What’s Going on with Private Credit? (with Graham Steele)

April 28, 2026

By Brad Lipton

Private credit firms are companies that are not banks that lend money to other companies, making loans that are not as well regulated as bank loans, nor as transparent as issuing bonds. Private credit has spent years in the shadows of the financial system, growing rapidly but quietly, largely unregulated, and poorly understood by most people outside of Wall Street. Now it’s making headlines, and not for good reasons.

In a new conversation, Roosevelt President and CEO Elizabeth Wilkins sits down with Senior Fellow Graham Steele, former assistant secretary for financial institutions at the US Department of the Treasury, to break down how private credit works, how it became more than a trillion-dollar market, and why financial observers are starting to ask uncomfortable questions about what happens if things go wrong. Elizabeth and Graham walk through the warning signs, the policy options, and what the 2008 financial crisis can (and can’t) tell us about the road ahead.

In this blog post, we discuss how private credit fits into the larger landscape of the financial system and what is at stake for American families and the economy.

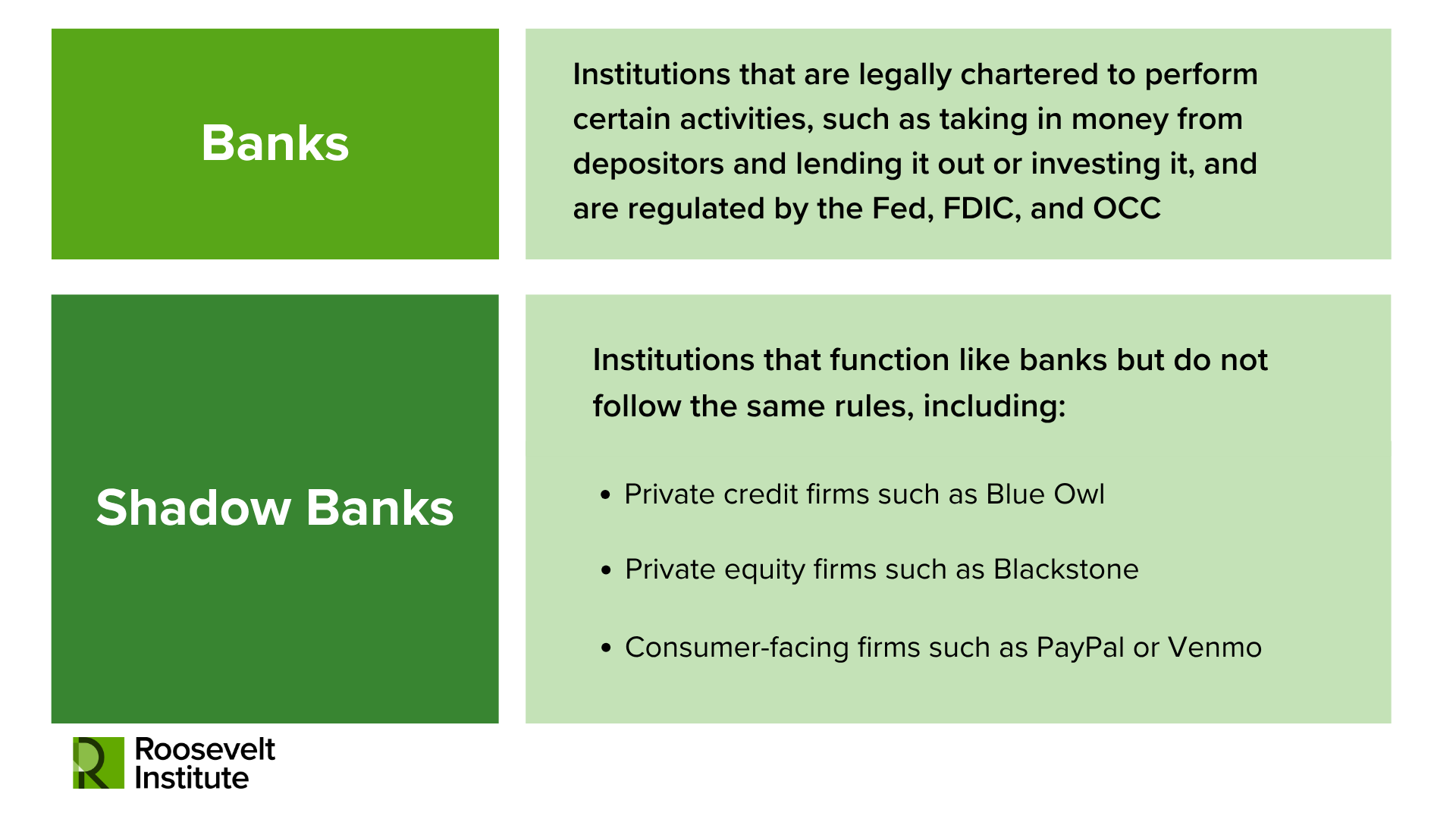

Shadow Banking

Private credit firms engage in a form of shadow banking—bank-like activity, such as taking in money from depositors or investors and lending it out, that doesn’t follow the regulations that govern banks.

