipsing the cost of the 2009 financial crisis and COVID-19 and leading to interruptions to half of the global container fleet for goods trade.37 This in turn comes on top of growing concern over disparities in production levels of all manner of military and nonmilitary production between the US and China, including a 230-1 disparity in shipbuilding capacity.38

While it is beyond the scope of this report to resolve these thorny geopolitical questions, it’s clear that against this backdrop, policymakers are pouring money into the defense industrial base: Currently, this administration is pushing for a 40 percent increase in the defense budget for FY 2027,39 a dramatic acceleration of an already upward trend in federal military spending.40 The enacted defense budget for FY 2026 was more than $1 trillion.41 Between 2020 and 2024, private-sector defense spending surged by an estimated $440 billion,42 and the 2026 National Defense Authorization Act aims to plow tens of billions into domestic shipbuilding, munitions manufacturing, and other defense industrial base projects.43 In April 2026, a large bipartisan, bicameral, labor-management coalition was announced to launch a full-scale industrial policy to rebuild US shipbuilding.44 While debates rage about whether such spending levels reflect the correct national priorities,45 it is clear that US policymakers are increasingly putting skin in the game of preserving US manufacturing for defense purposes.

Third, addressing the climate crisis means moving toward primarily manufactured (rather than primarily mined) energy.The United Nations estimates that countries globally need to be spending $4–6 trillion a year to mitigate and adapt to climate change.46 By some estimates, China is producing the majority of current world demand for clean energy.47 However, ceding production in this market to China would carry several risks. First, that degree of reliance on a single source would entail a level of monopolization far in excess of OPEC’s over the petroleum market—close to 100 percent in a single country for some subsectors for the former, compared to around 40 percent spread across a dozen countries in the latter.48 To be sure, the mechanics of clean energy versus fossil fuels are different: An existing stock of solar panels can continue to function even if US–China trade is cut off for a period of time, while an oil embargo can bring the economy to a halt. Nonetheless, China is already showing that it can weaponize its stock and pricing power over clean-energy minerals to create major shockwaves in the global economy.49 These actions confirm the desirability of a de-monopolization strategy with distributed energy production around the world.

Moreover, the economics of clean energy will eventually become irresistibly preferable over fossil fuel production. By some measures, renewables are already the cheapest form of energy—with solar and onshore wind undercutting fossil fuels by 41 and 53 percent, respectively.50 Countries and companies are racing to make other forms of clean energy cost-competitive. The US’s unprovoked war in Iran has led to oil prices spiking, but countries that use more clean energy have been relatively spared. This will push more countries to expand clean energy consumption.51 Thus, even as the US backtracks on climate action under the Trump administration, the world will not. According to some estimates, by the 2030s, relatively high-cost fossil fuel producers like the US and Canada will be priced out of global energy markets, while relatively low-cost fossil fuel producers like OPEC will expand their share of the remaining demand for fossil fuels. Even if the US were to maintain or expand fossil fuel consumption at home (as Trump appears to want to do), it would not make up for the decline in export revenues. US fossil fuel revenues could drop by 40 percent, and exports by 65 percent.52 This could lead to an unplanned and unmanaged transition out of fossil fuels, putting key US jobs and regions at risk.

It would be far preferable to get out ahead of that juncture and plan for clean energy manufacturing and service-sector jobs better than policymakers handled the opening to global markets over the neoliberal period. Indeed, for manufacturers, this transition holds a lot of promise. According to the UN Industrial Development Organization, manufacturing generates the majority of “green patents” globally.53 What would planning a transition require? As research for the French government has shown, reaching net zero by 2050 will require that 80 percent of total energy supply be provided by nuclear, hydropower, solar, wind, and other renewables—which for many countries will involve investments of over 2 percent of GDP per year. Clean energy requires a lot of machines and a lot of factories, with high up-front capital costs but eventually lower operating costs than fossil fuels. This study also estimated the number of electric vehicles, heat pumps, and other products that will need to be brought online to meet intermediate climate targets.54

This complements the work of the “Draghi report”—named for its author, Mario Draghi, the former European Central Bank chief and Italian prime minister—which categorizes industries into four cases: where Europe cannot catch up, where Europe could catch up, where Europe should try to maintain a technology and production edge, and where Europe should maintain a production (but not technology) edge.55 Having quantitative targets in mind for each industrial sector allows national, subnational, and private leaders to make plans for what production will happen where. After 2029, US policymakers will need to learn from these planning experiences,56 and ensure that their investments are visible, durable, and executed as speedily as possible.57

