How Long-Term Care Costs Drain the Middle Class and Deepen Intergenerational Wealth Inequality

April 9, 2026

By Jessica Forden

Key Takeaways

- Growing old in the US is expensive. Median household income for those aged 65+ is approximately $57,000, but nursing home care can cost between $115,000 and $129,000 annually.

- Few Americans have enough savings to cover long-term care costs out-of-pocket. After the onset of care needs, middle-class individuals face permanent wealth reductions to just 42% of their original levels, whereas the top quartile of earners eventually recover 94% of their assets.

- Even among upper-middle-class couples with lifetime earnings over $4.75 million, nearly half will spend down their assets paying for long-term care and eventually enroll in Medicaid if they require long-term care for five years or more.

- Unpaid family care is not without its own intergenerational costs. Unpaid caregivers provided an estimated $600 billion in economic value in 2021, often at the expense of their own career growth and retirement savings.

- The lack of public support turns long-term care from a personal health challenge into a structural component of downward mobility and intergenerational wealth inequality.

Introduction

Headlines claim that millennials are poised to become the wealthiest generation in American history, citing the massive transfer of wealth expected as baby boomers pass on their assets (Morning Brew 2025; Bahney 2024; Shan 2024). But these narratives are misleading. They focus on the fortunes of ultra-wealthy families and obscure a far more pressing and widespread reality. Most Americans—many more than may appreciate it—will have little left to pass onto future generations after depleting assets to pay for long-term care costs.

Over the last two decades, long-term care costs have risen sharply, precisely as the population over 65 in the US has grown at a rapid pace (Miller 2025; “Older Adults” 2025). This stark price hike is not a surprise. Demand for long-term care services is increasing as the US population ages, but the industry has long had problems attracting and retaining workers. Long-term care workers often face low pay and poor working conditions, with 36 percent living in or near the poverty line (PHI n.d.). This means long-term care supply is short and has been for decades. When demand outpaces supply, prices will only continue to rise.

But eldercare, much like health care, is a fairly inelastic good, meaning even as costs increase, people’s demand for it does not change much. That is because long-term care is a necessity, not a choice. Individuals who need long-term care often cannot perform necessary daily self-care tasks for themselves, like bathing or showering, getting dressed, or walking across a room. Long-term care ensures they can live with dignity as they continue to age.

The US, however, lacks a comprehensive, affordable, and accessible long-term care system. As a result, aging lower-income and middle-class Americans1 are forced to spend down their assets to cover the rising costs of home care, assisted living, and nursing facilities. By examining how long-term care needs impact older Americans’ finances and bequest expectations, this brief illustrates the consequences of the US’s long-term care system on low- and middle-income families.

Long-term care is not just an individual health issue, but a structural driver of wealth inequality. By maintaining a system that depends on unpaid family caregiving, provides public support only after families have nearly exhausted their savings, and allows private, profit-driven companies to capture rising care costs, the US effectively penalizes aging.

Using data from the 1992–2022 waves of the Health and Retirement Study (HRS), I demonstrate that long-term care needs lead to a decline in household wealth for low-income and middle-class Americans. About 2–4 years before a high level of care is needed, net wealth declines more sharply than under typical patterns of depletion from retirement, and continues for another two years after. The wealthiest Americans are able to recover financially from these declines, while low-income and middle-class families experience permanent losses. Expected bequest amounts also show a parallel pattern.

Long-term care costs can essentially deplete older middle-class Americans’ wealth, leaving little to be passed on to younger generations. This spend-down process interrupts the potential for intergenerational wealth building, after what is often a lifetime of work and saving by low-income and middle-class families, perpetuating cycles of wealth inequality. Meanwhile, these costs are increasingly captured by profit-driven corporations and private equity firms.

In some cases, adults may decide to instead rely on unpaid family caregiving from adult children rather than spend down their assets entirely. While this may increase the chances of leaving a bequest to a family member, unpaid family care is not without its own intergenerational costs. Like demand for formal long-term care services, unpaid family care to older adults in the US is increasingly common (Caregiving in the US 2025). While relying on unpaid family care may help to avoid long-term care costs in the short run, caregivers often face other financial costs and intergenerational wealth impacts from stymied career growth, reduced income, and reduced financial savings for their own retirements as a result of care responsibilities, on top of the mental and physical costs the often come with caregiving.

Long-term care is not just an individual health issue, but a structural driver of wealth inequality. By maintaining a system that depends on unpaid family caregiving, provides public support only after families have nearly exhausted their savings, and allows private, profit-driven companies to capture rising care costs, the US effectively penalizes aging. The result is a system that drains the resources of low-income and middle-class families, eroding their ability to build or transfer wealth across generations. In this way, long-term care is both a symptom and a cause of the nation’s deepening wealth divide. It is a force shaping who gets to grow old with security and who bears the financial cost of care.

I. Risks and Costs of Long-Term Care

The majority of Americans will need some amount of long-term care in their lifetimes. Over half (56 percent) of Americans that turned 65 between 2022–25 will develop a need for long-term services and supports (LTSS), with one in five of those adults (22 percent) needing care for more than five years (Johnson and Dey 2022). Currently, over 8.3 million adults over 50 have difficulty with one or more activities of daily living (ADLs) (Forden and Ghilarducci 2025). ADLs are a set of self-care tasks that researchers and healthcare professionals use to assess care need. They include walking across a room, getting dressed, bathing or showering, eating, getting in or out of bed, and using the toilet. The total number of older adults that struggle with ADLs will only grow as Baby Boomers begin to enter the latter years of retirement.