Shadow banks: institutions that function like banks—such as by taking in money from depositors or investors and lending it out—but do not follow the same rules

The financial system has a variety of functions, including accepting deposits or investments, facilitating the transmission of money, and facilitating lending or investment by people or companies with money to people or companies that need money. So-called “public markets” are highly regulated ways that companies in the financial system conduct financial activity. For example, “publicly traded” companies offer investment in their company in the form of shares sold on a stock exchange. A variety of rules govern this activity, such as detailed public disclosure requirements. Likewise, banks are financial institutions with a formal charter from the government to perform certain activities, such as taking in money from depositors and lending it out or investing it. Banks are subject to a range of rules put in place primarily by (in the US case) the Federal Reserve, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation (FDIC) to protect depositors and the financial system.

Yet there is also financial activity—so-called “shadow banking”—that operates in whole or in part outside of this system of rules (sometimes known as the “regulatory perimeter”). Companies engaging in this activity may take advantage of exceptions that allow them to operate in a less regulated manner, including often with much less disclosure. Other times, they simply flout the rules. These companies’ activity is sometimes also said to occur in “private markets.”

There isn’t a single definition of shadow banking. Private equity—raising money outside of public markets and using that money to buy portions of other companies—is a well-known component of the sector. Consumer-facing firms specializing in money transmission, such as Venmo or PayPal, have sometimes also been described as shadow banks. More recently, private credit has been making headlines.

Private Credit

Some big companies that received loans from private credit firms recently went bankrupt. In turn, some investors in private credit have begun to pull their money out, raising concerns about the possibility of a crisis spilling over to the financial system more broadly.

Private credit firms have been popular with investors because their loans come at higher interest rates. These higher rates reflect that this lending is riskier than loans made by banks because these lenders use looser underwriting, such as fewer requirements for collateral.