Fourth, changes in technology may make manufacturing work relatively more attractive. Innovations like advanced or “additive manufacturing,” also called 3D printing, are intended not necessarily to replace workers but to tailor production to meet customer-specific needs. 3D printers can be used, for instance, to create a customized prosthetic limb for an amputee within hours of diagnosis.58 In a first step, workers create a digital model of the desired product, and then supervise as the “printer” creates a series of very thin layers of plastic, textiles, steel, or other materials until the product is fully formed—typically without the need for molds or final assembly. They can be entered directly into markets without the need to retain excess inventories. An increase of 1 percent in the additive manufacturing patent stock (a proxy for the spread of the process) actually increases the demand for labor by 0.065 percent—rather than displacing labor as historical technology changes did. By saving on capital costs, 3D printing reduces the scale of operations needed and the importance of international wage disparities, leading to possibilities to reshore work and distribute it around the country.59

Another study found that while traditional manufacturing divides labor tasks into “high-skilled” work that requires high levels of training and discretion, and “low-skilled” work that is routine (and thus automatable and low pay), additive manufacturing converts the would-be assembly line workers into designers and experimenters, executing more nonroutine, bespoke tasks. While “high-skilled” engineers also gain skills relative to traditional manufacturing, the relative upskilling effect is highest for the previously “low-skilled” operators.60