Unfortunately, most Americans underestimate their risk of needing long-term care. Only 43 percent of people aged 50 and older think it is likely they will need long-term care in the future. More importantly, many more underestimate their financial need for long-term care: 62 percent mistakenly think Medicare will cover costs if they need to move into a nursing care facility (Montoya and Bynum 2025). Medicare does not cover long-term care. Adults must pay their own care costs out-of-pocket unless they qualify for Medicaid long-term care by meeting much more stringent income and asset eligibility thresholds.

Adults will have to make a choice: spend down the assets they have spent a lifetime building up and leave nothing for the next generation, or rely on unpaid family and friend caregiving, which comes with its own set of costs—financial, emotional, and physical—borne by the caregiver.

But long-term care is prohibitively expensive. The national yearly median cost of long-term care in 2025 was roughly $80,000 for in-home care, and ranged from $25,000–$74,000 for community and assisted living and $115,000–$129,000 for nursing home care (CareScout n.d). Families are estimated to pay more than a third (37 percent) of the expected costs adults age 65 and older will incur from long-term care, with 14 percent expected to pay at least $100,000 out of pocket (Johnson and Dey 2022). That is much more than median household income for households with a member age 65 or older of around $57,000 (Kollar and Scherer 2025).

Few Americans have enough savings to cover long-term care costs out-of-pocket. Four in ten adults (43 percent) say they are not confident that they will have the financial resources to pay for the care they might need as they age (Hamel and Montero 2023). Whereas those at the bottom of the wealth distribution can rely on Medicaid long-term care and those at the top of the distribution will be able to pay for care out-of-pocket as needed, a portion of the American middle class will likely spend down their assets until they qualify for Medicaid or rely on unpaid family caregiving if it is an option. This forgotten middle often relies more heavily on unpaid care from family members, largely wives and daughters (Forden and Ghilarducci 2023).

Long-term care needs as adults age place serious pressures on the financial and nonfinancial resources families rely on across generations. Adults will have to make a choice: spend down the assets they have spent a lifetime building up and leave nothing for the next generation, or rely on unpaid family and friend caregiving, which comes with its own set of costs—financial, emotional, and physical—borne by the caregiver. Together, these dynamics constitute an underappreciated source of resource depletion that forestalls intergenerational wealth building among American families, especially middle-class families, who feel this squeeze the hardest.

II. How US Long-Term Care Works

The US does not have a unified or universal long-term care system. Instead, it relies on a patchwork of unpaid family caregiving, out-of-pocket private pay options, and limited, onerous-to-access public support through Medicaid. As a result, the system leaves the majority of Americans and their families to navigate a complex and costly set of options to meet their own and their loved ones’ long-term care needs.

Unpaid family and friends perform 75–80 percent of all eldercare hours in the US (Spillman, Allen, and Favreault 2021). In 2021, unpaid family caregivers to an adult performed 36 billion care hours, an estimated $600 billion in economic value (Reinhard et al. 2023). These unpaid caregivers are majority women (61 percent), often wives and adult daughters, and nearly a quarter (24 percent) care for more than one care recipient (Caregiving in the US 2025). Many juggle employment and caregiving simultaneously, sometimes cutting back on paid work or leaving jobs altogether to provide care (Forden 2024).

Paid care is less common generally, but often necessary as care needs intensify. About 48 percent of adults who develop severe care needs end up receiving some paid care (Johnson and Dey 2019). Median long-term care costs are rising precipitously each year due to increasing demand and insufficient supply. In 2024, paid care prices ranged from $26,000 for one year of five-days-per-week adult day care services to $128,000 for a year in a private nursing home room (Houser 2026). For most families, paying out-of-pocket can quickly deplete savings and home equity.

Meanwhile, public coverage for long-term care is fragmented and restrictive. While Medicare, the federal health insurance program for adults age 65 and older, provides short-term (up to 100 days of) skilled nursing or rehabilitation after a hospital stay, it does not cover ongoing assistance with activities of daily living (ADLs) like using the bathroom, eating, or getting in and out of bed (Colello 2025).

Medicaid is the primary public program that covers long-term care costs for Americans, and is the largest payer of formal long-term care services in the US. In 2023, Medicaid accounted for 46 percent of the $564 billion dollars spent on long-term services and supports (LTSS). Out-of-pocket spending, in contrast, accounted for 14 percent of all LTSS spending or about $80 billion, but was still the largest component of private spending on LTSS in 2023 (Colello and Sorenson 2025).

Terms and Definitions

Eldercare, long-term care (LTC), and long-term services and supports (LTSS) are often used interchangeably, but they emphasize different aspects of the same set of tasks and services meant to help and support older adults and people with chronic illnesses or disabilities who need assistance with daily life.

- Long-term care (LTC) generally refers to a broad range of medical and personal care services provided over an extended period to people who can no longer fully care for themselves due to aging, illness, or disability.

- Long-term services and supports (LTSS) is a term used by researchers and policymakers to describe both the paid and unpaid services that help people meet daily needs, whether provided in the home, community, or institutional settings.

- Eldercare is a more general term that encompasses both LTC and LTSS but specifically focuses on the care of older adults.