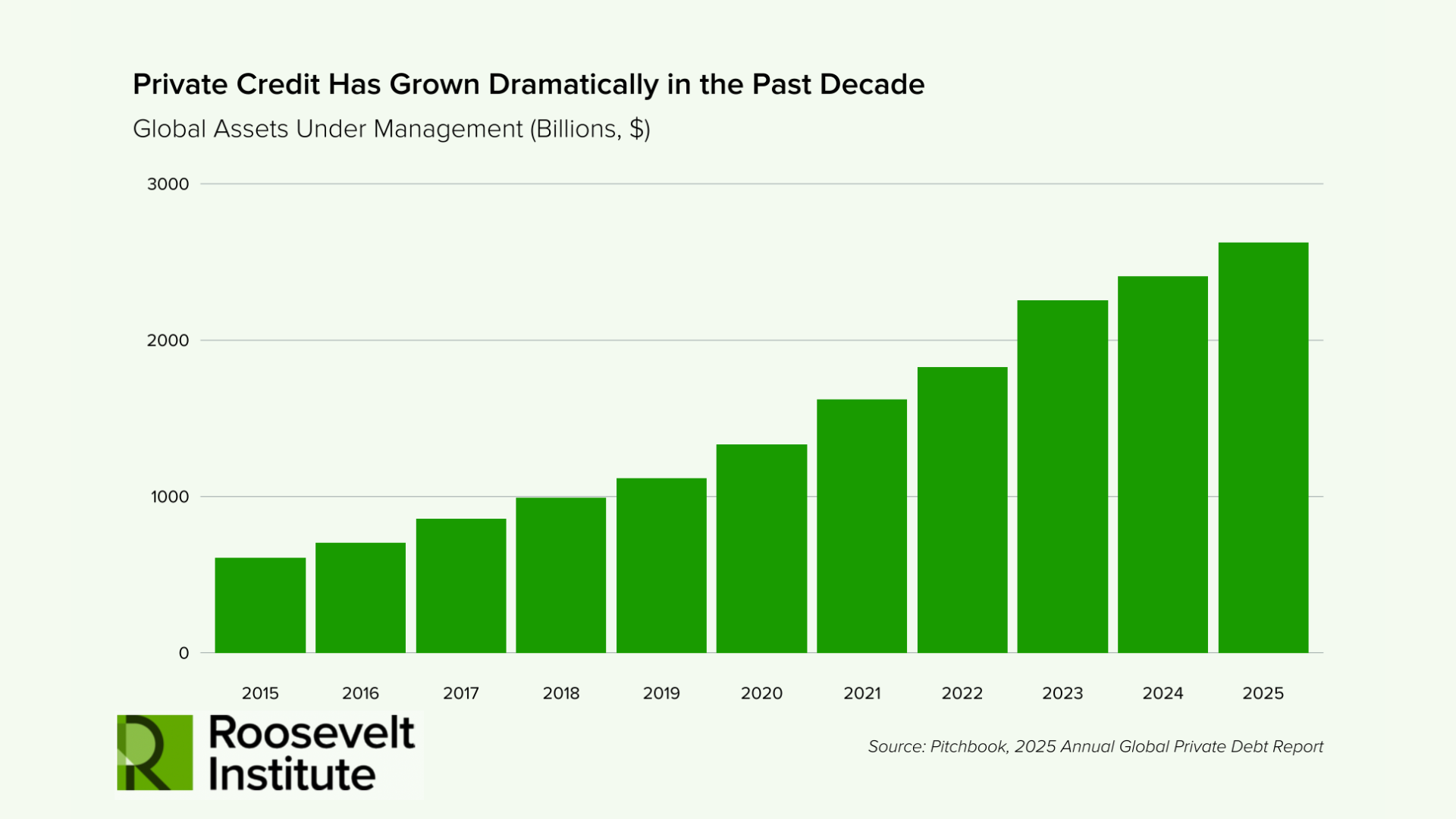

Private credit has grown dramatically in recent years, in both the United States and globally.

Investors in private credit are mostly institutions, such as pension funds, foundations, and endowments. In 2018, Harvard announced it was investing $300 million in private credit. The largest public pension fund, the California Public Employees’ Retirement System, as well as the Indiana Public Retirement System, the Ohio School Employees Retirement System, and the University of California each invested at least $100 million in private credit in 2022.

Investment in private credit by individual people has also been growing in recent years. Since there is limited disclosure about private credit, it is difficult to figure out the exact size of the market, but some have estimated that total private credit in the US has tripled since 2015 to at least $1.3 trillion. Moreover, while today individual investors in private credit must specifically seek out such investments, the Trump administration has recently been trying to lower the standards for what is offered in people’s tax-advantaged retirement accounts, such as 401(k)s, to permit “alternative investments” like private equity, private credit, and crypto. This change could prompt people with less information about private credit to invest their precious retirement dollars in it.

Some of the biggest private credit firms are companies also known for their private equity activity, such as Apollo, Blackstone, Ares, KKR, and Carlyle. (When these firms raise money and use it to buy portions of other companies, they are engaging in “private equity.” When they make loans and earn returns via interest payments and fees, they are doing “private credit.”) There are also some large firms that specialize more specifically in private credit. One of the largest and most well-known of these companies is Blue Owl.

What’s at Stake

If private credit firms were to fail, both investors in private credit and the companies borrowing money from them, including their workers and customers, could be at risk.

As Graham says in his interview with Elizabeth: “How concerned should we be? The short answer is, we really don’t know. The agencies that are responsible for tracking these risks, like the Securities and Exchange Commission or Treasury Department, have by and large been asleep at the switch for a lot of the growth of these markets.”

As private credit and other forms of shadow banking continue to grow, policymakers will need to consider the risks to individual people as well as to the larger stability of the financial system. Proponents of shadow banking may argue that some financial activity can be conducted with less government oversight without creating problems for anyone else, perhaps because the people involved are particularly sophisticated. But the track record of shadow banking, including possibly now in private credit, casts doubt on that idea. To ensure that real risks do not grow unnoticed until there is a crisis, it may be appropriate to apply more disclosure and other rules to shadow banking (and enforce existing rules). Moreover, to the degree that interdependencies between public markets and private markets—such as banks lending to private credit firms—present risks to the whole system, regulators may need to reconsider the rules for those connections.

Given the trouble that may be brewing in private markets, now is certainly not the time to allow risky investments like private credit into retirement plans. And if the private credit market does ultimately need emergency relief, policymakers should provide it first to workers at companies that are at risk and everyday people who are invested in private credit, including retirees in pension plans, before even thinking about bailing out the private credit firms themselves.

Author

Brad Lipton

Director, Corporate Power and Financial RegulationAs director of the corporate power and financial regulation program, Brad Lipton leads Roosevelt's work on the rules governing financial institutions and other corporations to produce a more equitable economy.