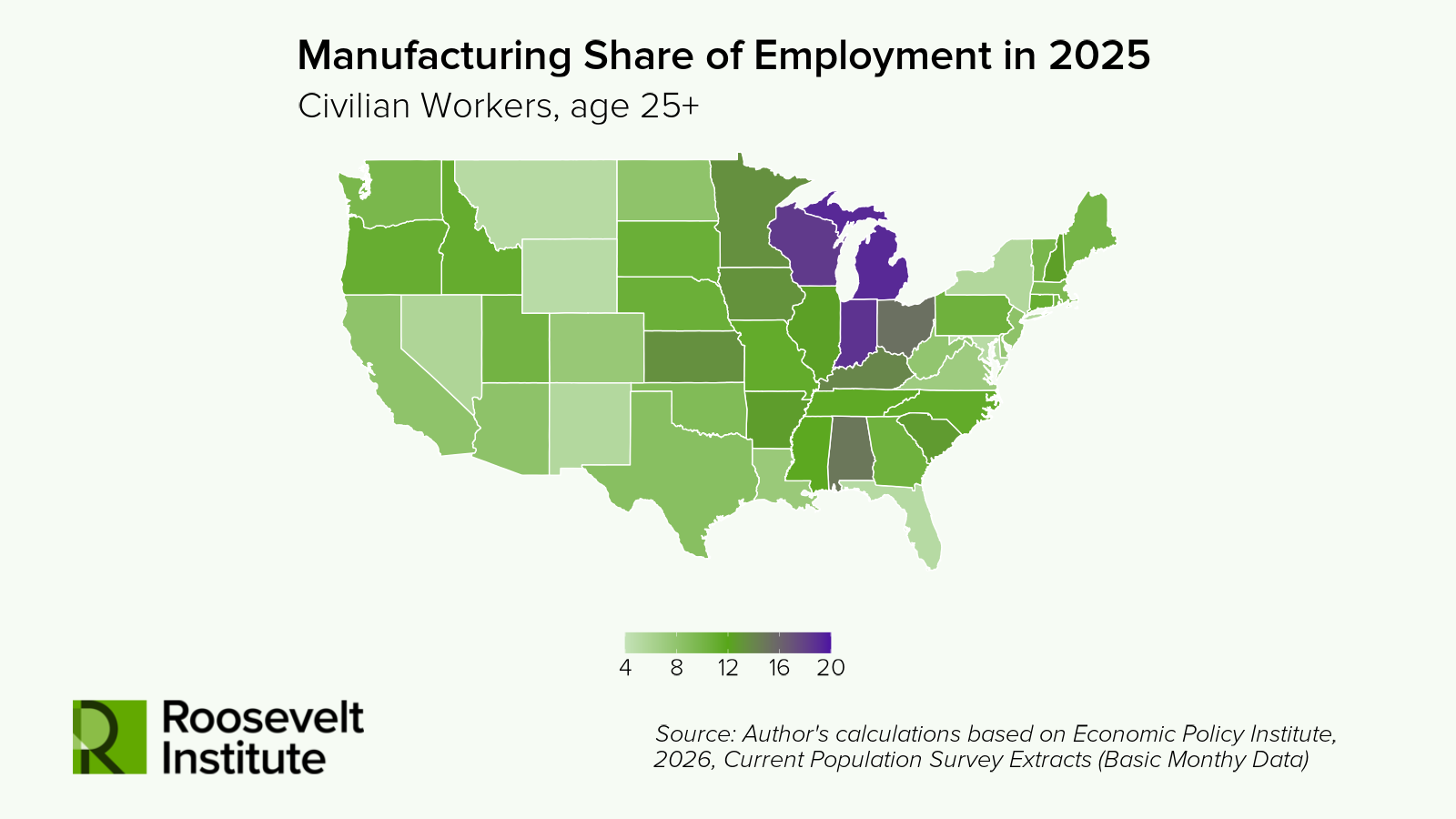

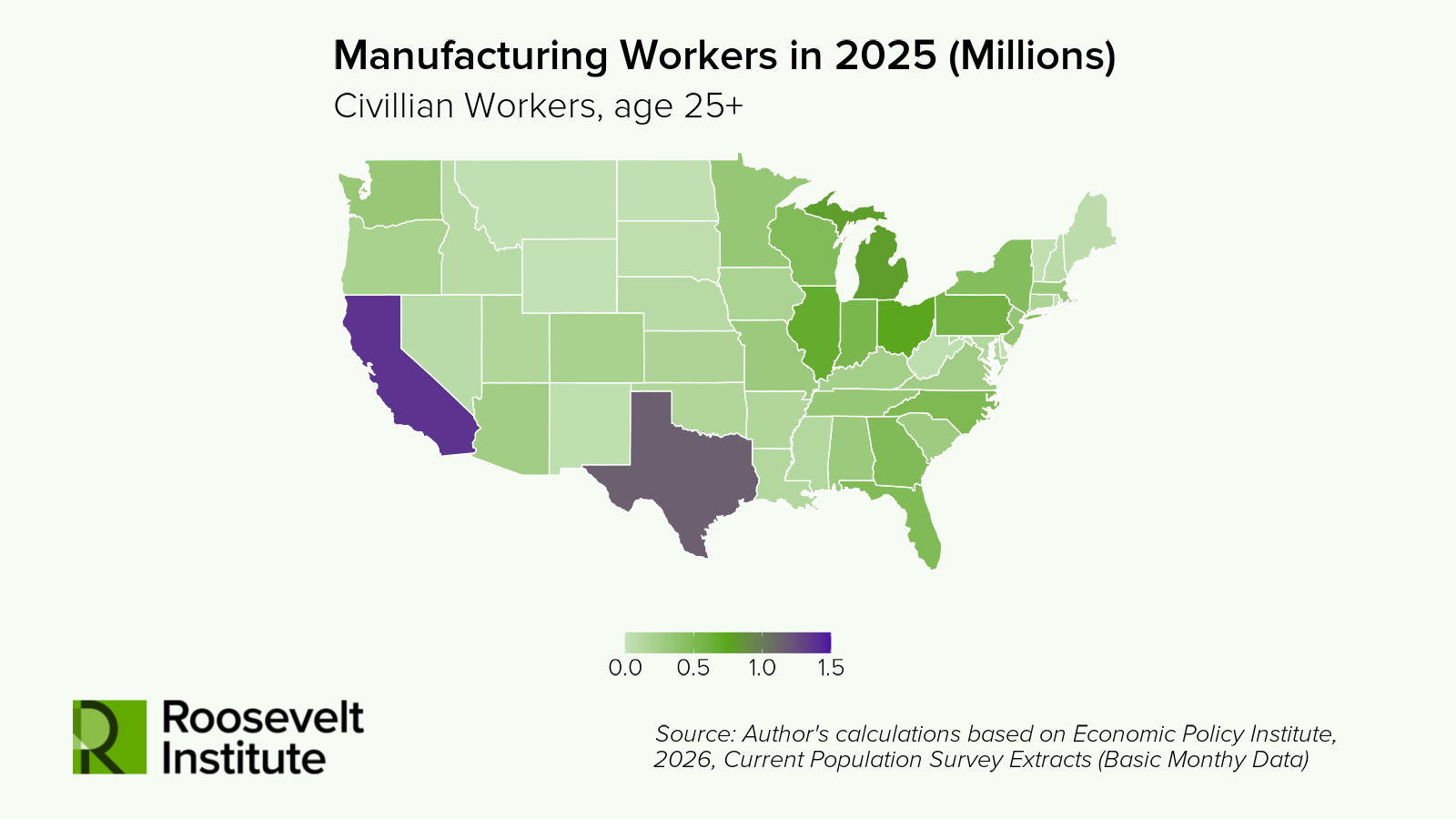

Finally, even as manufacturing employment declines overall, there are some areas where the sector remains important in employment terms. As Figure 5a shows, several states, including Michigan, Wisconsin, and Ohio, have more than 10 percent of their workers in manufacturing. While these states have long been associated with their manufacturing sectors, Figure 5b shows that in numeric terms, California and Texas are actually the nation’s leading industrial centers. If manufacturing continues to matter to places (especially such politically relevant ones), it will continue to matter for policy.