This brief uses these terms interchangeably, but primarily refers to long-term care to describe the continuum of supports older adults rely on to live with dignity and independence. People are considered to need long-term care when they have trouble with daily functioning, often measured by some combination of difficulty with activities of daily living (ADLs) and instrumental activities of daily living (IADLs), or cognitive decline (Colello 2025).

- Activities of daily living (ADLs) are routine self-care tasks that most healthy individuals can perform daily without assistance, including

- walking across a room;

- eating;

- getting dressed;

- transferring (getting in and out of bed);

- using the toilet; and

- bathing or showering.

- Instrumental activities of daily living (IADLs) are necessary activities that allow a person to continue living independently, including

- grocery shopping;

- managing money;

- making phone calls;

- taking medication; and

- preparing meals.

Older adults are often considered to have a severe level of care need when they have difficulty with two or more ADLs. Under Medicaid, adults must demonstrate their state’s definition of “nursing home level” of care need, which again, differs state by state. Often this is some combination of difficulty with a certain number or set of ADLs and/or IADLs, or cognitive decline, like a dementia or Alzheimer’s diagnosis (American Council on Aging 2026).

Most Americans, however, do not qualify for Medicaid long-term care (Chen, Munnell and Wettstein 2025). To access Medicaid long-term care, adults must fall below certain household income and asset thresholds that vary state to state. As of June 2025, income limits range from $967 to $2,901 a month for a single individual, and asset ceilings are typically around $2,000 for most states (American Council on Aging 2026). Most states also implement look-back periods of 5–10 years that penalize asset transfers made within the years prior to applying. While some families may preemptively transfer assets to qualify, these strategies can be risky and require financial literacy and legal support to plan ahead. For most older adults, the transition to Medicaid occurs after assets have been exhausted.

What about long-term care insurance?

Some older adults pay for a long-term care insurance policy as a means of covering future anticipated long-term care costs. These policies often require paying premiums for a set duration prior to long-term care need onset, when policy holders can start making claims. The policies range from full coverage to fixed amounts for a limited number of years, with the latter case being more common.

Reliance on long-term care insurance is relatively low. Only 3–4 percent of adults over age 50 pay for a long-term care insurance policy (Rau and Aleccia 2023), and private insurance only accounted for 8.7 percent of all long-term supports and services (LTSS) spending in 2023 (Colello and Sorenson 2025). The long-term care insurance market has also been shrinking after years of insurers underestimating longevity and care durations. As a result, policy premiums have continued to increase to the point of unaffordability.

Anecdotal stories suggest long-term care insurance coverage is inadequate, often covering too little for too few years, or imposing restrictions, such as limited lists of covered providers, that make it impossible to meet full care needs (Rau and Aleccia 2023). Indeed, some research suggests that about a quarter of long-term care insurance policyholders over age 65 let their policies lapse, forfeiting benefits before they can be used. Lapse rates are particularly higher among those with cognitive impairment who are more likely to draw from the policies (Friedberg et al. 2023). Essentially, a substantial proportion of older adults, especially those with cognitive impairment, let their insurance policies lapse before they can fully claim their entitled benefits.

Ultimately, some portion of adults in the US simply do not get their care needs met. In 2020, over half of adults 55 and older with any reported ADL or IADL difficulties did not get any help, paid or unpaid, with those activities (Forden and Ghilarducci 2023). Single older adults without adult children are particularly at risk.

III. Long-Term Care Depletes Assets for Middle-Class Americans and Contributes to Widening Wealth Inequality

For millions of older Americans, the path from aging to needing long-term care is also a path toward financial depletion. Even families who may start retirement comfortably above Medicaid eligibility often end up spending down their assets until they qualify. More than four out of five middle-class adults over 65 who need long-term care for five years or more will eventually enroll in Medicaid, as will nearly half of upper-middle-class couples with lifetime earnings over $4.75 million. Specifically, 95 percent of this group of adults in the bottom quintile of lifetime earnings, 91 percent in the second quintile, 87 percent in the third quintile, 75 percent in the fourth quintile, and 53 percent in the top quintile will eventually enroll in Medicaid after age 65 (Johnson et al. 2021). Long-term care is often too expensive, and unpaid family caregiving alone is not a solution to meeting growing needs.

Using 1992–2022 data from the University of Michigan’s Health and Retirement Study (HRS), this analysis shows how quickly long-term care needs decrease net wealth for older adults, especially those in the middle class. Figure 1 shows the trajectory of net wealth for low-income and middle-class individuals in the years before and after individuals report difficulty with two or more activities of daily living (ADLs), a common threshold for assessing institutional long-term care need.

“Low-income” includes individuals in the bottom quarter of the income distribution based on their pre-retirement household income. The “middle class,” while notoriously difficult to define, includes individuals whose pre-retirement household incomes fall in the middle of the distribution (the 26th and 75th percentiles) of household income. I use this definition in order to capture families who have some opportunity to accumulate assets through work and saving, but whose economic security might still be substantially undermined by the onset of long-term care needs. The middle class, in particular, is most exposed in the current long-term care system. Lower-income adults are more likely to already qualify as is for Medicaid long-term care, while high-wealth households are better able to absorb rising out-of-pocket costs without exhausting their assets.

