Unlocking the Significant Potential of Mortgage Refinancing for Working Families

June 16, 2026

By Brad Lipton and Peter Carroll

Key Takeaways

- When interest rates fall, the gains from mortgage refinancing flow disproportionately to wealthy homeowners—not because helping lower-income borrowers is unprofitable, but because of fixable friction. Targeted, low-cost policy interventions could put thousands of dollars per year into the pockets of millions of families who are currently left out.

- Fixed closing costs, paperwork burdens, and lender focus on larger loans all make refinancing harder for lower-income borrowers. Some down payment assistance programs make matters worse by imposing clawbacks that can penalize borrowers for refinancing into a lower rate.

- The policy fixes are concrete and cost-effective. Modernize IRS rules so states can use tax-exempt bonds for refinancing. Streamline underwriting—a borrower’s payment history usually already tells lenders what they need to know. Waive closing cost taxes for low-income borrowers: A one-time $2,000 fee waiver unlocks $884 or more in annual savings.

- Low-income borrowers who don’t refinance are effectively subsidizing the lower rates that high-income borrowers get when they do. Fixing this isn’t just good housing policy; it’s correcting a market failure that concentrates the benefits of monetary policy at the top.

Executive Summary

Mortgage refinancing makes homeownership more affordable and is one of the main ways that individual households benefit directly from falling interest rates. The benefits from refinancing can be substantial—thousands of dollars per year in the pockets of families with even relatively low mortgage balances, every year for the life of the mortgage loan, with corresponding lower default rates. Indeed, refinancing can put as much money into low-income borrowers’ pockets every single year as some significant government stimulus programs, such as the American Rescue Plan (ARP), have done once. Hence, refinancing can provide much more benefit to each borrower cumulatively than those programs have (Stein and Bhagat 2021). Nonetheless, the benefits of refinancing have disproportionately gone to higher-income Americans in recent years. This report argues that policymakers at the state and federal level should change this dynamic with targeted, cost-effective government interventions, to the benefit of hundreds of thousands or even millions of low- and middle-income families.

Introduction: What Mortgage Refinancing Is and Who Benefits from It

Mortgage refinancing is the process by which a homeowner replaces their existing mortgage with a new one without selling their home. The homeowner pays off their existing mortgage with a particular financial institution by securing a new mortgage from the same or a different financial institution (CFPB 2020).

To start with the basics, a mortgage is a loan from a financial institution that is secured by a lien on a dwelling (CFPB 2024a). The mortgage is for a particular amount, known as the principal, and has an associated interest rate, which can either be “fixed” or “adjustable” (FDIC 2024). Taking out a mortgage has certain associated one-time costs, known as “closing costs” (CFPB 2024b). The mortgage has a particular duration, or loan term, over which the homeowner typically makes monthly payments.

Although the 30-year mortgage is the most common in the United States, there has recently been discussion about offering a wider variety of loan terms, such as a 50-year mortgage (Leath 2025). All other things being equal, the shorter the loan term, the less interest the homeowner pays and the faster the homeowner pays off the loan, reducing the principal amount and hence accumulating “equity” (money that does not need to be paid back upon selling the home or refinancing) (Bertelsen 2022). Hence, keeping other factors equal, a mortgage with a shorter term will have a higher monthly payment, and the homeowner will accumulate equity faster. Conversely, a mortgage with a longer term will have a lower monthly payment, but the homeowner will pay the mortgage off, and accumulate equity, more slowly and pay more total interest over the life of the loan. Regardless of the length of the mortgage term, homeownership fundamentally differs from renting because homeownership includes a speculative investment—i.e., the homeowner takes on the risk and benefit of any appreciation or loss of the home’s value when the home is sold.

Refinancing a mortgage requires homeowners to pay the upfront costs of securing a new mortgage for the benefit of a lower interest rate on the new mortgage (Compass Mortgage n.d.). Because these closing costs generally do not vary with loan amount, these costs have a disproportionate effect on the economics of refinancing for borrowers with lower mortgage balances, who tend to have lower incomes.

Most commonly, when interest rates fall, refinancing allows homeowners to reduce their monthly mortgage payments. If other loan terms stay the same (or at least mostly the same), a lower interest rate translates into a lower monthly payment, to the homeowner’s benefit. Alternatively, homeowners can refinance to build equity faster under a shorter loan term (CFPB 2020; Freddie Mac 2025), to get cash (i.e., to “cash out,” by refinancing for a loan amount that is more than the remaining principal of the existing mortgage), or to replace an adjustable interest rate with a fixed one (CFPB 2020).

Refinancing makes homeownership more affordable by reducing homeowners’ monthly payments by hundreds of dollars per month on average, which is thousands of dollars per year and many thousands of dollars in total over the course of a loan. For example, a homeowner that originated a 30-year mortgage with a principal balance of roughly $199,000 at an interest rate of 6.875 percent in 2024 would save about $1,200 each year (or about $100 per month) from refinancing at a new rate of 6.125 percent in 2026—for the life of the mortgage. For an original principal balance of $300,000, the annual savings would be about $1,800 and the monthly savings would be about $150. If interest rates continue to fall, homeowners could benefit even more, and more homeowners could benefit. Refinancing therefore is a significant opportunity for at least some homeowners to substantially improve their household balance sheets.

Relatedly, refinancing has also been shown to significantly decrease mortgage default rates (Abel and Fuster 2021). In particular, reducing monthly mortgage payments produces an especially big reduction in default rates for homeowners with lower credit scores (Ehrlich and Perry 2015). So refinancing should allow families, including those struggling the most, to stay in their homes at an affordable price.

Unfortunately, the benefits of refinancing have disproportionately gone to higher-income Americans during “refi booms” triggered by falling interest rates. Studies show that, when interest rates fell dramatically in 2020–21, higher-income households were significantly more likely than lower-income families to refinance and so captured much more of the gains from refinancing. One study found that, in 2020, if individuals in lower segments of the income distribution had refinanced at the same rate as individuals in the top quintile of the income distribution (and obtained similar rate reductions), they would have captured an additional $5 billion in refinance savings over the course of their loans (Agarwal et al. 2024).

Who Could Refi If Interest Rates Drop

To estimate how many households of various characteristics would benefit from refinancing at various interest rates, we analyzed publicly available Home Mortgage Disclosure Act (HMDA) data. HMDA generally requires mortgage lenders to disclose every loan they originate in the United States, including relevant characteristics of the loan and borrower(s).

We analyzed HMDA data from 2022, 2023, and 2024 to determine how many households that bought homes with a mortgage in those years would be “in the money” at various interest rates, meaning that they have existing interest rates at least 75 basis points (.75 percent) above those various rates. We followed other studies in using 75 basis points as the “in the money” threshold (Golding et al. 2020; Gerardi, Lambie-Hanson, and Willen 2021; Wheat et al. 2023).1 These three years cover higher post-COVID mortgage rates, so borrowers from this period are likely to be in the money as rates fall. Additionally, as discussed below, some borrowers from before 2020 may be in the money now because many homeowners with high-interest mortgages failed to refinance when rates fell dramatically in 2020–21.

The total number of mortgage loans in the HMDA data in 2024 was 6,176,052. This includes a variety of types of loans, including mortgages for investment and vacation properties and reverse mortgages. The relevant mortgages for this paper are loans financing the purchase of family-owned principal-residence homes (including the refinancing of such loans that could be refinanced again). Accordingly, using the variables present in the HMDA data, we define “covered loans” to mean closed-end first lien, principal residence mortgages for site-built,2 single-family (1–4 units) homes, excluding reverse mortgages. Filtering on this basis, the number of covered loans in 2024 was 3,649,951. See Table 1 for the totals from each year.

Table 1: Mortgages in the United States, 2022–25

| Year | Total Loans | Covered Loans |

| 2022 | 8,406,350 | 5,467,246 |

| 2023 | 5,710,399 | 3,362,732 |

| 2024 | 6,176,052 | 3,649,951 |

| Total 2022–24 | 20,292,801 | 12,479,939 |

| 2025 (preliminary) | 6,823,421 | 3,986,515 |

| Total 2022-25 | 27,116,222 | 16,466,454 |

The Consumer Financial Protection Bureau (CFPB) also recently released a preliminary version of the HMDA data, with limited demographic information, for loans originated in 2025. Based on that data, in 2025, the total number of originated loans was 6,823,421, which reduced to 3,986,515 covered loans after filtering. With those numbers included in the total, the number of loans originated in 2022–25 was 27,116,222, which reduced to 16,466,454 covered loans after filtering.

Average interest rates fell to around 6% for a 30-year fixed rate mortgage at the beginning of 2026, though they have since risen significantly due to the Iran war. At that rate of 6%, 3,074,584 of the 12,479,939 borrowers who originated covered loans in 2022, 2023, or 2024—about 25%—would be in the money for refinancing because they had loans with interest rates of 6.75% or more.3 Including the preliminary 2025 data brings that number to 4,223,318 of the 16,466,454 borrowers—again about 25%—who would be in the money for refinancing.

With respect to demographics, 810,369 (26.4%) borrowers of covered loans from 2022–24 who are in the money at a rate of 6% are low-to-moderate income (LMI),4 defined as having incomes less than 80 percent of their area’s median family income (CFPB 2024c). We estimate that this number rises to about 1.1 million borrowers if we include loans originated in 2025.5 For covered loans from 2022–24, 27% of Hispanic or Latino borrowers would be in the money at a rate of 6%, as would 21.6%, 23.9%, and 25.2% of Asian, Black, and white borrowers, respectively.