Figure 5a

Figure 5b

Footnotes

- US Bureau of Labor Statistics, “Employment by Major Industry Sector,” last modified August 28, 2025, https://www.bls.gov/emp/tables/employment-by-major-industry-sector.htm; The Story of U.S. Agricultural Estimates (US Department of Agriculture, 1969), https://nass.usda.gov/About_NASS/pdf/The%20Story%20of%20U.S.%20Agricultural%20Estimates.pdf, 1. ↩︎

- US Bureau of Labor Statistics, “Employment by Major Industry Sector.” ↩︎

- Federal Reserve Bank of St. Louis, “All Employees, Manufacturing,” April 3, 2026, https://fred.stlouisfed.org/graph/?g=1TqEq. ↩︎

- Federal Reserve Bank of St. Louis, “Population, Total for United States,” July 2, 2025, https://fred.stlouisfed.org/series/POPTOTUSA647NWDB. ↩︎

- Tomasz M. Płudowski and Kim Mee Chong, “Campaign Rhetoric vs. Economic Reality: Analyzing Job Outsourcing and Reshoring Narratives in Donald Trump’s 2016–2024 Campaigns,” Contemporary Economics 19, no. 4 (2025): 464, https://doi.org/10.5709/ce.1897-9254.578. ↩︎

- The remaining 0.2 percent is accounted for by mining. US Bureau of Labor Statistics, “Employment by Major Industry Sector.” ↩︎

- Eric Levitz, “Trump’s Tariff and Trade War Is a Doomed Quest Fueled by Nostalgia,” Vox, August 7, 2025, https://vox.com/politics/407025/trump-tariffs-reciprocal-trade-war-why-explanation-nostalgia. ↩︎

- Dylan Matthews, “Chinese Electric Cars: Why Biden Is Keeping Cheap Cars from BYD Out,” Vox, April 3, 2024, https://vox.com/climate/2024/3/4/24087919/biden-tariff-chinese-ev-byd-battery-detroit. ↩︎

- Constance Grady, “The Incels Supporting Trump’s Tariffs, Explained,” Vox, April 14, 2025, https://vox.com/culture/408578/trump-tariffs-incels-misogyny-email-jobs. This comes after decades of similar comments, such as when Nike CEO Phil Knight once quipped that Americans don’t want to make shoes, or when Barack Obama’s chief economist, Christina Romer, faulted views that see producing “real things” as important. See Christina D. Romer, “Do Manufacturers Need Special Treatment?,” Business, New York Times, February 4, 2012, https://nytimes.com/2012/02/05/business/do-manufacturers-need-special-treatment-economic-view.html. ↩︎

- Milo Yiannopoulos (@Nero), “Men are depressed and addicted and broken because they have nothing to do,” X, April 4, 2025, https://x.com/Nero/status/1908287716690977084. ↩︎

- Howard Lutnick, “Transcript: Commerce Secretary Howard Lutnick,” interview by Margaret Brennan, Face the Nation with Margaret Brennan, CBS News, April 6, 2025, https://www.cbsnews.com/news/transcript-commerce-secretary-howard-lutnick-on-face-the-nation-with-margaret-brennan-april-6-2025/. ↩︎

- In Trump’s second administration, the target now seems to be 16 percent. By either target, they are moving in the wrong direction: Over Trump’s first term, the share of workers in manufacturing declined from 8.5 percent in 2016 to 8.3 percent in 2020. From the start of Trump’s second term to the most recent numbers available, the number of workers has decreased by 100,000, from 8 percent to 7.9 percent. These are the lowest numbers since the US industrialized in the 19th century. See Matthew J. Belvedere, “Trump’s Point Man on Trade: ‘We Envision a More Germany-Style Economy,’” CNBC, January 25, 2017, http://cnbc.com/2017/01/25/trumps-point-man-on-trade-we-envision-a-more-germany-style-economy.html; Doug Palmer, “Navarro Says Manufacturing Job Gains Will Take Time,” Politico PRO, October 17, 2025, https://subscriber.politicopro.com/article/2025/10/navarro-says-manufacturing-job-gains-will-take-time-00613730. ↩︎