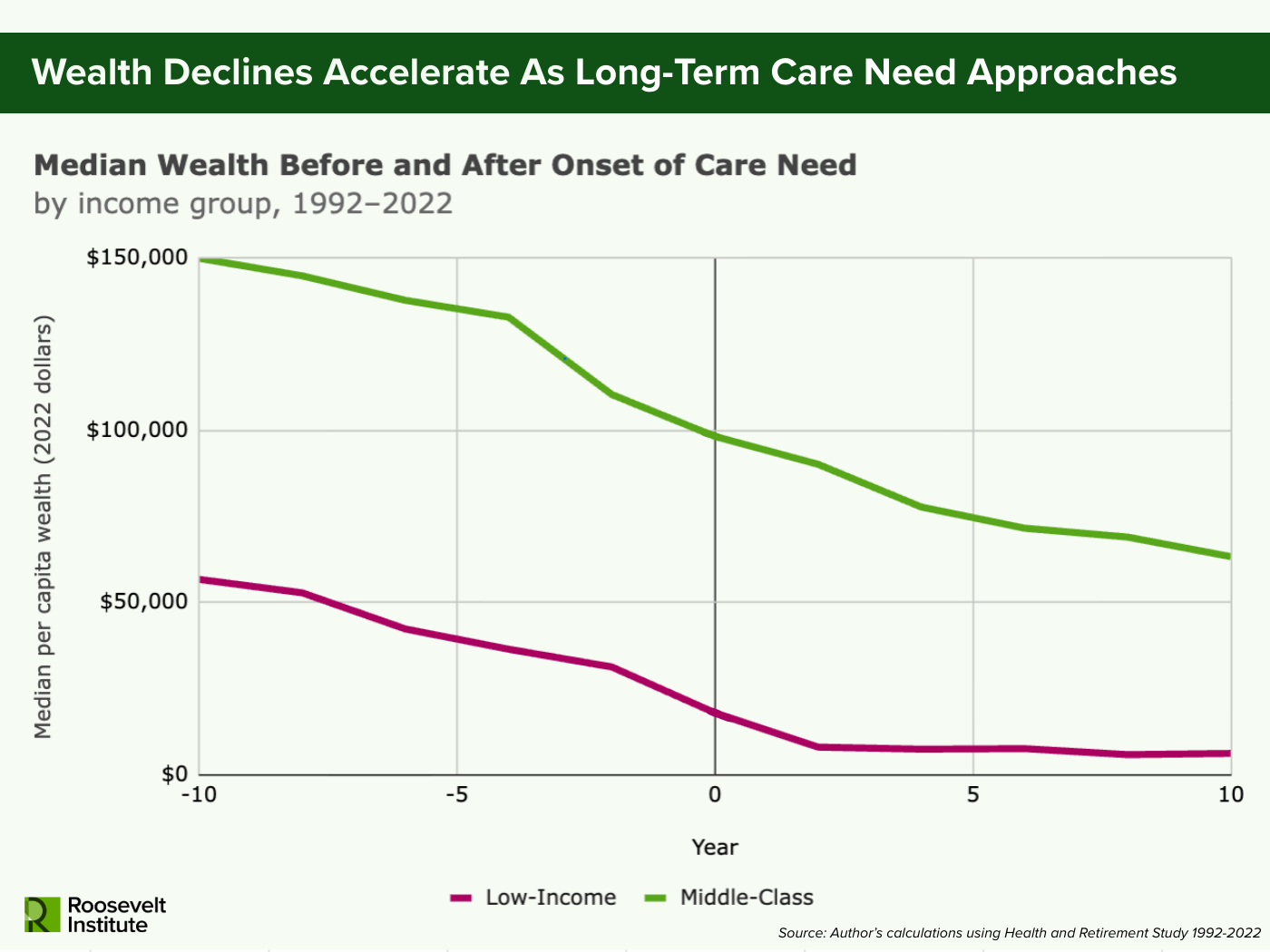

Figure 1.

Note: Sample includes adults over 50, combined respondent and nursing home resident weights applied, all wealth values in 2022 dollars. Care need onset is defined as the first wave in which a respondent reports having difficulty with two or more activities of daily living (ADLs). Low-income and middle class are calculated based on where each respondent’s pre-retirement household income falls on the household income distribution for all households in the US in the corresponding pre-retirement year. Individuals in the bottom 25% of the distribution (up to the 25th percentile) are classified as “low-income” and those in the middle 50% of the distribution (26th–75th percentile) are classified as “middle class.” Year-specific household income distribution for all US households is estimated using the Current Population Survey (CPS) Annual Social and Economic Supplement (ASEC) across 1991–2023.

Across both low-income and middle-class older adults, net wealth declines gradually over time, but begins falling more sharply two to four years before care needs arise and continues to fall at the accelerated pace for a few years after. For lower-income adults, the accelerated pace of wealth decline slows down about two years after meeting the formal definition of institutional care need. For middle-class Americans, the rate of decline continues for much longer, eventually tapering off at around the eight year mark. The leveling off among low-income adults likely reflects the point at which assets fall low enough to qualify for Medicaid coverage. Middle-class Americans, however, must continue drawing down savings for much longer before reaching any comparable floor.

That wealth declines precede year zero suggests that financial strain begins before formal disability as health issues intensify and caregiving needs build. This pattern matches previous research showing that costs linked to disability often occur before the formal onset of care need (De Nardi et al. 2016; Coe and Lindeboom 2008; Baker et al. 2006). Care needs develop gradually rather than popping up over night, and care-related spending likely starts increasing during this earlier ramp-up period. In the interim, families likely fill the gap through unpaid or privately financed support.