If the mortgage rate were to fall an additional 0.75% to 5.25%, 5,999,168 borrowers from 2022–24 (an additional 2,924,584 borrowers, and close to half of all borrowers from 2022–24) would be in the money because they had loans with interest rates of 6% or more. Including 2025 brings that number to 8,802,931. If the rate falls by a further 0.75% to 4.5%, 8,500,686 borrowers from 2022–24 (an additional 2,501,518 borrowers, or more than two-thirds of all borrowers from 2022–24) would be in the money because they had loans with interest rates of 5.25% or more. Including 2025 brings that number to 12,247,684. And falling interest rates make refinancing even more profitable for borrowers who would still be in the money at higher interest rates.

Table 3: Borrowers “In the Money” at Various Interest Rates

| Interest Rate | Number of Borrowers “In the Money” from 2022–24 | Percent of Borrowers of Covered Loans | Numbers of Borrowers “In the Money” from 2022–25 |

|---|---|---|---|

| 6% | 3,074,584 | 24.6% | 4,223,318 |

| 5.25% | 5,999,168 | 48.1% | 8,802,931 |

| 4.5% | 8,500,686 | 68.1% | 12,247,684 |

A Path for More Equitable Refinancing

This report begins by reviewing existing literature on the benefits of and disparities in mortgage refinancing across various groups, possible causes of those disparities, and existing policy proposals to remedy them. The reason that mortgage refinancing occurs unequally is largely not that the refinancing of low- and moderate-income homeowners’ mortgages is unprofitable for financial institutions. LMI borrowers are a key client market segment for many mortgage lenders, both for purchase and refinance transactions. Instead, certain homeowners’ failure to refinance reflects a combination of frictions during refi booms—factors and costs that make low- and moderate-income borrowers relatively less likely to apply for refinancing, and similarly factors and costs that make financial institutions less likely to prioritize offering refinancing to these borrowers. Fortunately, many of these frictions should be able to be eased with relatively light-lift policy interventions. And if these frictions are addressed, many more low- and moderate-income borrowers should be able to refinance in transactions that will be attractive for them and the financial institution.

To illustrate the scale and cost-effectiveness of this opportunity for policymakers, consider an illustrative back-of-the-envelope analysis. If the proposed policy interventions enabled a successful refinance for even one-quarter of the approximately 1.1 million LMI borrowers who would be in the money at a 6% mortgage rate from 2022–25 (approximately 275,000 households), the economic impact would be substantial. Assuming a modest 0.75% interest rate reduction on an average loan of $199,000, each borrower would capture roughly $1,200 in annual savings. For this subset alone, this equates to $330 million in aggregate annual savings (over $2.3 billion in total savings over a typical seven-year loan life). If the average loan amount reaches $300,000, these figures climb to $1,800 in annual savings per household and $495 million in aggregate annual savings (roughly $3.5 billion in total savings). These projections are likely quite conservative, as they do not account for borrowers achieving savings beyond 0.75%.

Conversely, the fiscal cost to achieve these gains is remarkably low. The recommendations discussed below would primarily require the administrative labor to make federal and state-level legislative and regulatory changes, not direct subsidy to borrowers. The cost of these changes would pale in comparison to the extra dollars in the pockets (better housing affordability) for families. And even if states were to completely eliminate one-time taxes and fees for households that refinance, the fiscal effect would be much less than the benefits to those families, especially over the course of the loan. The average taxes and fees for refinancing are estimated to be $265, far less than the estimated savings in even the first year of $1,200 on a $199,000 loan refinanced to reduce the interest rate by 0.75%.6 Eliminating one-time fees for 275,000 borrowers would cost about $73 million, well below the estimated benefit to these borrowers of $330 million in just the first year. That cost would go up if more borrowers refinanced with taxes and fees waived, but those costs would again generally be well below the savings to those borrowers in even the first year. Consequently, addressing these refinancing frictions is an exceptionally cost-effective policy lever.

Existing literature already makes strong cases for modifications to programs operated by the Federal Housing Administration and Fannie Mae and Freddie Mac as key pillars for improving the equity of mortgage refinancing (Stein and Bhagat 2021; Alexandrov, Goodman, and Tozer 2022). We show that complementary solutions can also be found in targeted, relatively low-cost policy interventions that address additional market frictions and incentive misalignment.

Our policy discussion begins with a brief overview of how the market for mortgages works in the United States and the state and federal policy apparatus that shapes the mortgage market. We then propose several federal policy actions that should enable more low- and moderate-income homeowners to refi, including by empowering state and local officials. Congress should empower states to enable low- and moderate-income borrowers to refi by amending the Internal Revenue Code to allow states to issue tax-exempt bonds on favorable terms to fund mortgage refi programs. (This proposal is broadly similar to the recently introduced Affordable Housing Bond Enhancement Act, although we suggest some additional guardrails to ensure these bonds are used for affordable housing.) We also propose that the Federal Housing Finance Agency (or the CFPB or Federal Reserve) use existing federal regulatory authority to create a “mortgage refi dashboard” that would enable the public and policymakers to track refinance activity on an ongoing basis (perhaps monthly). Additionally, the CFPB should change its rules to smooth out underwriting requirements for refi loans, and the government-sponsored enterprises Fannie Mae and Freddie Mac should make accompanying changes to smooth out paperwork and documentation requirements. Federal policymakers should also apply antidiscrimination law to lenders whose refi activity has a disparate impact on borrowers in protected groups.

At the state level, policymakers have a significant opportunity to unlock refi for low- and moderate-income borrowers by targeting refi programs around homeowners who originally purchased their homes with Down Payment Assistance in an existing state-level program. We also stress a range of enhancing policy levers for state and local policymakers. States could reduce closing costs by modifying or waiving taxes and fees that make up a large portion of closing costs in certain states or by creating public options for mortgage services. Additionally, to support the other tactics described in this report, states, municipalities, or nonprofits supported by philanthropy could lead informational campaigns focused on encouraging homeowners to consider refi as interest rates fall. Given the amount of money at stake in mortgage refinancing, such campaigns could be an extremely effective use of resources for philanthropy or other sources, particularly in jurisdictions where lower one-time costs make refis profitable for more borrowers. States should also apply antidiscrimination laws to refi lending.

Existing Research on Mortgage Refinancing Benefits and Disparities

The process of mortgage refinancing is similar to the process of originally financing a home purchase. A potential lender will consider the homeowners’ financial characteristics, such as the applicants’ credit history, income, debt obligations, liquid assets, down payment, and home value (Comerica Bank n.d.). Borrowers need to provide documentation of these characteristics and pay closing costs (DeFusco and Mondragon 2020). The refinance process can be time-consuming, taking an average of roughly 42 days even in 2025 when lenders were not facing huge demand for refi (Yale 2025).

Refinancing through the federal government’s Home Affordable Refinance Program in the wake of the 2008 financial crisis had significant benefits for borrowers, including both substantial reductions in mortgage default rates and reductions in delinquency rates on non-mortgage debt (Abel and Fuster 2021). This is consistent with other studies showing that reducing monthly mortgage payments substantially decreases default risks, especially for homeowners with negative equity or lower credit scores (Ehrlich and Perry 2015).