- This mirrored the president’s main talking point on climate: Joe Biden (@JoeBiden), “When I hear ‘climate,’ I think jobs. Good-paying, high-quality jobs that will help speed our transition to a green economy of the future and unleash sustainable growth,” X, June 15, 2022, https://x.com/joebiden/status/1537150703633850371. See “Biden-Harris Administration Celebrates Two Years of the Inflation Reduction Act,” August 17, 2024 https://www.presidency.ucsb.edu/documents/what-they-are-saying-biden-harris-administration-celebrates-two-years-the-inflation. ↩︎

- “THE 1992 CAMPAIGN; Transcript of 2d TV Debate Between Bush, Clinton and Perot,” U.S., The New York Times, October 16, 1992, https://www.nytimes.com/1992/10/16/us/the-1992-campaign-transcript-of-2d-tv-debate-between-bush-clinton-and-perot.html. ↩︎

- Jared Golden, Golden Introduces Bill to Restore American Manufacturing with 10 Percent Tariff on All Imports (U.S. House of Representatives Maine-02, 2024), http://golden.house.gov/media/press-releases/golden-introduces-bill-to-restore-american-manufacturing-with-10-percent-tariff-on-all-imports. ↩︎

- Earlier interventions on this question include Stephen S. Cohen and John Zysman, Manufacturing Matters: The Myth of the Post-Industrial Economy (Basic Books, 1988); Adam Hersh and Christian E. Weller, “Does Manufacturing Matter?,” Challenge 46, no. 2 (2003): 59–79, https://doi.org/10.1080/05775132.2003.11034193; Susan Helper et al., Why Does Manufacturing Matter? Which Manufacturing Matters? A Policy Framework (Brookings Institution, 2012), https://www.brookings.edu/articles/why-does-manufacturing-matter-which-manufacturing-matters/; Antonio Andreoni and Mike Gregory, “Why and How Does Manufacturing Still Matter: Old Rationales, New Realities,” Revue d’économie Industrielle, no. 144 (December 2013): 21–57, https://doi.org/10.4000/rei.5668; Jostein Hauge and Ha-Joon Chang, “The Role of Manufacturing versus Services in Economic Development,” in Transforming Industrial Policy for the Digital Age, ed. Patrizio Bianchi et al. (Edward Elgar Publishing, 2019), https://elgaronline.com/edcollchap/edcoll/9781788976145/9781788976145.00007.xml. ↩︎

- Ana Margarida Fernandes and Tristan Reed, Industrial Policy for Development: Approaches in the 21st Century, Policy Research Reports (World Bank, 2026), https://openknowledge.worldbank.org/entities/publication/9f8098d5-fa1f-4c1b-97b5-f04262818bb3. ↩︎

- Todd N. Tucker, Industrial Policy and Planning: What It Is and How to Do It Better (Roosevelt Institute, 2019), https://rooseveltinstitute.org/industrial-policy-and-planning/. ↩︎

- Todd N. Tucker, Everything Is Climate Now: New Directions for Industrial Policy from Biden’s Supply Chain Reports (Roosevelt Institute, 2022), https://rooseveltinstitute.org/publications/reading-bidens-supply-chain-reports. ↩︎

- Todd N. Tucker et al., Industrial Policy 2025: Bringing the State Back In (Again) (Roosevelt Institute, 2024), https://rooseveltinstitute.org/publications/industrial-policy-2025. ↩︎

- Tim Minshall, How Things Are Made: A Journey Through the Hidden World of Manufacturing (Ecco, 2025): 64–65. ↩︎

- Some analysts vary these groupings slightly. Classical economists like Adam Smith paired agriculture with mining, fisheries, furs, and other activities that extract from the land in a category called “rude produce.” See Adam Smith, An Inquiry into the Nature and Causes of the Wealth of Nations (W. Strahan and T. Cadell, 1776). The UN Industrial Development Organization, for its part, breaks the economy into five sectors: agriculture, manufacturing, nonmanufacturing industry (mining, utilities, and construction), modern services (transport, communication, finance, and business services), and other services. See Industrial Development Report 2024: The New Era of Industrial Policy (UN Industrial Development Organization, 2024): 38, https://unido.org/sites/default/files/unido-publications/2024-06/Industrial%20Development%20Report%202024.pdf. ↩︎

- US Census Bureau, “North American Industry Classification System: Introduction to NAICS,” last accessed April 11, 2026, https://www.census.gov/naics/?58967?yearbck=2022. ↩︎

- While there are 20 sectors, there are 24 two-digit NAICS codes: Manufacturing gets three NAICS two-digit codes (31, 32, and 33), and retail trade and transportation/warehousing each get two. ↩︎

- “Other services” was the second highest, at 19.1 percent. See Lois M. Plunkert, “The 1980’s: A Decade of Job Growth and Industry Shifts,” Monthly Labor Review (Bureau of Labor Statistics, September 1990), https://bls.gov/opub/mlr/1990/09/art1full.pdf. ↩︎