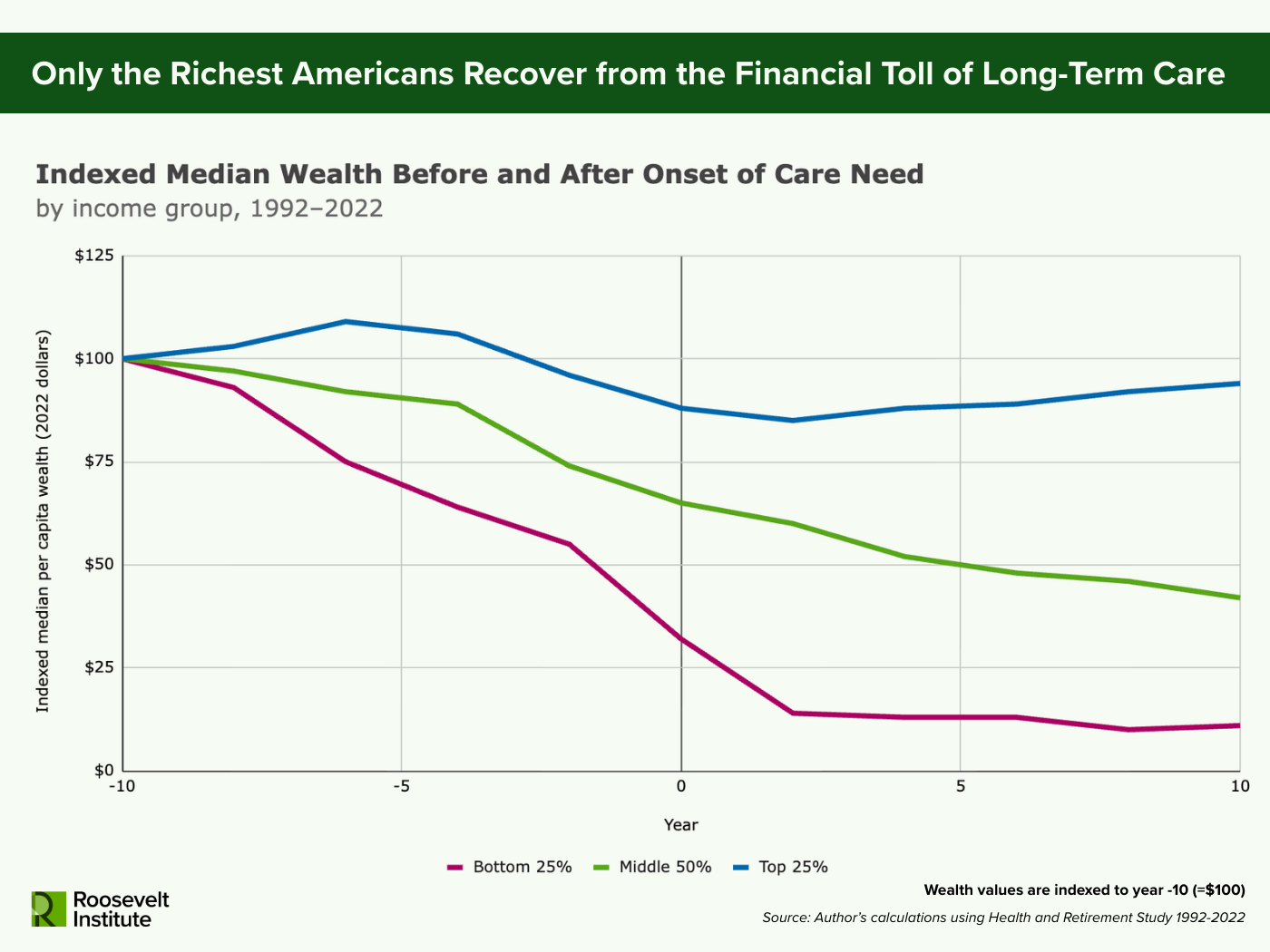

Figure 2.

Note: Sample includes adults over 50, combined respondent and nursing home resident weights applied, all wealth values in 2022 dollars. Wealth values are indexed at 100 to the first year of data (year -10 = 100). Care need onset is defined as the first wave in which a respondent reports having difficulty with two or more activities of daily living (ADLs). Income groups (bottom 25%, middle 50%, and top 25%) identify where a respondent’s pre-retirement household income falls on the household income distribution for all households in the US in the corresponding pre-retirement year. Year-specific household income distribution for all US households is estimated using the Current Population Survey (CPS) Annual Social and Economic Supplement (ASEC) across 1991–2023.

Not all families are similarly affected by long-term care costs though (see Figure 2). For the highest-income Americans (the top 25 percent), the decline in median wealth near care onset is a smaller percentage decline compared to their lower-income peers. More importantly, the decline is not permanent. Those in the top 25 percent eventually regain enough wealth at the median to make up about 94 percent of their starting assets, while lower-income and middle-class individuals face permanent reductions to just 11 percent and 42 percent of their original, and much lower, wealth levels. High-income households, in other words, can absorb out-of-pocket care costs without fundamentally altering their long-run financial position. Low-income and middle-class families cannot. Instead, long-term care permanently drains assets from the middle class and lower-income families that might otherwise support retirement security or be passed on to the next generation.