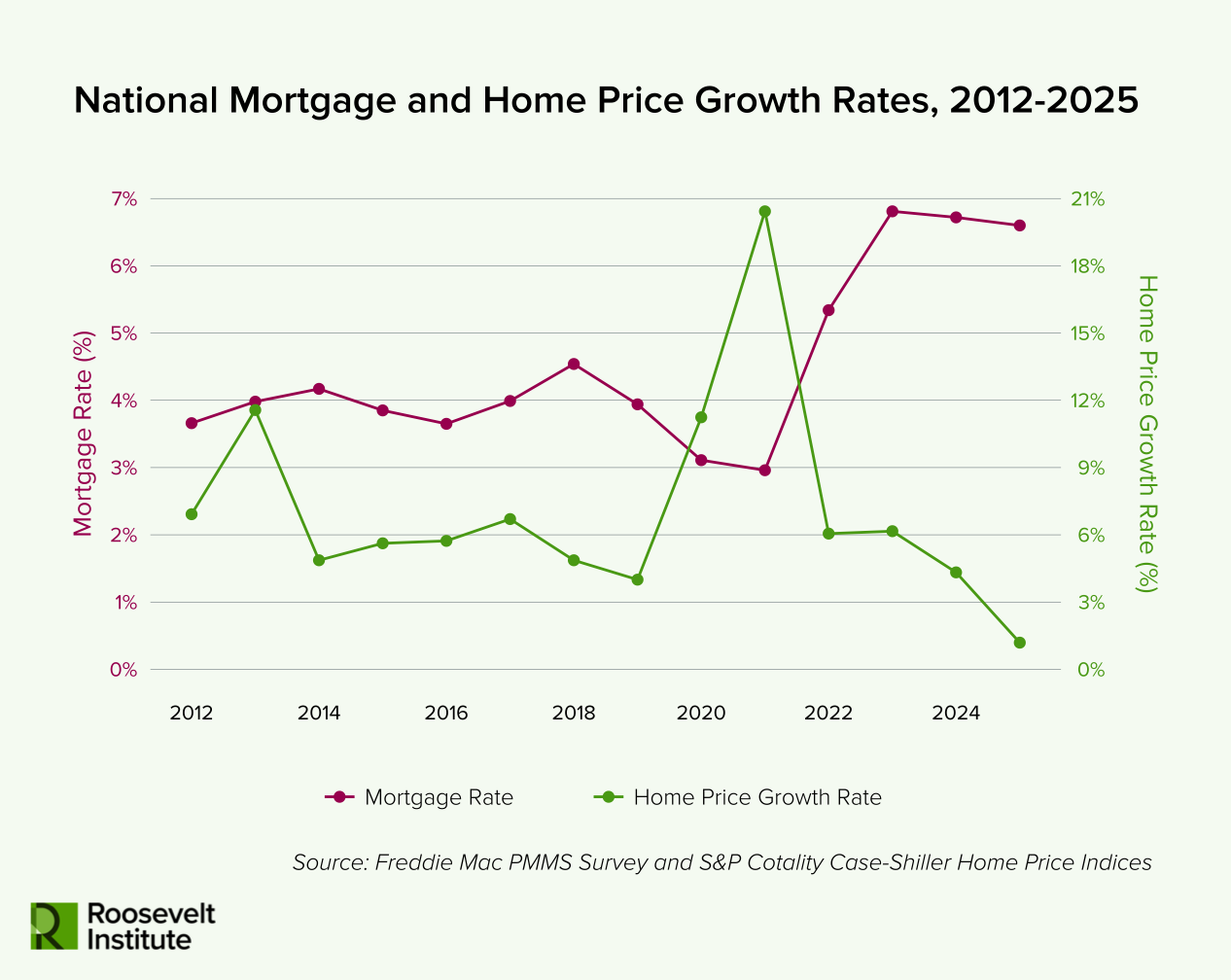

The COVID-19 pandemic sparked a dramatic boom in mortgage refinancing throughout the United States, spurred by a historically low interest rate environment and spikes in home valuations. 2020 saw the largest inflation-adjusted dollar value of refinance originations since the early 2000s, reaching $2.6 trillion in total. Many households refinanced as home prices grew 10.4% year-over-year (compared to the 10-year average of 5% between 2010 and 2020) and the 30-year fixed mortgage rate averaged 3.1%, a decline of about 0.83% from a year earlier. Homeowners who refinanced saved on average more than $2,800 annually in their mortgage payments, and about one-fourth of refinance borrowers shortened their loan term (Freddie Mac 2021). Another study found that refinancing during the COVID-19 pandemic resulted in an average of $8,800 in savings over the expected life of the loan (Agarwal et al. 2024). That high refinance activity carried into 2021 and 2022, with home prices continuing to grow year-over-year at 18.9% and 5.6%, respectively (S&P Dow Jones Indices 2026). However, following a 10-year low of 2.96% in 2021, the annual average mortgage rate rebounded to 5.34% in 2022 as the Federal Reserve raised interest rates to slow inflation, leading to a rapid reduction in refinancing activity that culminated in an almost 30-year low in 2023 (Freddie Mac 2023). Since then, annual home price growth fell to 1.1% in 2025 (S&P Dow Jones Indices 2026).

The gains from refinancing have not been evenly distributed across all homeowners. Of course, not all homeowners with mortgages will benefit from refinancing. As noted above, it is generally accepted that borrowers need a new interest rate that is at least 75 basis points lower than their existing rate to be incentivized to refinance (Wheat et al. 2023). These borrowers are sometimes referred to as “in the money.”

Fixed costs associated with refinancing can be a significant impediment to refinancing for many borrowers and make a bigger difference for borrowers with lower mortgage balances. About a decade ago, refinance closing costs were estimated to be about 1 percent of the loan amount plus $2000 (Agarwal, Driscoll, and Laibson 2013) with a more recent mean of $2,844 and median $2,990 (Kiefer, Kiefer, and Mayock 2023). These costs vary significantly by jurisdiction, primarily due to differences in taxes and government fees. For example, one study found that “the median cost of refinancing a conventional 30-year fixed-rate mortgage with an initial balance between $190,000 and $210,000 ranged from a low of $1,997 in Iowa to a high of $4,957 in New York,” with some of the costliest jurisdictions having very high taxes and fees (Kiefer, Kiefer, and Mayock 2023). The average borrower in Iowa paid only $84 in taxes and fees, while the tax and fee component of closing costs exceeded an average of $1,000 in New York and Florida. Iowa has also reduced closing costs by eliminating private title insurance, instead offering a state-run public option, with prices that are consistently among the lowest in the nation (Sterk 2022; Berry et al. 2025).

Under certain circumstances, these fixed costs can be financed as part of the refi transaction.7 But even so, these costs reduce the benefits of refi, especially for borrowers with lower mortgage balances, sometimes enough to make the refinancing no longer in the borrower’s interest. And borrowers with lower mortgage balances tend to be low- and moderate-income (LMI) borrowers.

In any event, many homeowners who would benefit financially from refinancing fail to do so. One study found more than a million such borrowers in the United States failed to refinance during the COVID-19 pandemic (Wheat et al. 2023). Another study estimated that about 90 percent of in the money homeowners failed to refinance during 2020 (Gerardi, Lambie-Hanson, and Willen 2021).

Throughout the mid 2010s, individuals in the top and bottom quintile of the income distribution had the same probability of refinancing. That changed dramatically during the refinance wave that began in 2020, when the top quintile of the income distribution increased its refinancing activity substantially as interest rates dropped and the bottom quintile did not (Agarwal et al. 2024). In 2020, borrowers in the top income quartile were 2.2 times more likely to refinance than those in the lowest quartile (1.1% compared to 0.5%) (Wheat et al. 2023). Additionally, in the mid 2010s, borrowers in the bottom quintile of the income distribution on average reduced their interest rate by more than borrowers in the top income quintile (1.66% vs. 1.5%), whereas in 2020 that gap more than closed, with borrowers in the bottom income quintile receiving slightly less of an interest rate reduction than borrowers in the top income quintile (1.82% vs. 1.86%). Accordingly, even adjusting for loan balance, the gap in savings from refinancing between the top and bottom quintiles of the income distribution increased tenfold in 2020 (Agarwal et al. 2024).

The savings from refinancing also differed significantly by race and ethnicity. From early 2020 through October of that year, 6% of Black borrowers refinanced compared to 12%, 14%, and 9% of white, Asian, and Hispanic borrowers, respectively (Gerardi, Lambie-Hanson, and Willen 2021; DeMaria 2022). Black households, which at the time composed 9.1% of all homeowners, accrued only 3.7% of the savings from refinancing during that period. This is true even though Black and Hispanic borrowers were actually more likely to be in the money than other borrowers, in part because they are less likely to have previously refinanced to a lower interest rate (Gerardi, Willen, and Zhang 2023). Indeed, only 5.8% of in the money Black borrowers refinanced in 2020, compared to 10.9% of in the money white borrowers (Gerardi, Lambie-Hanson, and Willen 2021).

Causes of the Disparities

The reason why so many fewer LMI borrowers refinance than higher-income borrowers is primarily not that refinancing the mortgages of LMI borrowers would be unprofitable for financial institutions. As noted above, LMI borrowers are an important market segment for many mortgage lenders. Rather, the disparities in who refinances are primarily attributable to factors and costs that make LMI borrowers less likely to apply for refinancing during refi booms and less likely to be prioritized by financial institutions, especially when refi booms strain originator capacity. This distinction is critical because it suggests that solutions can be found in targeted, relatively low-cost policy interventions that address market frictions and incentive misalignment, rather than requiring large, ongoing public subsidies. And because mortgage refi substantially benefits household balance sheets and reduces default rates, these interventions should be extremely cost-effective.

Existing research indicates that certain homeowners apply for refinancing less frequently than other homeowners, even when it may economically benefit them. Low-income borrowers applied to refinance their mortgages during the pandemic much less frequently than high-income borrowers (Agarwal et al. 2024). Almost 16 percent of refinancing applications come from borrowers in the top decile of the income distribution of portfolio mortgages, and only 4.5 percent come from the bottom decile (Agarwal et al. 2024). When disaggregating for race and ethnicity (and excluding borrowers lacking race/ethnicity data), Hispanic borrowers composed 7.6% of all refinance applications in 2020 and non-Hispanic Black borrowers made up 4.7% (author’s calculations using 2020 HMDA data), while Hispanic homeowners and non-Hispanic Black homeowners made up 10.5% and 7.9% of all homeowners, respectively (US Census Bureau 2023).

These disparities in homeowner refi application rates can be broken down into several subfactors. Part of the explanation is that low-income borrowers are more often in acute financial distress and unable to, for example, show the necessary income required to refi (DeFusco and Mondragon 2020). That said, the number of LMI borrowers in financial distress pales in comparison to the number of LMI borrowers who are in the money to refinance (Agarwal et al. 2024). Borrowers may also systematically differ by demographics in whether they would benefit financially from mortgage refinancing, even after accounting for loan balance. In particular, as noted above, closing costs vary significantly by jurisdiction, and the populations in these jurisdictions correlate with differences in borrower demographics (Kiefer, Kiefer, and Mayock 2023; Berry et al. 2025). This likely accounts for some of the difference in the demographics of who applies to refinance.