- See Betony Jones and Joe Peck, “The Receipts: The Untold and Underappreciated Outcomes of Biden’s Clean Energy Strategy,” Roosevelt Institute, 2026 https://rooseveltinstitute.org/publications/the-receipts-the-untold-and-underappreciated-outcomes-of-bidens-clean-energy-strategy/ ; Skanda Amarnath, “Did the CHIPS Act Trigger the Manufacturing Construction Boom?,” Factory Settings, March 9, 2026, https://factorysettings.org/p/did-the-chips-act-trigger-the-manufacturing. ↩︎

- Though for some positive early indications in semiconductor manufacturing and associated employment, see Bilge Erten et al., “Employment Impacts of the CHIPS Act,” Working Paper 34625 (National Bureau of Economic Research, January 2026), https://www.nber.org/papers/w34625. ↩︎

- The literature on these dynamics is extensive. For useful starting points, see Paul A. C. Koistinen, Beating Plowshares Into Swords: The Political Economy of American Warfare, 1606-1865 (University Press of Kansas, 1996) (and its four follow-up volumes); Linda Weiss, America Inc.?: Innovation and Enterprise in the National Security State (Cornell University Press, 2014); Mark R. Wilson, Destructive Creation: American Business and the Winning of World War II (University of Pennsylvania Press, 2016); Thomas Heinrich, Warship Builders: An Industrial History of U.S. Naval Shipbuilding, 1922-1945 (Naval Institute Press, 2020); Rana Foroohar, Homecoming: The Path to Prosperity in a Post-Global World (Crown, 2022). ↩︎

- 19 U.S. Code § 1862(d). For an application of this authority to the green steel industry, see Todd N. Tucker and Timothy Meyer, A Green Steel Deal: Toward Pro-Jobs, Pro-Climate Transatlantic Cooperation on Carbon Border Measures, Working Paper (Roosevelt Institute, 2021), https://rooseveltinstitute.org/publications/a-green-steel-deal-towards-pro-jobs-pro-climate-trans-atlantic-cooperation-on-carbon-border-measure/. ↩︎

- See Joel Dodge and Todd N. Tucker, Trump Wields Defense Production Act to Promote Fossil Fuels. It Could Instead Be Used to Promote All-of-the-Above Energy Abundance. (Roosevelt Institute, 2026), https://rooseveltinstitute.org/publications/trump-wields-defense-production-act-to-promote-fossil-fuels/. ↩︎

- Farooq Mitha, “Small Businesses Are Key to National Defense,” The Hill, February 7, 2023, https://thehill.com/opinion/congress-blog/3847967-small-businesses-are-key-to-national-defense; Jonathan Chang and Meghna Chakrabarti, “The Last Supper”: How a 1993 Pentagon Dinner Reshaped the Defense Industry, (Boston), March 1, 2023, https://www.wbur.org/onpoint/2023/03/01/the-last-supper-how-a-1993-pentagon-dinner-reshaped-the-defense-industry. . ↩︎

- Taylor Barnes, Labor of the US Military-Industrial Complex (Transition Security Project, 2026), https://transitionsecurity.org/labor-of-the-us-military-industrial-complex/. ↩︎

- DOD, Securing Defense-Critical Supply Chains (Department of Defense, 2022), https://media.defense.gov/2022/feb/24/2002944158/-1/-1/1/dod-eo-14017-report-securing-defense-critical-supply-chains.pdf, at 62. ↩︎

- Daniel Immerwahr, “What’s Behind Trump’s New World Disorder?,” Annals of War, The New Yorker, March 16, 2026, https://www.newyorker.com/magazine/2026/03/23/whats-behind-trumps-new-world-disorder. ↩︎

- Joana Colussi and Michael Langemeier, “Middle East Conflict Revives Concerns Over Fertilizer Dependence in the U.S. and Brazil,” Farmdoc Daily 16, no. 68 (2026), https://farmdocdaily.illinois.edu/2026/04/middle-east-conflict-revives-concerns-over-fertilizer-dependence-in-the-u-s-and-brazil.html; Kailyn Rhone, “It’s Not Just Oil. The Iran War Is Disrupting Many Essential Goods.,” Business, the New York Times, March 10, 2026, https://www.nytimes.com/2026/03/10/business/iran-war-impact-helium-urea-sulfur.html; Ryan Dezember, “How Oklahoma Landed America’s First Aluminum Smelter in Half a Century,” Business, Wall Street Journal, April 12, 2026, https://www.wsj.com/business/how-oklahoma-landed-americas-first-aluminum-smelter-in-half-a-century-e00c83d3. ↩︎