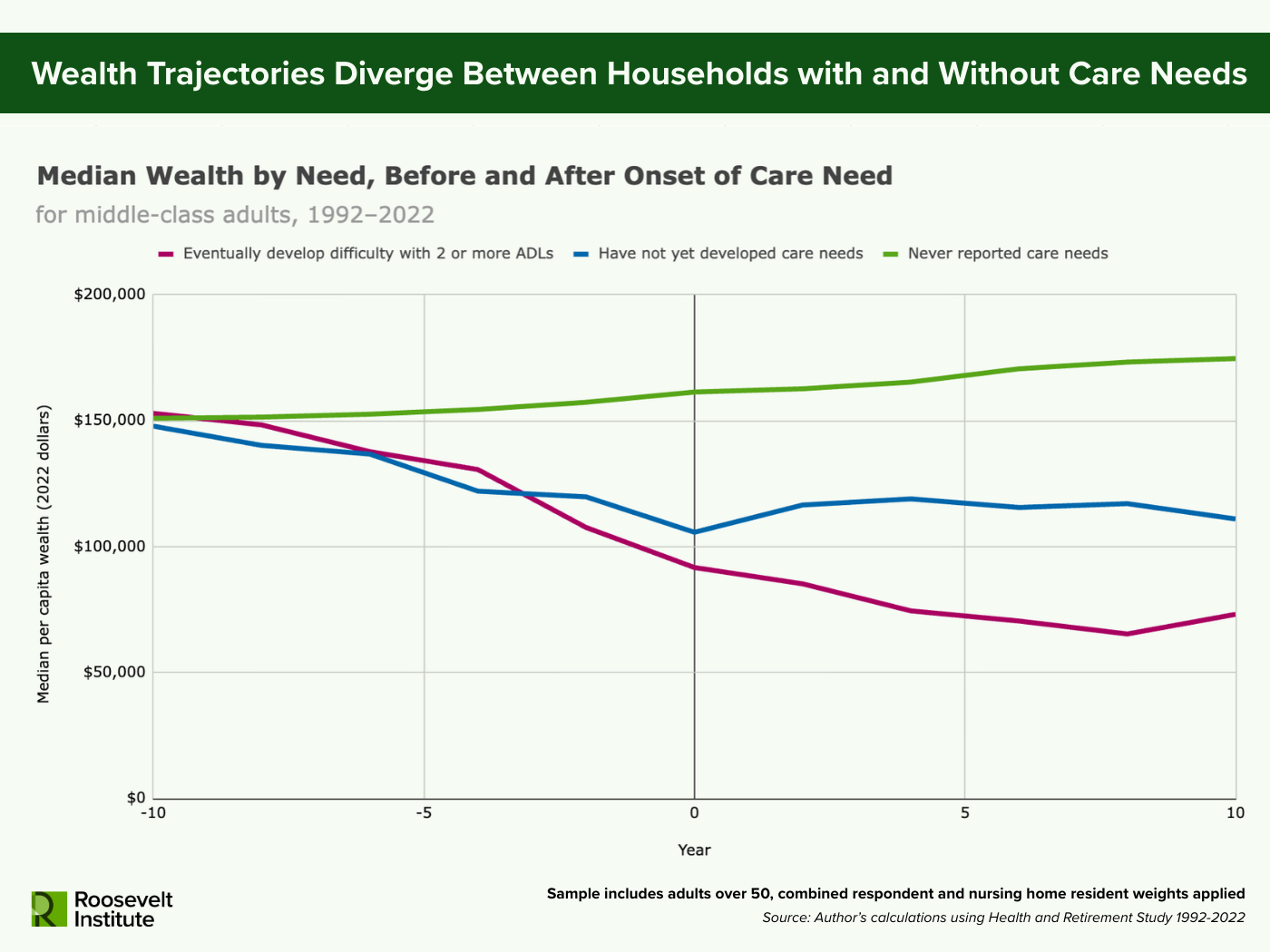

Figure 3.

Note: Sample includes adults over 50, combined respondent and nursing home resident weights applied, all wealth values in 2022 dollars. Care need onset is defined as the first wave in which a respondent reports having difficulty with two or more activities of daily living (ADLs). Middle-class is defined as falling in the middle 50% of the household income distribution (26th–75th percentile) in an individual’s pre-retirement year. Year-specific household income distribution for all US households is estimated using the Current Population Survey (CPS) Annual Social and Economic Supplement (ASEC) across 1991–2023. The treated group contains individuals who eventually develop difficulty with two or more ADLs. The control group is a synthetic cohort matched on age band, survey wave, and pre-retirement income category. The never-treated group is drawn from individuals who have never reported care needs in the survey sample, while the not-treated-yet group is drawn from individuals who have not yet developed care needs in the survey wave.

When we focus on the middle class, we can also examine what would have happened to their wealth trajectories if they had not developed long-term care needs (see Figure 3). By comparing middle-class older adults who eventually develop long-term care needs to similar adults who do not or have not yet, the divergence in wealth is clearer. At the start, all groups begin with comparable median wealth, around $150,000 per capita. Among those who eventually need care, median wealth declines in the decade leading up to care need onset, falling by roughly 40 percent or just over $61,000. Most of this decline happens in the four years immediately preceding the onset of care need, showing an acceleration of asset drawdown before year zero. After care need onset, wealth depletion continues, with median assets for this group falling for several years and reaching a low of $65,000 by about eight years after onset.