Additionally, borrowers’ financial literacy may account for some of the differential in who applies for refinancing. The National Association of Realtors (2021) articulated that many homeowners missed out on refinancing during the pandemic due to a lack of knowledge of the refinance process. Higher financial literacy has been linked to a greater propensity to refinance (Bialowoski et al. 2022). Another study found that greater familiarity with online financial services mitigated refinancing inequality during the pandemic (Agarwal et al. 2024). Consistent with this explanation, one study found significant “peer effects” of refinancing during the pandemic, including that homeowners are significantly more likely to refinance if a neighbor within 50 meters has recently refinanced (McCartney and Shah 2022). Another study showed that exposure to relevant media coverage can affect refinancing behavior, particularly among lower-income and minority borrowers (Hu et al. 2024).

Lender behavior also appears to have a significant effect on disparities in the rates of who applies for refi. Capacity constraints during refinance booms lead lenders to ration attention away from LMI borrowers (Frazier and Goodstein 2025). Refinancing LMI borrowers may be less profitable for lenders than other borrower populations for a variety of reasons. Fixed lender costs associated with soliciting and processing borrowers for mortgages are disproportionately large for smaller loan balances. Moreover, lenders may prioritize processing applications from higher-income borrowers because underwriting and completing the documentation required for an application is easier for borrowers with a single, continuous source of W-2 employment. One study found that lenders adjust their marketing strategies by targeting outreach or advertising to higher-income households or by triaging requests for a formal price quote, for example by screening calls and prioritizing higher-income customers (Frazier and Goodstein 2025). Another study found that unpaid balance size had a particularly large effect on refi activity during the pandemic and suggested that lenders may have targeted their marketing efforts toward high-income borrowers, who tend to have larger loan balances (Agarwal et al. 2024).

While studies have found that income disparities in who ultimately refinances largely are attributable to disparities among who applies for refinancing (Agarwal et al. 2024; Frazier and Goodstein 2025), there are also significant disparities in who gets approved for refinancing among those who apply. When lenders face excess demand, they may deprioritize loan applications from lower-income borrowers, as reflected in longer application processing times and higher rates of applications being closed or denied for incompleteness (Frazier and Goodstein 2025).

There are also significant racial disparities in who ultimately gets approved for refinancing. For example, in 2020, Black and Hispanic borrowers were approved at rates of 71% and 79%, compared to 87% and 85% for white and Asian borrowers. Some of the largest banks had significant racial disparities. One of the biggest banks in the United States had especially large racial disparities, approving only 47% of Black homeowners who completed a refinance application, compared with 72% of white homeowners. The industry as a whole approved a greater share of applications from low-income white homeowners than Black applicants at all income levels. While the industry explains away these racial disparities as a matter of Black borrowers having lower credit scores, banks have also lobbied against releasing federal data accompanied by credit score information that would allow the public to verify these claims (Donnan et al. 2022).

Existing Policy Proposals

Our survey of the existing literature found a handful of policy proposals to increase the number of LMI homeowners who refi. Consistent with proposals we advocate for in this report, the National Consumer Law Center, Center for Responsible Lending, and National Housing Law Project (2022) as well as Alexei Alexandrov, Laurie Goodman, and Ted Tozer (2022) have proposed that the CFPB make certain changes to its regulations to streamline underwriting for refinance transactions. At the height of the COVID-19 pandemic, there were similar proposals to allow refinancing without income verification (Golding et al. 2020; Gerardi, Loewenstein, and Willen 2021). As previously noted, Eric Stein and Kanav Bhagat (2021) have suggested improving pricing and removing administrative burdens for refinancing Federal Housing Administration (FHA) loans, including eliminating upfront mortgage insurance payments and allowing borrowers to roll their closing costs into loans refinanced with FHA.

Certain proposals would more dramatically change the refi market than those we contemplate in this report: Alexandrov, Goodman, and Tozer (2022) propose more significantly reducing requirements for refi and also requiring servicers to proactively contact all borrowers with a refinancing offer when their potential financial gains from refinancing are large enough. A considerably more dramatic proposal would be to reimagine mortgage contracts to include automatic refinancing (Bhagat 2021).

Market and Policy Structure

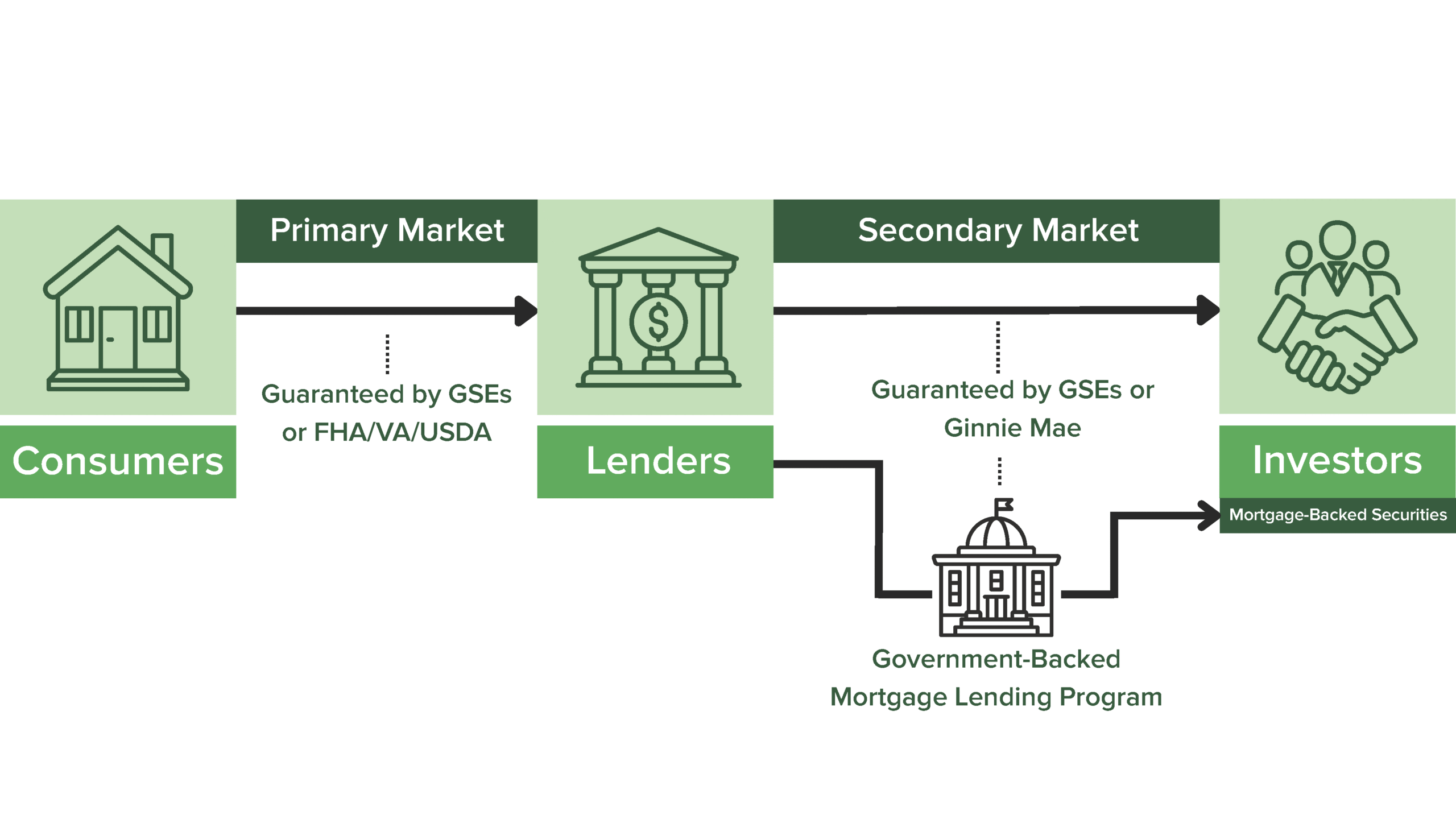

In the “primary market” for mortgage loans, private financial institutions (banks and nonbank mortgage lenders) interact directly with consumers. These lenders underwrite consumers (i.e., look at individual consumers’ and the homes’ characteristics) and then offer consumers mortgage loans with particular terms based on the underwriting, subject to significant regulation. Mortgage loans are then packaged for sale as so-called mortgage-backed securities, which are purchased by investors.8 The sale of loans from a financial institution to an entity that handles the packaging and issuing of the securities as well as the sale of the resulting securities to investors make up the “secondary market” for mortgage loans.

The federal government’s role in this market is to “guarantee” loans originated by financial institutions meeting certain specifications as well as securities made from those loans. The guarantee is that, if the consumer fails to pay back the loan or the entity collecting consumer payments fails to pay investors, the government will step in and pay. (As explained below, homeowners ultimately pay for this guarantee.) The government’s specifications control underwriting standards, documentation that the borrower must provide, and operational practices by the financial institutions themselves. Because financial institutions design the vast majority of mortgage loans in the United States to meet these specifications, the specifications have a large impact on financial institution activity (OFHEO 2008).

From the perspective of investors in mortgage-backed securities, they are purchasing a steady stream of money—“fixed income”—from the payments by consumers on their mortgages. Accordingly, the risk to these investors is that these payments will stop early. Payments can stop early either if consumers “prepay” their mortgage (i.e., pay off the mortgage before the end of the duration of the mortgage, either by selling the home or refinancing the mortgage) or if consumers default (stop paying). Since the government guarantees repayment on the loans and securities, the investor is generally indifferent between prepayment and default.9

How the Policy Proposals in This Report Would Affect the Mortgage Market

The policy proposals discussed in this report would likely modestly reduce the value of mortgage-backed securities to investors, because increasing the rate of refinances would, by design, facilitate prepayment of certain mortgages that would otherwise remain outstanding.