- Seth G. Jones, Empty Bins in a Wartime Environment: The Challenge to the U.S. Defense Industrial Base (Center for Strategic and International Studies, 2023), https://csis.org/analysis/empty-bins-wartime-environment-challenge-us-defense-industrial-base; Eric Schmitt and Jonathan Swan,” Iran War Has Drained U.S. Supplies of Critical, Costly Weapons,“ The New York Times, April 23, 2026. https://www.nytimes.com/2026/04/23/us/politics/iran-war-cost-military.html; Grant Newsham, “Does Iran War Make a China Attack on Taiwan More Likely?,” Asia Times, March 5, 2026, https://asiatimes.com/2026/03/iran-war-make-a-china-attack-on-taiwan-more-likely/. ↩︎

- Jennifer Welch and Maeva Cousin, “The $10 Trillion Fight: Modeling a US-China War Over Taiwan,” Bloomberg, February 10, 2026, https://www.bloomberg.com/news/articles/2026-02-10/the-10-trillion-fight-modeling-a-us-china-war-over-taiwan. ↩︎

- Seth G. Jones and Alexander Palmer, China Outpacing U.S. Defense Industrial Base (Center for Strategic and International Studies, 2024), https://csis.org/analysis/china-outpacing-us-defense-industrial-bas; ↩︎

- Tony Romm, “White House Seeks $1.5 Trillion for Defense in New Budget Request,” New York Times, April 3, 2026, https://www.nytimes.com/2026/04/03/us/politics/white-house-defense-budget.html. ↩︎

- US Bureau of Economic Analysis, Federal Government: National Defense Consumption Expenditures and Gross Investment [FDEFX], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FDEFX, April 27, 2026. ↩︎

- US Department of War, FY 2027 Budget Request Overview Book, p. 8, https://comptroller.war.gov/Portals/45/Documents/defbudget/FY2027/FY2027_Budget_Request_Overview_Book.pdf#page=8 ↩︎

- Sam Moyer, Mobilizing Private Capital for Defense (NDIA Emerging Technologies Institute, 2026), https://emergingtechnologiesinstitute.org/-/media/ndia-eti/reports/mobilizing-capital-for-defense/mobilizingcapitalreport_2026_final.pdf?download=1. ↩︎

- Nathan Owens, “What Trump’s $901B Defense Law Means for Manufacturing,” Manufacturing Dive, December 19, 2025, https://manufacturingdive.com/news/trumps-901b-defense-law-manufacturing-shipbuilding-CRMN-DIB/808443. ↩︎

- Mike Schuler, “‘We Need to Get This Done’: Lawmakers, Labor and Industry Renew Push for SHIPS for America Act,” gCaptain, April 23, 2026, https://gcaptain.com/we-need-to-get-this-done-lawmakers-labor-and-industry-renew-push-for-ships-for-america-act/. ↩︎

- See e.g. Oliver Milman, “Cost of the War in Iran Is Outweighing the Budget of Several Government Agencies in the US,” The Guardian, March 18, 2026, https://www.theguardian.com/us-news/2026/mar/18/us-spending-iran-war-priorities . ↩︎

- UNFCCC, Sharm El-Sheikh Implementation Plan (United Nations Climate Change, 2022), https://unfccc.int/documents/624444. ↩︎

- Brad Setser, Will China Take Over the Global Auto Industry? (Council on Foreign Relations, 2024), https://cfr.org/articles/will-china-take-over-global-auto-industry; Brad Setser, China’s Massive Surplus Is Everywhere (Yet The IMF Still Has Trouble Seeing It Clearly) (Council on Foreign Relations, 2025), https://cfr.org/articles/chinas-massive-surplus-everywhere-yet-imf-still-has-trouble-seeing-it-clearly. ↩︎

- US Energy Information and Analysis, “What Drives Crude Oil Prices: Supply OPEC,” https://www.eia.gov/finance/markets/crudeoil/supply-opec.php. ↩︎

- Trevor Sutton and Evelyne Williams, How China’s New Trade Assertiveness Is Linked to Its Clean Energy Dominance (Center on Global Energy Policy at Columbia University, 2025), https://energypolicy.columbia.edu/how-chinas-new-trade-assertiveness-is-linked-to-its-clean-energy-dominance. ↩︎

- 91% of New Renewable Projects Now Cheaper Than Fossil Fuels Alternatives (International Renewable Energy Agency, 2025), https://www.irena.org/News/pressreleases/2025/Jul/91-Percent-of-New-Renewable-Projects-Now-Cheaper-Than-Fossil-Fuels-Alternatives. But, see Brett Christophers, The Price Is Wrong (Verso, 2024). ↩︎