In contrast, adults who never develop care needs in the survey, follow a different path. Assets rise modestly over the full 20-year period by around $24,000. This group is likely younger, wealthier, and healthier compared to individuals who eventually have care needs, and so are continuing to accumulate wealth as would be expected. By 10 years after the reference point (year zero), those never needing care have about $100,000 more in median assets than individuals who experienced care needs.

While households at the top end of the wealth distribution can absorb long-term care expenses, the majority of American families cannot. For middle-class families, long-term care costs are more likely to eliminate not only the assets of the older generation, but also to impact the capacity of the next generation to build wealth.

Adults who have not yet developed care needs in a given survey wave, but might report care needs at a later survey wave, sit in the middle. Their median wealth declines over a 10-year period, but less sharply than those who need care. At year zero, this group has over $11,000 more in median wealth than those who need care. By 10 years after the reference year, individuals who have not developed care needs yet have nearly $34,000 more in median wealth than those who did. These diverging trajectories between groups highlights how long-term care accelerates asset depletion among the middle class beyond normal retirement draw downs.

Together, Figures 1, 2, and 3 show that long-term care drains wealth for the American middle class. It accelerates the draw down of assets, eroding the potential for modest bequests to children. Since Medicaid coverage only kicks in after assets are nearly gone (in most cases), the US long-term care system essentially requires middle class families to spend down before accessing public support. In doing so, it turns long-term care from a personal health challenge into a structural component of downward mobility and intergenerational wealth inequality.

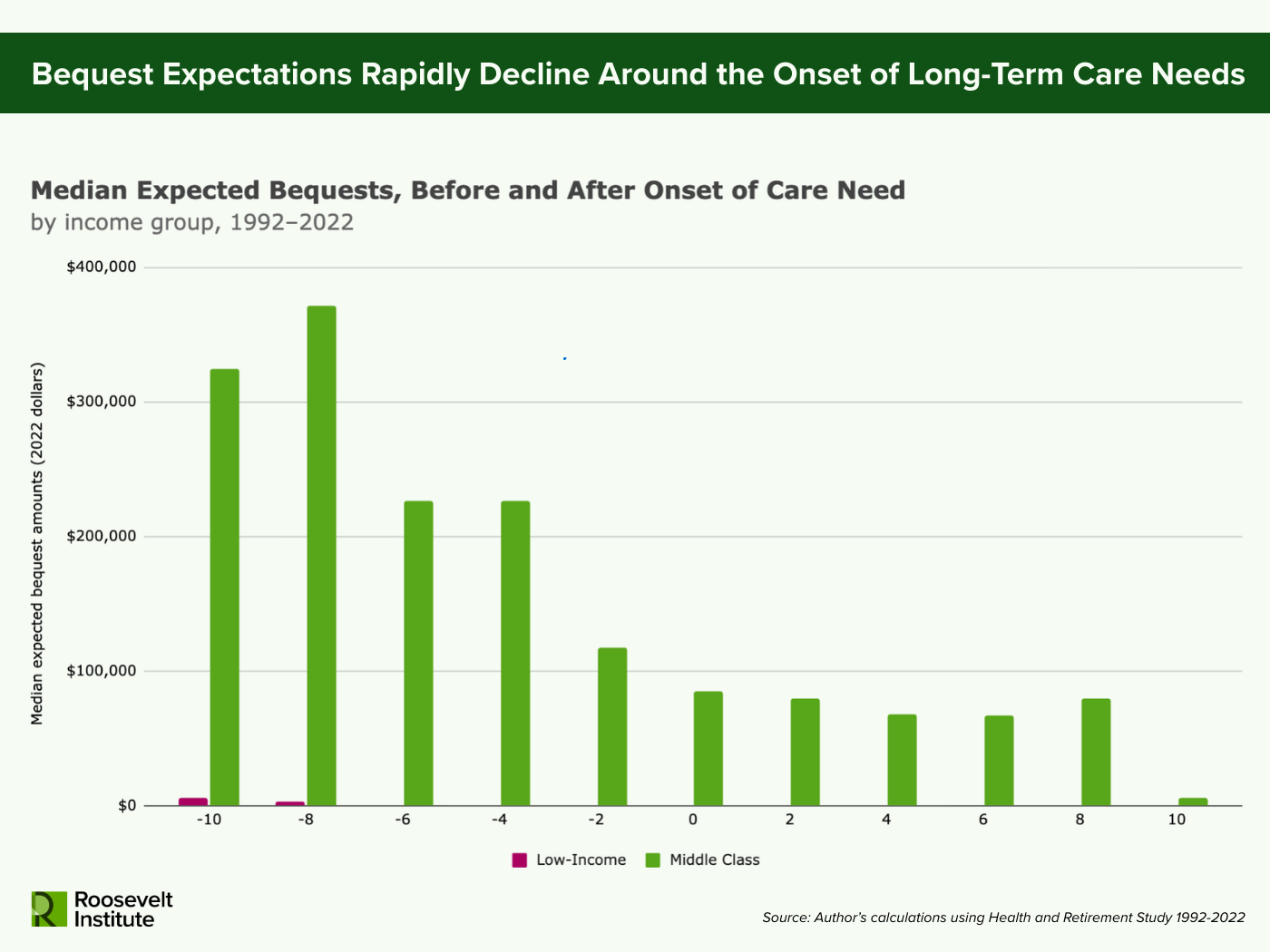

Figure 4.