A countervailing effect is that refinancing decreases the risk that borrowers will default and cause prepayment via the government guarantee (Golding et al. 2020; Alexandrov, Goodman, and Tozer 2022).10 And some uncertainty about prepayment rates is already priced into the yields of mortgage-backed securities (Golding et al. 2020).11 Nonetheless, in the long run, increased refinancing would likely reduce the value of mortgage-backed securities.

In turn, this reduction in value to investors may be passed on to borrowers in the form of higher interest rates (Alexandrov, Goodman, and Tozer 2022). Indeed, LMI borrowers are currently essentially subsidizing higher-income borrowers who are more likely to refi, as everyone pays the market-wide higher interest rates resulting from refis.

These effects are likely to be small. On the whole, estimates about the effects of increased interest rates due to increased refinancing are in the range of 5 to 25 basis points, with the lower end of that range being more likely (Golding et al. 2020; Alexandrov, Goodman, and Tozer 2022).12

It is also possible that the proposals in this report will change who refinances in a way that somewhat increases costs on mortgage lenders. For example, requiring mortgage lenders to solicit borrowers more equitably for refinancing could impose additional costs on the system, including by ultimately encouraging borrowers with smaller loan balances to refinance. This could also increase interest rates or reduce the availability of funds for refinances. Again, we expect this effect to be modest.

Additionally, increasing refi rates should make monetary policy more effective by putting money from declining interest rates immediately into the hands of families (Golding et al. 2020).

How Government Policy Shapes the Mortgage Market

To design effective policy solutions, it is essential to understand the distinct roles, authorities, and limitations of how government policy shapes the mortgage market.

GSEs, FHA, and Ginnie Mae: Fannie Mae and Freddie Mac (known as government-sponsored enterprises, or GSEs) dominate the conventional secondary mortgage market, while the Federal Housing Administration (FHA) (in partnership with Ginnie Mae) has increasingly become the primary source of mortgage credit for LMI, underserved, and first-time homebuyers.13 The GSEs and FHA guarantee payment on loans meeting their respective specifications, including borrower characteristics (Lucas and Torregrosa 2010; FHFA n.d.). As noted above, borrowers pay the cost of the guarantee.14 The GSEs also buy loans and package and issue them for sale as securities. In contrast, Ginnie Mae guarantees securities composed of FHA loans (but does not buy loans).15 Financial institutions in the primary market that originate FHA-guaranteed loans either package and issue the loans as Ginnie Mae–guaranteed securities themselves or sell the loans to another entity that does so (Ginnie Mae n.d.). In practice, the GSEs, FHA, and Ginnie Mae establish the underwriting, documentation, and operational standards that govern the vast majority of the US mortgage market.

The Federal Housing Finance Agency (FHFA) regulates the GSEs. Fannie Mae and Freddie Mac must align their policies with the GSE Affordable Housing Goals, which for the 2026–28 period include specific benchmarks for low-income (up to 80 percent area median income) and very low-income (up to 50 percent area median income) home purchases and refinances (FHFA 2025c).16

LMI Lending – Regulatory Frameworks & Counterparty Obligations: Financial institutions offering mortgage loans must comply with the Ability-to-Repay and Qualified Mortgage rules administered by the CFPB. Mortgage lenders operating in the LMI space must also navigate a rigorous framework of federal and state regulations designed to ensure equitable credit access and community reinvestment. For banks, this includes the Community Reinvestment Act (CRA), which requires depository institutions to help meet the credit needs of their entire communities. All lenders in the mortgage market must also comply with the Home Mortgage Disclosure Act for transparent data reporting, the Equal Credit Opportunity Act and Fair Housing Act to prevent discriminatory practices like redlining, and evolving laws, including state-level CRA expansions that bring nonbank mortgage lenders under similar community-focused oversight.

State HFAs: For LMI borrowers, state housing finance agencies (HFAs) are the vital connective tissue between the primary mortgage market where consumers get loans and the secondary market. State HFAs do not usually offer mortgage products directly to consumers in the primary market, but they offer programs for financial institutions to offer loans in that market. State HFAs can pilot innovative program designs, tailor solutions to local market conditions, and fill gaps that federally uniform programs may leave unaddressed (FDIC n.d.). These programs have been successful at creating programs that both work for LMI borrowers and make lending to such borrowers attractive for lenders. In addition to being profitable, participation in state HFA programs supports compliance with federal CRA obligations, emerging state-level community reinvestment regimes, and the GSE Affordable Housing Goals.

In a state HFA program, financial institutions originate GSE- or FHA-guaranteed loans to consumers. The loans must meet the requirements of either the GSEs or FHA/Ginnie Mae as well as any state HFA-specific requirements. As described below, these loans are then sold on the secondary market in various ways (Stegman and Loftin 2021). The mortgages primarily differ from other loans by including Down Payment Assistance (DPA) for LMI borrowers. These loans have been instrumental in enabling LMI borrowers to purchase homes with low or no down payment.

Today, more than 30 state HFAs operate mortgage loan programs. Although collectively they account for roughly 3 percent of national mortgage-backed securities issuance, in a $13.5 trillion mortgage market this share still represents a substantial number of LMI households served—and a platform with meaningful potential for expansion (NCSHA 2025).

Policy Proposals

We begin by identifying frictions—factors and costs that make LMI borrowers relatively less likely to apply for refinancing and make financial institutions less likely to offer refinancing to these borrowers—that federal policy levers should address. We then recommend policy solutions at the state level, including informational campaigns perhaps facilitated by nonprofit organizations and philanthropy.

Frictions in the Refi Market That Federal Policy Levers Should Address

1. Obstacles to States Supporting Refis Like They Do Original Mortgages

We propose that Congress make targeted changes to the Internal Revenue Code to allow state HFAs to support refinancing of LMI borrowers using tax-exempt Mortgage Revenue Bonds (MRBs) while avoiding abuses that led Congress to close off this avenue in the past. State HFA programs have been successful at getting large numbers of LMI borrowers into mortgage loans, creating an attractive value proposition for both borrowers and lenders. However, federal law significantly constrains state HFAs from using MRBs to similarly support borrowers seeking to refinance. Targeted changes to remove that constraint would allow states to support refinancing to the same degree that they support original mortgages, including to help borrowers who received DPA and have second liens on their homes to refinance.

The central enabler of state HFA mortgage loan programs is their ability to issue MRBs.17 State HFAs issue and sell municipal bonds that are tax-exempt under federal law. Because the interest earned by the bond investors is tax-free, they accept a lower interest rate than they do for other bonds. The state HFA uses this cheap capital to finance the first mortgage on loans meeting GSE or FHA specifications and to fund the DPA it provides to borrowers. The DPA is often structured as a second mortgage lien on the home, with zero percent interest, which is typically forgiven in 5–10 years (Stegman and Loftin 2021).18 The loans (or mortgage-backed securities created from them) are then placed into a legal trust and pledged as collateral to back the MRBs (Federal Deposit Insurance Corporation n.d.; Morgan Stanley 2019; Gallo 2020). To limit lost federal revenue on tax-exempt bonds, each state is subject to a statutory cap on tax-exempt bonds it can issue, which states allocate among various types of bonds, including MRBs (CDFA n.d.).

MRBs were projected to cost the federal government roughly $5.1 billion in forgone revenue from 2024 to 2028 (JCT 2024). To put that number in perspective, from 2021 to 2025, state HFAs are projected to have funded $85 billion in mortgage volume from MRBs. This stream is the dominant source of financing for LMI first-time homebuyers. And by sacrificing this tax revenue to lower borrowing costs, the government effectively unlocks significant tranches of private capital that would otherwise remain on the sidelines. This trade-off is particularly critical in high-interest-rate environments, where the “yield spread” provided by tax-exempt bonds allows state HFAs to offer interest rates 1–2 percent below market averages, keeping homeownership accessible for LMI first-time home buyers. (This spending also reduces the need for rental assistance and other spending.)

However, the federal tax code significantly constrains the use of tax-exempt mortgage revenue bonds for refinancing. Due to amendments passed by Congress in the 1980s, the Internal Revenue Code § 143 (26 U.S.C. § 143(a)) limits tax-exempt bond proceeds to “qualified mortgage issues,” which are defined primarily as financing for the acquisition of a principal residence for low-income first-time homebuyers or, in more limited circumstances, qualified home improvement loans. Using these funds for programs to support refinancing of existing mortgages is largely prohibited.

Before the 1980s, MRBs were frequently exploited to refinance higher-income homeowners who already had access to credit, rather than helping new or lower-income buyers. States continuously recycled the money to refinance existing mortgages, including transactions that may not have produced much benefit to the borrower (but generated fees) and for properties owned by higher-income borrowers. This allowed financial institutions and wealthy borrowers to capture the financial benefit of the tax break, defeating the program’s purpose of expanding affordable housing. Congress eventually stepped in and largely prohibited funds from MRBs from being used for refi (JCT 1987).