- Dharna Noor, “What Does the Iran War Mean for Clean Energy Transition?,” Environment, The Guardian, March 26, 2026, https://theguardian.com/environment/2026/mar/26/iran-war-clean-energy-transition. ↩︎

- Jean-Francois Mercure et al., “Reframing Incentives for Climate Policy Action,” Nature Energy 6, no. 12 (2021): 1133–43, https://doi.org/10.1038/s41560-021-00934-2. ↩︎

- Alejandro Lavopa and Maria de las Mercedes Menendez, Who Is At the Forefront of the Green Technology Frontier? Again, It’s the Manufacturing Sector, Policy Brief Series, Insights on Industrial Development (UN Industrial Development Organization, 2023), https://unido.org/sites/default/files/unido-publications/2023-10/IID%20Policy%20Brief%206.pdf. ↩︎

- Jean Pisani-Ferry and Selma Mahfouz, The Economic Implications of Climate Action: A Report to the French Prime Minister (France Stratégie, 2023), https://piie.com/sites/default/files/2023-11/2023-11-08-pisani.pdf; Jean Pisani-Ferry, The Transition to Carbon Neutrality: An Unusual Type of Structural Reform (Peterson Institute for International Economics, 2024), https://piie.com/commentary/speeches-papers/2024/transition-carbon-neutrality-unusual-type-structural-reform. ↩︎

- Mario Draghi, The Future of European Competitiveness: A Competitiveness Strategy for Europe (“The Draghi Report”) (European Commission, 2024), https://commission.europa.eu/topics/strengthening-european-competitiveness/eu-competitiveness-looking-ahead_en. ↩︎

- Todd N. Tucker, Building Up in 2029: How To Make Green Statecraft Durable (Roosevelt Institute, forthcoming). ↩︎

- For the importance of the traceability of these efforts, see Alexander F. Gazmararian et al., “Why Biden-Era Clean Energy Investment Policies Had Limited Political Returns,” Proceedings of the National Academy of Sciences 123, no. 9 (2026): e2526802123, https://doi.org/10.1073/pnas.2526802123. ↩︎

- Jacob Williamson-Rea, “Reducing Prosthesis Fitting Time through Additive Manufacturing,” Manufacturing PA Innovation Program, August 16, 2022, https://manufacturingpa.org/news/2022/08/rmu-union-orthotics.html. ↩︎

- Giulia Felice et al., “The Employment Implications of Additive Manufacturing,” Industry and Innovation 29, no. 3 (2022): 333–66, https://doi.org/10.1080/13662716.2021.1967730. ↩︎

- Avner Ben-Ner et al., “Effects of New Technologies on Work: The Case of Additive Manufacturing,” ILR Review 76, no. 2 (2023): 255–89, https://doi.org/10.1177/00197939221134271. For more on the labor impact of advanced manufacturing more broadly, see Susan Helper et al., “Who Profits from Industry 4.0? Theory and Evidence from the Automotive Industry,” SSRN Scholarly Paper no. 3377771 (Social Science Research Network, January 31, 2019), https://doi.org/10.2139/ssrn.3377771; Susan Helper et al., Factories of the Future: Technology, Skills, and Digital Innovation at Large Manufacturing Firms, Research Brief no. 19 (MIT, 2021); John Liu and William B. Bonvillian, “The Technologist,” Issues in Science and Technology, February 5, 2024, https://issues.org/technologist-advanced-manufacturing-workforce-liu-bonvillian. ↩︎

Acknowledgments

The authors would like to thank Ijeoma Ogbonna for stellar work on data visualization, and Katherine De Chant, Hannah Groch-Begley, Julie Hersh, Suzanne Kahn, Mike Madowitz, Stephen Nuñez, Toyosi Odusola, Aastha Uprety, Martin Yim, and Elizabeth Wilkins for their feedback, insights, and contributions to this report. We also benefited from helpful insights from Heather Boushey, Susan Helper, Adam Hersh, Alejandro Lavopa, Lenore Palladino, and John Schmitt. Any errors, omissions, or other inaccuracies are the authors’ alone.

Suggested Citation

Tucker, Todd N. and Oskar Dye-Furstenberg. 2026. Against Manufacturing Doomerism: Why and How Making Stuff Matters. New York: Roosevelt Institute.

May 8, 2026: Figures 7, 8, 17a, and 17b in the report have been updated.

RELATED RESOURCES

Authors

Oskar Dye-Furstenberg

Senior Research AssociateOskar Dye-Furstenberg is a senior research associate at the Roosevelt Institute where he supports think tank staff and fellows in their research.