Note: Sample includes adults over 50, combined respondent and nursing home resident weights applied, all wealth values in 2022 dollars. Care need onset is defined as the first wave in which a respondent reports having difficulty with two or more activities of daily living (ADLs). Middle-class is defined as falling in the middle 50% of the household income distribution (26th–75th percentile) in an individual’s pre-retirement year. Low-income is defined as falling in the bottom 25% of the household income distribution in an individual’s pre-retirement year. Year-specific household income distribution for all US households is estimated using the Current Population Survey (CPS) Annual Social and Economic Supplement (ASEC) across 1991–2023. Expected bequest amounts are imputed based on respondent’s expectation of the probability they would leave any bequest, a bequest of $10k or more, a bequest of $100k or more, or a bequest of $500k or more.

In fact, Americans who need long-term care expect to leave their kids less money (Chen, Munnell, and Wettstein 2025). When comparing expected bequest amounts of middle-class Americans before and after a severe level of care need, there is a similar pattern to that of the net wealth figures, where expected amounts drop significantly over the two years before and after onset (see Figure 3). For low-income older adults, bequest amounts are practically zero across the board.

The decline in expected bequest amounts for middle class Americans around long-term care needs suggests that families are forced to sacrifice their capacity to pass on wealth to the next generation in order to pay for present long-term care costs. For middle-class Americans, this spend-down dynamic represents an underappreciated mechanism of intergenerational wealth extraction. While households at the top end of the wealth distribution can absorb long-term care expenses, the majority of American families cannot. For middle-class families, long-term care costs are more likely to eliminate not only the assets of the older generation, but also to impact the capacity of the next generation to build wealth. A long-term care system structured around private payment till asset depletion perpetuates wealth inequality across generations.

IV. Unpaid Care Also Comes with Intergenerational Costs

The intergenerational financial toll of long-term care extends beyond the cost of formal services. Many older adults rely on some unpaid caregivers, who step in when paid care is unavailable or insufficient. But this “free” care is far from costless. It shifts the bill from aging parents to their adult children by impacting these caregivers’ own capacity for wealth building.

The economic impacts of unpaid eldercare to caregivers is well documented. Caregivers may reduce work hours, forgo career advancement, and even leave the labor force altogether (Maestas, Messel, and Truskinovsky 2023; Moussa 2019; Skira 2015). Such impacts reduce an individual’s lifetime earnings, decreasing their capacity to save for the future and build their own financial stability and wealth. Research by the Urban Institute highlights how unpaid family caregivers have an increased probability of falling into poverty and experience smaller percentage growth in assets as well (Butrica and Karamcheva 2018).

The result is an intergenerational double bind. Older adults spend down their assets to pay for care, while the younger generation sacrifices income and savings to provide unpaid care. In both cases, wealth that might have been preserved, passed down, or built instead disappears, either to the cost of care or to the economic penalties of caregiving itself. This dynamic shows how the intergenerational consequences of our long-term care system may be especially impactful for middle-class families. In this way, long-term care is not simply an economic risk older adults face as they age, but a structural and institutional factor shaping intergenerational wealth trajectories for middle-class and low-income families.

Conclusion

Long-term care in the United States places downward pressure on middle-class intergenerational wealth building. Working families who have spent a lifetime saving for retirement are forced to draw down their assets, often at an accelerating rate in the years surrounding the onset of long-term care needs until little remains. This spend-down process is not a reflection of poor planning or financial irresponsibility, but a predictable outcome of a system designed to offer public support only after families have functionally exhausted their savings.

The result is that long-term care costs decrease the wealth of aging middle-class families and their children, eliminating the financial buffers that sustain security in old age and enable intergenerational wealth building. While Medicaid serves as a funder of last resort for care, it is available only after near-total asset depletion. Those at the top of the wealth distribution can absorb long-term care costs without substantial losses, but for most Americans, the burden of paying for care wipes out decades of savings and home equity.

To build a sustainable and equitable care system, policy must recognize long-term care not only as an individual health issue but as a structural contributor to wealth inequality. Protecting low-income and middle-class families from financial depletion in old age and ensuring that wealth can be passed forward rather than drained away requires robust public investment and a new social contract that values care as a shared public good rather than a private burden.

Footnote

- In this brief, low-income and middle class are defined based on where pre-retirement household income falls on the household income distribution for all households in the US. Individuals in the bottom 25 percent of the distribution (up to the 25th percentile) are classified as “low-income” and those in the middle 50 percent of the distribution (26th–75th percentile) are classified as “middle class.” ↩︎

Acknowledgments

The author would like to thank Matt Hughes, Suzanne Kahn, Michael Madowitz, Noa Rosinplotz, and Aastha Uprety for their feedback, insights, and contributions to this paper. Any errors, omissions, or other inaccuracies are the author’s alone.

Suggested Citation

Forden, Jessica. 2026. “How Long-Term Care Costs Drain the Middle Class and Deepen Intergenerational Wealth Inequality.” Roosevelt Institute, April 9, 2026.

RELATED RESOURCES

Author