Although Congress’s reaction to prior abuses was understandable, it threw the proverbial baby out with the bathwater, preventing the financing of even non-wasteful state refinancing programs using tax-exempt mortgage bonds. Properly structured, a modernized §143 refinance authority should deliver durable payment relief to households that are otherwise locked out of government-backed mortgage lending program refinance channels while including guardrails to prevent the former waste or abuse. Accordingly, we propose a targeted modernization of Internal Revenue Code § 143 to authorize state HFAs to issue MRBs in support of LMI mortgage refinancing. These changes are consistent with the recently introduced Affordable Housing Bond Enhancement Act (H.R. 7414 / S. 1511), which proposes to allow MRBs for refinancing, subject to certain guardrails to maintain the program’s focus on LMI borrowers. We support the following guardrails in that bill:

- Principal Residence: The home being refinanced should be the borrower’s principal residence and must be single-family (or two-to-four-unit properties if the borrower lives in one of the units and the building is at least five years old). This requirement ensures MRBs are used to subsidize homeowners, not investors.

- Income: Existing MRB income limits for first-time borrowers should apply to refinances. These limits ensure that MRBs are fulfilling the program’s promise of increasing housing affordability.

- Administrative Oversight: The Secretary of the Treasury should send yearly reports to Congress detailing how each state is using its tax-exempt bond authority. This requirement helps ensure on an ongoing basis that states are actually using the money for purposes Congress intended.

We recommend additional guardrails to further ensure MRBs benefit LMI borrowers:

- Net Tangible Benefit: Each refinance should be required to deliver a documented net tangible benefit to the borrower, such as a material reduction in monthly principal and interest payments, conversion from an adjustable-rate loan to fixed-rate mortgage at a similar monthly payment amount, or shortening of loan term at a similar monthly payment amount. This requirement would ensure that the borrower is actually benefiting from the loan and not merely generating fees for financial institutions.

- Loan Seasoning: Refinances funded by MRBs should only be allowed after a minimum “seasoning” period that the borrower has held their original mortgage.19 This would ensure that the program is used to provide long-term stability, preventing churning for the purpose of harvesting fees.

- Qualified Mortgage Limitation: Eligibility should be restricted to Qualified Mortgages, as defined by the CFPB, to ensure robust consumer protections. (We discuss modifications to the Qualified Mortgage rule below.)

These guardrails directly respond to the policy failures that led to earlier restrictions, while aligning § 143 refinance authority with contemporary consumer-protection standards. Additionally, Congress can either maintain the existing volume caps on the total dollar amount of tax-exempt bonds a state can issue or expand the cap specifically for refinances. Either way, budget predictability will be ensured.

Modernizing § 143 would transform mortgage revenue bonds from a narrowly constrained purchase-only tool into a flexible but disciplined affordability stabilizer for LMI homeowners without reopening the door to the excesses of past decades.

2. Underwriting Requirements and Paperwork and Documentation Burden

We propose that the CFPB should change its rules to reduce underwriting requirements for refi loans and that Fannie Mae and Freddie Mac should make accompanying changes to smooth out paperwork and documentation requirements. These changes would both encourage more LMI borrowers to apply for refinancing and reduce the incentive for lenders to deprioritize those borrowers.

Underwriting requirements deter LMI borrowers from refinancing in several ways, yet make little sense in the context of refi. As noted above, some number of low-income borrowers are in acute financial distress that makes them unable to show the necessary income required to refi (DeFusco and Mondragon 2020; Agarwal et al. 2024). Also problematic are frictions related to paperwork and documentation for underwriting. Lenders typically require new appraisals and full income and asset documentation for refinances, which disproportionately burden LMI borrowers. These requirements impose higher time and administrative costs on borrowers with less flexible work schedules, fewer liquid assets, or nontraditional or irregular income sources. In turn, as noted above, this dynamic may also cause lenders to deprioritize the applications of LMI borrowers because they are more time-intensive and less likely to result in success for the lender.

The CFPB’s Ability-to-Repay and Qualified Mortgage requirements are consumer protection standards, designed to reflect Congress’s belief that certain lending practices (such as low or no-documentation loans or underwriting loans without regard to repayment) led to consumers having mortgages they could not afford, resulting in high default and foreclosure rates (CFPB 2013). But these rules do not serve that purpose when refinancing reduces the borrower’s risk of default. In that context, underwriting requirements protect investors to some degree, but generally not borrowers or the federal government (i.e., taxpayers). Our proposal to change these rules is largely consistent with a proposal by the National Consumer Law Center, Center for Responsible Lending, and National Housing Law Project (NCLC 2022).

For refinanced loans, underwriting to some extent serves the interests of investors in both the original mortgage and the refinanced mortgage. For the refinanced mortgage, underwriting ensures that the borrower can repay the new loan, “catching” situations where the borrower’s financial situation is worse when they try to refi than when they took out the original mortgage. This reduces default and hence prepayment risk for investors in the refinanced loan. For the original mortgage, underwriting requirements for a refi reduce prepayment of the original mortgage by “locking in” the borrower to the original loan. Hence, easing underwriting requirements may cost investors some amount of money, which may ultimately result in modestly higher interest rates, subject to the countervailing factors described above.

But underwriting for refinancing does not actually reduce default risk for the borrower or the federal government, assuming that the refi will reduce the borrower’s overall default risk by producing a net tangible benefit for the borrower. Crucially, a refinance does not result in any more mortgage loans; the borrower just moves from one mortgage to another. Hence, the government already bears the default risk for a borrower who is refinancing; the refi at most moves it around on the government’s books. Therefore, if the refi reduces the risk of default for that borrower, that reduces default risk to the government.

Even for the purpose of protecting investors, requiring new appraisals and full income and asset documentation is overkill for refinances that will reduce the borrower’s overall risk of default. The borrower already has a payment history on the existing mortgage, from which their ability to repay a lower mortgage payment (or otherwise less risky mortgage) can be largely gleaned. Assessing this payment history substantially meets the needs of protecting investors in a refinance.

Accordingly, we propose a safe harbor from the CFPB’s underwriting requirements in situations where the borrower has a solid payment history and the refi should reduce the borrower’s risk of defaulting by producing a net tangible benefit for the borrower. The CFPB should establish an explicit streamlined refinance Qualified Mortgage safe harbor for refinances that meet the following criteria:

- Payment History. Lenders generally require new appraisals as well as income and asset documentation primarily to meet the CFPB’s requirements. Specifically, to receive treatment as a “qualified mortgage” under CFPB rules, lenders must consider and verify an applicant’s income, assets other than the home, debt obligations, alimony and child support, and monthly debt-to-income ratio or residual income.[4] For refinances, the CFPB should replace this requirement with a requirement that the borrower has demonstrated a sustained record of on-time mortgage payments (e.g., only on-time payments within the last 6 months and no more than one late payment within the last 12 months). This easy-to-access record substantially captures a homeowner’s ability to repay a less risky mortgage as well as the metrics that would be replaced.20

- Net Tangible Benefit. If the refi reduces the borrower’s monthly payment without substantially increasing the principal loan amount, that should reduce the risk of default for that borrower. This would exclude cash-out refis, which by definition increase the principal amount, except to the degree that the borrower is financing minimal closing costs. Similarly, if the refi converts the mortgage from an adjustable to a fixed rate or lowers the mortgage term without substantially increasing the borrower’s monthly payment, that should also reduce the risk of default for that borrower. The CFPB should ease requirements related to underwriting for borrowers in these situations. (The transaction should involve no cash-out beyond bona fide closing costs and escrow funding.) This would also help prevent fee-harvesting by lenders in situations where the borrower does not benefit from the refi.

- Loan Term. The treatment of refinances that extend the borrower’s remaining loan term (for example, a new 30-year mortgage for a borrower who has already completed 10 years of payments) is more complicated. Some advocates have fully embraced such refinances because the longer term reduces the borrower’s monthly payment (NCLC 2022). Others have cautioned against longer loan terms that reduce the borrower’s accumulation of equity, increase the total amount of interest paid, and may have mixed effects on default rates (lower monthly payment but longer time where default is possible) (Alexandrov, Goodman, and Tozer 2022). We propose a middle path: The CFPB should require that the refinance default to the borrower’s remaining loan term unless the borrower expressly opts in to a longer loan term. This would ensure that families make the choice to extend loan terms carefully, in a context where multiple features of the mortgage may be changing.21

- Other Consumer Protections. The mortgage should otherwise meet the criteria for a Qualified Mortgage under CFPB rules.

This approach is consistent with public statements made by former CFPB Directors Kathy Kraninger (Ornstein 2020) and Rohit Chopra (2022), which emphasized that rigid underwriting requirements can unnecessarily impede access to risk-reducing refinances, particularly for borrowers who have already demonstrated an ability to repay. It also aligns with long-standing principles embedded in the FHA and GSE refinance programs, which recognize that successful loan performance is often the most reliable indicator of repayment capacity.

By explicitly aligning the Qualified Mortgage framework with performance-based underwriting for streamlined refinances, the CFPB could materially expand access to refinancing for LMI borrowers without weakening consumer protections or increasing systemic risk.

Further, in addition to the recommendations made by Stein and Bhagat (2021) with respect to the FHA Streamlined Refinance Program, there is also room to streamline LMI refinancing for GSE loans. Although the existing GSE programs have important flexibilities for refi, such as appraisal waivers and higher allowable debt-to-income ratios, more could be done by lenders to remove operational frictions. For instance, where income verification is necessary, lenders should rely on automated electronic tax transcripts, bank data, and other third-party verification tools rather than manual document collection. Additionally, if the CFPB modifies its underwriting requirements as described above, the GSEs should align their refi programs to accept payment history in lieu of income and asset verification. This proposal is broadly similar to some of the proposals made by Alexandrov, Goodman, and Tozer (2022).

Although the CFPB and GSEs have existing authority to make these changes, Congress could pass legislation requiring the CFPB and GSEs to make these changes.22

3. Lack of Ongoing Transparency About Refi Uptake

We propose the creation of a federal “mortgage refi dashboard”—hosted by FHFA or another federal agency—that would enable the public and policymakers to track refinance activity on an ongoing basis. Notwithstanding the significant role that refi plays for American families, including the large amount of money at stake, there is typically little ongoing information available during refi booms about patterns in refi transactions. Data is available on a yearly basis under the Home Mortgage Disclosure Act (HMDA), but the public and policymakers currently have no way to track refi trends more quickly. This prevents policymakers at all levels as well as private parties from putting pressure on financial institutions where disparities exist and makes it difficult for financial institutions themselves to target refi efforts.

If more information about refi trends were available on an ongoing basis, it would be useful in a variety of ways. Lenders could use the dashboard to target outreach to areas with many potential refi candidates. States and municipalities could use the information to put pressure on lenders in their communities to improve the equity of who refinances. For instance, municipalities could reward lenders by placing municipal deposits in institutions with particularly good records. Elected officials could also demand that financial institutions showing disparities improve and conduct oversight of large institutions with poor records. Private attorneys and law enforcement could mine the information to find lenders with disparities on the basis of class or other protected characteristics, supporting discrimination lawsuits under the Equal Credit Opportunity Act or other laws.

A federal mortgage refi dashboard would essentially contain the same data as available from HMDA, but it would be updated much more frequently—perhaps monthly, with at most a lag of a month or two. This information could be disaggregated by geography and demographics. As with HMDA, the data would be anonymized.

Multiple agencies, including the CFPB or Federal Reserve, could create this resource under existing authorities, but we believe the FHFA would host this database most easily. FHFA could simply update its existing National Mortgage Database of Outstanding Residential Mortgage Statistics to include this information and update that database more quickly. Alternatively, the CFPB could gather this information from financial institutions on a rolling basis and create this dashboard using its existing authority under section 1022 of the Dodd-Frank Act, which allows the CFPB to require financial institutions to provide data and other information. Or the Federal Reserve Banks could use their authorities or data from the Consumer Credit Panel to gather the data.

Although these regulators likely possess the ability to gather this information and create such a dashboard already, Congress could pass legislation requiring FHFA, CFPB, or Fed to do it.

Incidentally, many mortgage lenders have already built or procured dashboards to assist them with identifying LMI borrowers, at hyper-local levels, that are refinance candidates. As noted, LMI borrowers are a key client market segment for many mortgage lenders, both for purchase and refinance transactions. A national refi dashboard serves not only as a stick, but also as a carrot, providing mortgage lenders with benchmark information on local LMI refinance activity so they can recalibrate their internal dashboards accordingly. Moreover, if all lenders had access to a national mortgage refi dashboard that assisted lenders with identifying LMI candidates for refi, it would spur competition and potentially further reduce mortgage rates and fees for these borrowers.

4. Reducing the Burden of Title Insurance

We propose eliminating requirements to get new title insurance for refis wherever possible. Inflexible requirements to get new title insurance make little sense in the context of refinancing. For 2022–25 vintage loans, title insurance policies were recently obtained for the borrower’s original mortgage. Outside of Iowa (which as noted has reduced title insurance costs via a public option), title insurance costs for mortgage loans are material. The cost of a new title insurance policy for a purchase loan ranges from 0.5 to 1 percent of the purchase price. For a median-priced home of $420,000, that translates to roughly $2,100 to $4,200 (Old Republic Title n.d.). The borrower may in some circumstances pay less for title insurance when refinancing, but nonetheless is typically required to get the insurance even when unnecessary.

In some states such as Florida, Texas, and Pennsylvania, lenders are required to offer borrowers a “reissue” rate on their lender’s title insurance policy, which can be discounted up to roughly 40 percent (First Integrity Title Company n.d.; Supreme Title 2022; Legal Information Institute n.d.). But borrowers who do not live in these states face substantial hassle as well as cost, as they must shop around with title companies to obtain favorable rates.

Further and substantially reducing these fees at the federal level would unlock even more borrower savings. (State options to reduce closing costs, including further discussion of Iowa, is included in the state-focused section below.) In 2024, the FHFA launched a pilot program to waive the requirement for lender’s title insurance on certain low-risk, “standard” refinances handled by Fannie Mae and Freddie Mac (Grace 2024). This pilot aims to save borrowers an average of $750. This program should be expanded to further streamline or eliminate this requirement, as proposed by Alexandrov, Goodman, and Tozer (2022).

5. ECOA at the Federal Level

An additional—and often overlooked—policy dimension concerns antidiscrimination law and the legal obligations of lenders in refinance, particularly with respect to outreach and solicitation. This law includes the federal Equal Credit Opportunity Act (ECOA), which private litigants and state attorneys general can enforce under section 1042 of the Dodd-Frank Act.

ECOA prohibits discrimination in any aspect of a credit transaction. It is hard to see why this would not include refinancing.

Evidence of discriminatory intent in refinancing is often difficult to establish. Nonetheless, there is a long history of pursuing ECOA claims against financial institutions for actions that have a disparate impact. The CFPB has recently proposed to interpret ECOA to dramatically narrow this legal theory by regulation. It is unclear if this interpretation will survive legal scrutiny (Jackman et al. 2025). In any event, the federal government is currently unlikely to pursue disparate impact cases. For this reason, we primarily discuss antidiscrimination claims as state-level policy levers below. Nonetheless, congressional policymakers should put pressure on the Trump administration to use this important tool.

Further, the statute of limitations for an ECOA claim is three years. So, depending on when refinancings take place, a future presidential administration could hold financial institutions accountable for ECOA violations that occur during the Trump administration. Policymakers in Congress or at the state and municipal level should also remind lenders of this possibility as part of other efforts to encourage institutions to pursue more equitable refinancing.

Frictions in the Refi Market That State Policy Levers Should Address

1. Helping Borrowers Who Received Down Payment Assistance

We propose that state HFAs create programs to help borrowers locked into their original mortgages because of their receipt of Down Payment Assistance (DPA) when they originated those mortgages. As noted above, a significant value-add of state HFAs is creating lending programs using sophisticated financing mechanisms that are attractive to lenders and help LMI borrowers with DPA. Notwithstanding how well these programs have worked at enabling LMI borrowers to purchase homes, they have had the unintended effect of locking many of these borrowers—particularly those with higher-rate mortgages—into their original mortgages. State HFAs could fix this “lock in” effect, especially if Congress allows them to use MRB funds for refinances as described above. We believe HFA-sponsored LMI refinance initiatives would be attractive to lenders.

As noted above, most DPA programs nationwide are structured as loans to the borrower that become second mortgages on the home. In these situations, when the consumer purchases the home, they take out an additional loan (mortgage) for some or all of the down payment, and this mortgage becomes a lien on the home that is subordinate (i.e., second) to the mortgage that covers the home’s purchase price (the first mortgage). Most of the time, this second loan is structured to be forgiven over time.

Many HFA program rules contain a “clawback” provision, under which any satisfaction of the original first mortgage automatically triggers full repayment of the DPA loan. Accordingly, when a borrower seeks to refi, the down payment assistance must be repaid—notwithstanding that the borrower is not selling the property and recovering all the principal and equity. This becomes a significant obstacle to refi. For many LMI borrowers, producing an average of $18,000 in cash23 at refi closing is infeasible, causing beneficial refinances to fail even when monthly payments would fall significantly.24 This creates a refinance “lock-in” dynamic. (This dynamic does protect investors in these loans from prepayment due to refinancing.)

If Congress modernized § 143 to permit the use of MRBs for refinances, state HFAs could deploy that authority to resolve this DPA lock-in problem. In such a program, the HFA should use proceeds from newly issued MRBs to repay borrowers’ existing first-lien mortgage in full, thereby satisfying any investor or bond covenants tied to the original financing.25 The borrower would then receive a new first mortgage at a lower interest rate that delivers a net tangible benefit.

The treatment of the DPA second lien would depend on program structure. In some cases, particularly where the second lien does not contain an explicit requirement that it be repaid upon refinancing of the first lien, the HFA could simply re-subordinate the existing second lien to the new first mortgage. This approach minimizes operational complexity and avoids unnecessary disruption to borrowers. However, where the original DPA includes a clawback that requires payoff if the first mortgage is satisfied, the HFA could originate a replacement second lien at refinance. That replacement lien would mirror the core features of the original DPA—zero or below-market interest, deferred or forgivable payments, and income-based eligibility—while preserving prepayment safeguards for investors in the new mortgage.

One operational consideration is how to treat the forgiveness or clawback period associated with the DPA. Policymakers must balance borrower equity and program integrity. On the one hand, it may be inequitable to reset the full forgiveness clock for a borrower who has already satisfied several years of occupancy requirements. On the other hand, some HFAs may reasonably determine that a partial reset—or an adjusted remaining term—is an appropriate trade-off for delivering a materially lower first-lien rate, particularly if maintaining predictable prepayment speeds is necessary to manage bond execution. State HFAs should determine whether to preserve elapsed forgiveness credit, apply a proportional remaining term, or reset the forgiveness schedule. HFAs must weigh borrower fairness against operational feasibility, especially where legacy portfolios contain second liens with varying structures and terms.

For the reasons described above with respect to congressional revisions to MRBs, HFAs should only allow refinances that produce a net tangible benefit to the borrower. Cash-out refinances should be prohibited, except for bona fide closing costs and escrow adjustments. Eligibility should be limited to owner-occupied principal residences meeting LMI income thresholds (e.g., borrower family income no greater than 120 percent of the median income earned by all families in their county) at the time of refinance. These guardrails ensure that the program functions as a payment-relief and affordability-stabilization tool rather than an equity extraction vehicle.

As with the proposed safe harbor for CFPB underwriting requirements, by default HFAs should arrange the refinanced first mortgage to have a term equal to the remaining term of the borrower’s original first mortgage. For example, if the borrower has already made 5 years of payments on their first purchase mortgage, the HFA should structure the refinanced first mortgage as a 25-year term loan to preserve the borrower’s equity. The exception should only be if the borrower expressly requests that the refinanced first mortgage be for the full 30-year term.

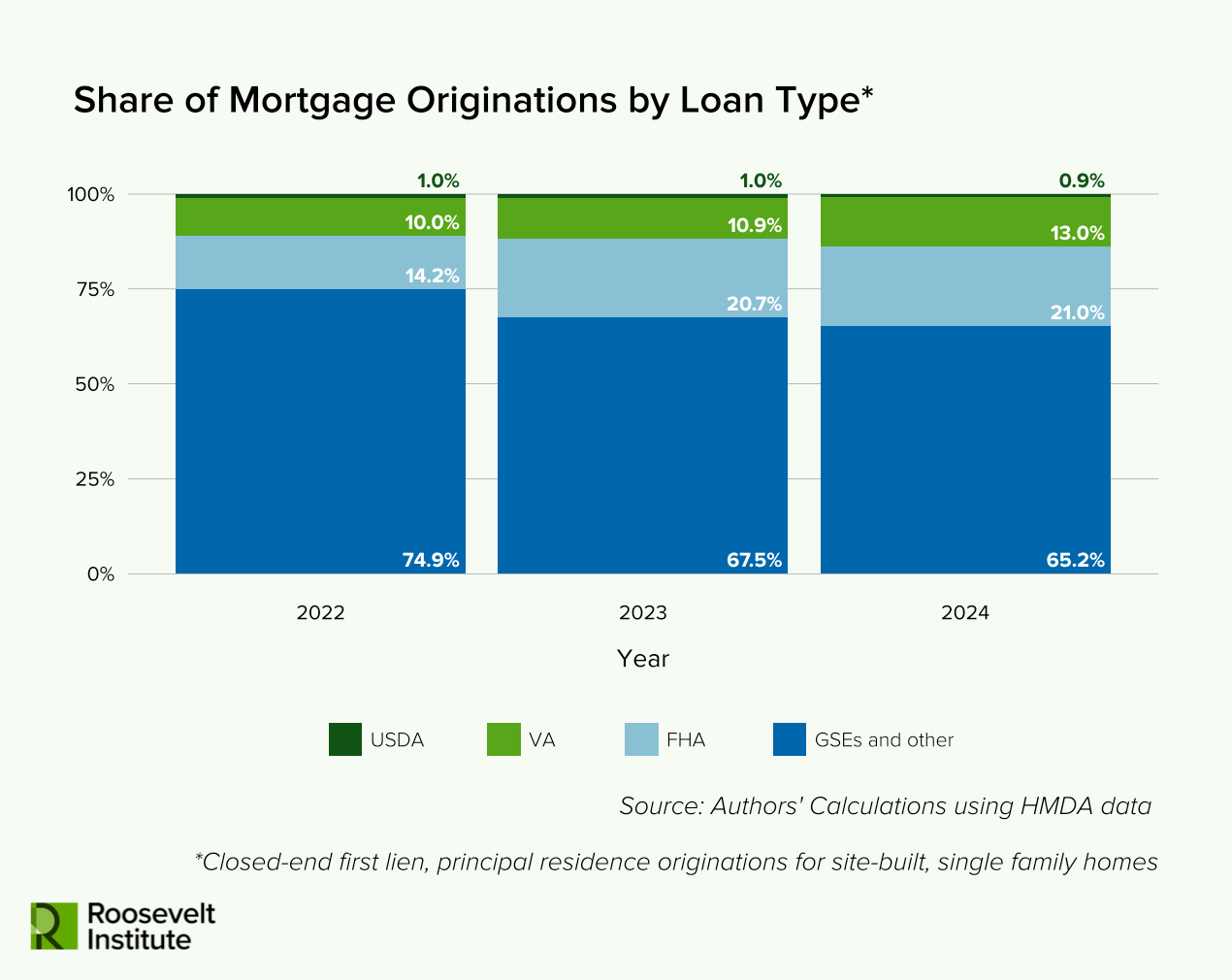

The potential scale of such a program is significant. There are currently more than 2,600 down payment assistance programs nationwide, including 466 administered by state HFAs. According to Cotality Araya Market Intelligence, approximately 650,000 FHA purchase loans originated in 2025 alone. Historically, roughly 18 percent of FHA borrowers rely on government-sourced down payment assistance. That implies more than 100,000 FHA purchase mortgages annually are originated with public DPA support. State HFAs account for roughly 19 percent of this segment, representing on the order of 20,000 FHA-assisted purchases per year. Across both FHA and conventional executions, MRB programs historically support between 80,000 and 100,000 new LMI homebuyers annually.

When mortgage rates spiked sharply beginning in the first quarter of 2022, a substantial cohort of these borrowers took out loans with interest rates between roughly 6.5 and 7.5 percent. Many did so out of necessity rather than timing advantage, as rental inflation, limited supply, and life-cycle pressures compelled purchase despite rising rates. As a result, hundreds of thousands of LMI homeowners are now positioned above prevailing market rates but are challenged in their ability to refinance because of DPA. And because the DPA pipeline continues to grow each year, the number of LMI homeowners who are locked out of refinancing increases over time. Unlocking § 143 refinance authority for state HFAs to create refi programs for this population would therefore open up refinancing for a sizable number of LMI homeowners.

Absent federal reform of § 143, state HFA options for refinancing mortgage borrowers with DPA are possible but more challenging. As a threshold matter, the HFA has to possess the operational ability to execute refinances via so-called capital markets execution. This approach to refinancing gets funds from private financial institution credit lines, as opposed to MRBs, which are not currently permitted for refinance loans. The state HFA uses credit lines from private financial institutions to finance the first mortgage. Loans facilitated by state HFAs are then packaged into securities. Because LMI borrowers are cash-constrained, they accept a slightly above-market interest rate on their first mortgage in exchange for upfront DPA. This higher interest rate generates a premium price from investors, creating a flow of upfront cash that contributes to the combined profits of all HFA activities. The HFA uses the profits it generates from its programs and activities to fund the DPA it provides to borrowers.

Assuming the HFA is able to execute refinances via capital markets execution, it needs to have a solution for handling the DPA on the original loan. If the DPA was either a zero percent interest soft-second lien or a low-interest amortizing second lien that does not have a clawback, the HFA can simply re-subordinate the existing second lien along with the new first mortgage. However, if the DPA was either form of second lien and contains the clawback provision, when originating the refinance the HFA would have to pay off the original DPA second lien using the HFA’s available profits from its combined activities and create a new second lien in its place to compensate itself for the financial outlay. These constraints inherently limit the population of DPA borrowers who can be assisted in the absence of federal reform of § 143.

We believe HFA-sponsored LMI refinance initiatives would be attractive to lenders. For lenders, participating in such an initiative converts small-balance, DPA-encumbered loans that are operationally unattractive today into standardized, low-risk, programmatic executions with predictable secondary-market treatment and limited repurchase exposure. Properly structured, a DPA refinance program operates not only as borrower relief, but as a mechanism for aligning public affordability objectives with private-market incentives.

2. Reducing Closing Costs

We propose that states and localities reduce certain closing costs. Closing costs may be a significant financial impediment to refinancing for LMI borrowers, especially in certain jurisdictions. As noted, these fixed fees disproportionately burden small-balance loans. (A $2,000 fee represents 1.3 percent of a $150,000 loan but only 0.4 percent of a $500,000 loan.) In some circumstances, this burden can be reduced by capitalizing these costs into the mortgage, allowing the borrower to pay the costs over time rather than upfront.26 But this reduces the benefits of refinancing for these borrowers. As described above, the median cost of refinancing a typical mortgage with an initial balance of about $200,000 ranged from a low of about $2,000 in Iowa to a high of about $5,000 in New York, and the average borrower in Iowa paid only $84 in taxes and fees, while the tax and fee component of closing costs exceeded an average of $1,000 in New York and Florida. (Kiefer, Kiefer, and Mayock 2023). Indeed, the difference in costs across jurisdiction may be significant enough to explain some of the disparities in mortgage refinancing rates across demographics. States and localities could modify or eliminate closing costs in a variety of ways, including waiving taxes and fees for lower-income borrowers, restructuring them to be less regressive, or creating public options for mortgage services, as in Iowa.